8th Annual Site Selection Consultants Survey Results

Since less than 50 percent of those responding to our 2011 Corporate Survey say they utilize the services of consultants in the site and facility planning process, we would expect the consultants' responses to differ from those of our corporate executive respondents. Let's find out to what extent they do.

Winter 2012

Fewer than half of the respondents to our 2011 Consultants Survey are working with manufacturing firms, while about the same number (42 percent) are working with distribution and logistics operations. The latter type of firms make up less than a fifth of those responding to our 2011 Corporate Survey. Additionally, about a fifth of the responding consultants are working with data center operations, financial services/insurance firms, and the healthcare and retail sectors (Slideshow, Chart A). These sectors are not significantly represented by the 2011 Corporate Survey respondents.

About 30 percent of those responding to the 2011 Consultants Survey are providing their clients with location studies/comparative analyses, as well as incentives comparisons and negotiations. A quarter of these respondents say they are actually making their clients' site selection decisions (Slideshow, Chart B). In fact, only about a quarter of the responding consultants say that the clients who ask them to perform a location search have already gathered preliminary data. Only a third say their clients have narrowed down the geographic area in which they wish to locate (Slideshow, Chart C).

The respondents to our 2011 Consultants Survey say that those using their services run the gamut from small to large in terms of their employment numbers, with mid-size firms (100-499 employees) being the primary users (Slideshow, Chart D).

Eighty percent of the responding consultants confirm that their clients' executive management is involved in the site selection process, with half noting the involvement of their clients' real estate, tax and finance, and other operational or business units as well (Slideshow, Chart E).

While 38 percent of the respondents to our 2011 Consultants Survey say their clients still plan to open new facilities or expand, despite the sluggish economy, 45 percent say the sluggish economy has caused their clients to put their new facilities plans on hold. More than 30 percent also say their clients are deferring capital spending and seeking ways to optimize current facilities (Slideshow, Chart F).

Importantly, two thirds of those responding to our 2011 Consultants Survey feel the U.S. economy will not improve until 2013 or 2014 (Slideshow, Chart G). However, the responding consultants are actually more optimistic than the 2011 Corporate Survey respondents, 80 percent of whom don't expect the economy to improve until 2013 or 2014.

When and Where Will Their Clients Open New Facilities?

When asked specifically about their clients who do expect to open new facilities, more than 85 percent of the responding consultants say those clients expect to open the new facilities within two years (Slideshow, Chart H). Of their clients planning new facilities, two thirds say their clients are planning only one, and a quarter say they are planning on opening two (Slideshow, Chart I). By comparison, of the corporate respondents planning new facilities, 70 percent are planning between two and five or more.

Many of those responding to our 2011 Consultants Survey are working on domestic location projects slated for the South (Alabama, Florida, Georgia, Louisiana, and Mississippi), accounting for 17 percent of the planned new facilities; for the South-Atlantic states (North Carolina, South Carolina, Virginia, and West Virginia), accounting for 15 percent of the projects; and for the Southwest (Arizona, New Mexico, Oklahoma, and Texas), which will see 12 percent of the consultants' clients' new facilities (Slideshow, Chart J). The Southwest region is also the one predominantly considered by the respondents to our 2011 Corporate Survey.

A quarter of the projects planned by the responding consultants' clients are slated to be manufacturing facilities, and another quarter will house warehouse/distribution operations. About 10 percent each will be headquarters or data centers (Slideshow, Chart K), many more of these last two types of facilities than planned by the respondents to our 2011 Corporate Survey.

The foreign locations mostly under consideration by the clients of those responding to our 2011 Consultants Survey include Asia (accounting for 23 percent of the projects), Mexico (18 percent), and Canada (17 percent). More of the projects planned by the respondents to our 2011 Corporate Survey are planned for Asia (33 percent), but fewer for Mexico and Canada - only 10 percent each. Those responding to the 2011 Consultants Survey say that China is their clients' preferred location for new Asian facilities (46 percent of the slated projects), followed by India (17 percent), and Malaysia (15 percent) (Slideshow, Chart L). Also of note, twice as many of the Corporate Survey respondents than the consultants' clients are planning new facilities for Western Europe (20 percent as compared with 10 percent).

