Statutory tax rates only tell part of the story. While topline rates are important, and high rates may provide “sticker shock” for companies considering locating within a given state, they are just one component of an enterprise’s effective tax burden. Tax incentives, apportionment, throwback rules, and other factors often have a dramatic effect on effective tax burdens. In some cases, states with low statutory tax rates often impose high effective tax burdens, and vice versa.

A Recent Study

The recent study Location Matters – The State Tax Costs of Doing Business by the Tax Foundation in collaboration with KPMG LLP highlights state differences in tax costs (measured as Total Effective Tax Rate) for a variety of hypothetical operations. It compares tax burdens in the 50 states (plus the District of Columbia) considering seven different types of businesses: corporate headquarters, R&D facilities, retail, capital-intensive manufacturing, labor-intensive manufacturing, call centers, and distribution/warehouse operations. The study ranks states by tax costs for newly established operations (potentially triggering incentives) and mature operations (older than 10 years) in a Tier 1 city (major metro) and Tier 2 city (less than 500,000 in population) in each state.

For each different model, the study assesses the tax costs borne by a mature operation — one that is at least 10 years old — versus those borne by a new facility. The study assumes that mature operations are typically no longer eligible for tax incentive programs, while new facilities are generally eligible for most incentives. The study also focuses on firm types that are also very mobile, with the assumption that the owners and investors have considerable flexibility in where to locate or relocate based on factors ranging from taxes to labor force, making them frequent recipients of economic development subsidies and tax incentives.

Each of these companies is assumed to have out-of-state customers or clients. Thus, how each state apportions a company’s income is a critical factor in determining a state’s effective tax rate for that industry.

Manufacturing in the United States has generally been on the decline since the 1970s, when it accounted for one fifth of the labor force, with nearly 18 million manufacturing employees in 1977, according to the U.S. Census Bureau’s Census of Manufacturers. Intense foreign competition likely contributed to a reduction in U.S. jobs as companies expanded overseas. The decline of U.S. manufacturing hit its lowest point in 2010, in the aftermath of the Great Recession. Today, U.S. manufacturing appears to be rebounding due to factors such as increasing overseas wages (particularly in China, where manufacturing wages are considered to be higher than ever before), transportation costs and complexity, and relatively inexpensive investment costs available in the United States, perhaps due in part to state incentives.

Manufacturing is still a highly coveted industry, and its positive effect on a community is well understood. Manufacturing jobs are generally considered good jobs, and the income they generate for workers can, in turn, help bring revitalization to the local economy through a multiplier effect, including appreciating property values, increased revenue for school districts, and increased discretionary income and consumption. Many states offer generous incentive packages to win these jobs and the large capital investment that these projects bring. Two of the seven business scenarios studied in the Location Matters study are a capital-intensive manufacturer, such as a steel company, and a labor-intensive manufacturer, such as an auto or truck manufacturer. All manufacturing facilities are located in a Tier 2 city.

Income, Unemployment, & Property Taxes

The study indicates that while often substantial, business income tax burdens are just one part of the actual burden for new companies. Unemployment insurance tax burdens, particularly for labor-intensive manufacturing, are shown to be a significant cost. As an incentive for manufacturers, the majority of states offer some degree of sales tax exemption on manufacturing equipment, including five states that do not have a state sales tax at all and three that do not impose a sales tax on any equipment. While manufacturing equipment generally receives favorable sales tax treatment, property tax burdens vary considerably.

Property taxes are shown to be a significant factor for capital-intensive manufacturing operations, as they have a substantial amount of equipment potentially subject to tax. States that limit their property tax base to land and buildings, rather than taxing equipment and inventory, offer a lower tax environment for both capital-intensive and labor-intensive manufacturing firm types. Thirty-nine states offer some degree of property tax abatement for new capital-intensive manufacturers, and a few states go so far as to practically eliminate property tax liability over a 10-year period.

One interesting finding for new manufacturing companies is the positive impact of favorable apportionment factors and the absence of a throwback rule in computing the overall tax burden. In many cases, these two factors may be more important to a firm than considering a lower corporate income tax rate. For example, Colorado’s income tax rate is one of the lowest at 4.63 percent, yet Colorado’s income tax burden is one of the highest due to single sales factor apportionment and a throwback rule which exposes “nowhere income” attributable to states with which a firm lacks nexus to in-state taxation.

In our work with companies, we have often found that credits and incentives are one of the most important considerations for new companies and frequently prove to be a deciding factor to locate in a particular place. Substantial credits and incentives may often transform traditionally heavy tax burden states, such as New York and New Jersey, into attractive business climates for new manufacturing companies. Generally, however, the actual benefit from credits and incentives depends on a firm’s business needs. States with withholding tax rebates and jobs tax credits are likely more beneficial for new labor-intensive manufacturers, while investment tax credits and property tax abatements are generally more beneficial for new capital-intensive manufacturers.

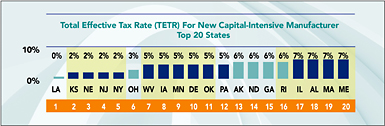

Incentives for Capital-Intensive Manufacturers: Louisiana and Kansas rank 1 and 2, respectively, among U.S