Forty percent of the responding consultants' clients' foreign projects will house manufacturing operations, and 16 percent will be warehouse/distribution centers (Slideshow, Chart M). The respondents to our 2011 Consultants Survey are also working with clients who are setting up back office/call centers, data centers, and headquarters operations overseas. Interestingly, none of those responding to our 2011 Corporate Survey say they have plans for a foreign headquarters operation.

Nevertheless, 70 percent of those responding to our 2011 Consultants Survey say they have not seen an increase in the number of companies establishing foreign facilities as opposed to domestic ones over the last year (Slideshow, Chart N). And 35 percent also say that some of their clients have engaged in onshoring, i.e., have relocated a foreign facility back to the United States (Slideshow, Chart O) - a far greater percentage than being considered by the respondents to our 2011 Corporate Survey (just 3 percent).

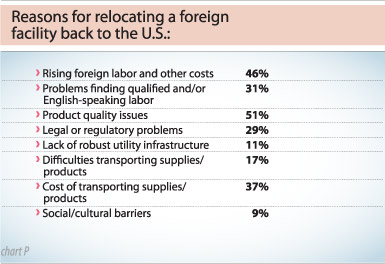

The majority of the responding consultants say that those planning onshoring moves have had problems with product quality coming out of their foreign facilities (51 percent) or are faced with rising foreign labor and other costs (46 percent) (Slideshow, Chart P). On the other hand, 62 percent of those responding to our 2011 Consultants Survey say economic instability is preventing their clients from spending more of their earnings on investment in U.S. facilities, and a third cite high corporate taxes as they reason for this lack of investment (Slideshow, Chart Q).

Do Their Clients Have Expansion or Relocation Plans?

When it comes to facility expansion plans, 84 percent of the responding consultants say that most of their clients who expect to expand facilities will do so within two years (Slideshow, Chart R). A similar percentage (83 percent) of those responding to our 2011 Consultants Survey also say their clients who are planning to relocate have one- to two-year plans (Slideshow, Chart S). A third of the responding consultants say a need for greater proximity to suppliers and/or markets served is behind their clients' relocation plans. Less than a fifth of the consultants cite high taxes, excessive government regulation, or labor costs as reasons for their clients' relocations (Slideshow, Chart T). However, these factors were cited by a much greater percentage of the respondents to the 2011 Corporate Survey as causing them to consider relocating a facility (41 percent cited high taxes and 25 percent cited both excessive government regulation and labor costs).

What Are Their Clients' Site Selection Priorities?

The consultants were also asked to rate the site selection and quality-of-life factors as "very important," "important," "minor consideration," or "of no importance" when helping their clients to make location decisions. The factors were then ranked based on the combined "very important" and "important" ratings. The 2011 consultants' ranking of the factors appears in Slideshow, Chart U.

This year, the consultants have ranked the same top factors in first and second place, respectively, as the 2011 Corporate Survey respondents. Highway accessibility is ranked as the consultants' number-one priority, with a combined importance rating of 98.3 percent. Labor costs is in the number-two spot, with a 96.3 percent importance rating.

Although highway accessibility is the only factor considered "very important" or "important" by more than 90 percent of the 2011 Corporate Survey respondents, more than 90 percent of the respondents to the 2011 Consultants Survey rated their top-five factors as "very important" or "important." Proximity to major markets - which showed the largest jump in importance in the 2011 Corporate Survey, although it is only ranked ninth by those respondents - is ranked third by the respondents to the 2011 Consultants Survey, with a 93.8 percent importance rating.

Like the respondents to our Corporate Survey, the responding consultants rate and rank availability of skilled labor quite high: it's in the number-four spot for 2011, with a 93.6 percent importance rating. On the other hand, availability of unskilled labor is near the bottom of the consultants' list of priorities, ranking 24th among the 26 site selection factors, considered "very important" or "important" by only about half of the responding consultants.

High unemployment rates may be responsible for the consultants' belief that unskilled labor is universally available and not very important in the location decision. In fact, half of the respondents to the 2011 Consultants Survey say high unemployment rates are making it easier for their clients to find the labor they need (Slideshow, Chart V) - only a third of the Corporate Survey respondents say this is the case. Nevertheless, of those consultants who think the unemployed are lacking skills, 45 percent say they are lacking both basic and advanced skills (Slideshow, Chart W).

Additionally, nearly 60 percent of the respondents to the 2011 Consultants Survey say their clients are dependent on contract or contingent labor (Slideshow, Chart X); only about 40 percent of the 2011 Corporate Survey respondents make that claim.

The available land factor shows the largest jump in importance in the consultants' list of site selection factors for 2011, gaining 7.4 percentage points over the 2010 Consultants Survey, with a 92.7 percent importance rating and ranking fifth among the factors. When rating this factor, perhaps the responding consultants have in mind large tracts, i.e., mega-sites, of shovel-ready or pre-certified sites. In fact, nearly 80 percent of the responding consultants consider the existence of such sites very or somewhat important (Slideshow, Chart Y).

Available buildings, however, is not as important to the responding consultants. This factor is ranked 16th, rated very or somewhat important by only three quarters of the responding consultants (Slideshow, Chart Z). The available buildings factor received an almost identical ranking from the 2011 Corporate Survey respondents. The sluggish economy has apparently increased the availability of facilities.

Energy availability and costs is considered quite important by the respondents to both our Corporate and Consultants surveys. The respondents to our 2011 Consultants Survey rank this factor sixth, with a combined 88.4 percent importance rating. More than 60 percent of the responding consultants say high energy costs are affecting their clients facility operations and/or supply/distribution network decisions (Slideshow, Chart AA), and about 70 percent say sustainable development is more important to their clients now than in the past (Slideshow, Chart BB). Three quarters of the respondents to our 2011 Consultants Survey say their clients are making energy-saving modifications to their existing facilities, and 40 percent of the respondents say their clients are seeking LEED certification for new or existing facilities, as well as recycling or re-using waste products (Slideshow, Chart CC).

Unfortunately, more than half of the responding consultants say communities are not offering specific "green" incentives. On the other hand, three quarters say their clients are not encountering "green performance" requirements as a stipulation for receiving incentives (charts DD and EE).

The respondents to our 2011 Consultants Survey also rate the tax-related factors high in importance. However, state and local incentives shows the largest decrease in the ratings from the 2010 Consultants Survey (8.5 percentage points), dropping from the first place spot in 2010 to seventh place in 2011. This seems strange since one of the consultants' primary responsibilities is to compare and negotiate for incentives on behalf of their clients. In fact, about half of the responding consultants say incentives are more important to their clients now than in the past (Slideshow, Chart FF). Forty-two percent of the responding consultants also say their clients consider tax incentives the most important type (Slideshow, Chart GG).

In line with that thinking, the consultants rank tax exemptions ninth among the site selection factors, considered "very important" or "important" by 86.9 percent of the respondents. In response to a related question, a quarter of the respondents to our 2011 Consultants Survey say their clients have had to repay incentives monies because investment and/or job creation obligations were not met (Slideshow, Chart HH).

Another tax-related factor - corporate tax rate - slipped down to 11th place in the 2011 Consultants Survey rankings, but is still considered "very important" or "important" by 85 percent of the respondents. The respondents to our 2011 Corporate Survey ranked corporate tax rate much higher among the factors; it's fourth on the corporate respondents' list, although its importance rating (86 percent) is in line with the consultants' rating. If we look back at what the consultants say with regard to the reasons behind their clients' relocation plans, only 16 percent cite high taxes; 41 percent of the Corporate Survey respondents cite high taxes as the reason behind a planned move.

Rounding out the consultants' top-10 list of site selection factors are occupancy and construction costs, ranked eighth with an 87.1 percent importance rating, and expedited or fast-track permitting, ranked 10th with an 86.4 percent importance rating. The consultants are cognizant of the need for speed when getting through the permitting process.

Some factors took an unexpected dive in the 2011 Consultants Survey rankings. It's odd that the consultants responding in 2011 consider the environmental regulations factor less important than those responding in 2010. This factor dropped 7.2 percentage points in importance and six places from 11th place in 2010 to 17th for 2011 with a 79 percent importance rating. And while the 2011 Corporate Survey respondents considered availability of long-term financing more important than those responding in 2010, the respondents to the 2011 Consultants Survey rated this factor as less important than the consultants taking the 2010 survey. Availability of long-term financing shows the largest decrease in importance (9 percentage points), ranking 21st with a 63 percent importance rating. The railroad service factor shows the second-largest decrease in the importance ratings (8.6 percentage points). Nonetheless, both these factors maintain their relative placement in the Consultants Survey rankings.

We also asked the consultants if their clients consider whether there are businesses performing similar activities to theirs in the area of search. Eighty-six percent say they do, and 81 percent say this factor is very or somewhat important (Slideshow, Chart II).

How Important Is Quality-of-Life?

The respondents to the 2011 Consultants Survey also rated the quality-of-life factors, which we rank separately from the other site selection factors. Based on their ratings, none of the quality-of-life factors would rank among the top-10 site selection factors.

Unlike the respondents to the 2011 Corporate Survey, the responding consultants do not say low crime rate is the most important quality-of-life factor. It is in the number-two spot with a 76.6 importance rating, and is edged out for first place by ratings of public schools, considered "very important" or "important" by 76.8 percent of the responding consultants - an 11.6 percent increase over the 2010 consultants' ratings. Again, the need to fill the nation's "skills gap" has put the focus on education.

Oddly enough, two quality-of-life factors that increased in importance according to the responding consultants are cultural opportunities (up 12.9 percentage points) and recreational opportunities (up 8.5 percentage points). The fact that the responding consultants count many more knowledge-worker firms among their clients (e.g., data- and computer-related, financial services, etc.) than represented by the Corporate Survey respondents may have something to do with the consultants' heightened focus on these quality-of-life issues.

Where Do the Consultants Get Their Information?

Three quarters of the respondents to the 2011 Consultants Survey rely on magazines like Area Development for their site selection information, as well as on economic data aggregators, including online resources. Half also say they use other financial publications as well as maintain their own site selection database. And nearly all (92 percent) use the Internet as a site and facility planning resource. When doing say, 84 percent of the responding consultants say they are seeking data on specific locations; three quarters are looking for contact information for economic development agencies; and 65 percent are perusing listings of available sites and buildings.

About a third of those responding to our 2011 Consultants Survey say that they go online looking for this information daily, with another third seeking this information several times a week - far more often than the 2011 Corporate Survey respondents who are not involved in location decisions on a daily basis. However, like the respondents to the 2011 Corporate Survey, 81 percent of the responding consultants say that between one and five locations usually make their clients' "short list," with 92 percent visiting the same number before making their final location decision. Eighty-five percent of the consultants also say their clients generally make a location decision within three months to one year of initial point of contact. (Answers to these questions are illustrated in the accompanying Consultants' Information Sources chart.)

Recent Project Announcements

SIP Manufacturing Plans Southaven, Mississippi, Operations

07/27/2026

Fortified Solar Expands Greenville County, South Carolina, Manufacturing Operations

07/27/2026

Canada-Based Swamp Rider Plans High Point, North Carolina, Production Operations

07/27/2026

Hepburn and Sons Plans Prince William County, Virginia, Headquarters Operations

07/27/2026

Relativity Space Expands Cape Canaveral, Florida, Production Operations

07/27/2026

Park Aerospace Plans Tulsa, Oklahoma, Production Facility

07/24/2026

Electra Plans Springfield, Ohio, Production Operations

07/24/2026

Taiwan-Based E Ink Expands Billerica, Massachusetts, Headquarters Operations

07/24/2026

Beehive Industries Expands Ohio Production Operations

07/24/2026

Redwire Expands Huntsville, Alabama, Production Operations

07/24/2026

Quality Companies Plans-Expands Louisiana Operations

07/20/2026

American Eagle Outfitters Plans Salisbury, North Carolina, Distribution Operations

07/20/2026

Australia-Based Detpak USA Plans Spartanburg, South Carolina, Production Operations

07/20/2026

SteelFab Expands Florence County, South Carolina, Operations

07/20/2026

Most Read

-

Rethinking Environmental Review

Q2 2026

-

The RFI Is No Longer the Starting Line

Q3 2026

-

21st Annual Shovel Awards: The American Industrial Economy Remade in Real Time

Q2 2026

-

Where Early-Stage Life Sciences Companies Get Stuck Scaling Their Real Estate—and How to Move Forward

Q2 2026

-

The Primary Problem

Q3 2026

-

Avoid These Red Flags, Deal Killers, and Blunders in Site Selection

Q2 2026

-

Why America's Largest Companies Are Investing in Skilled Trades

Q2 2026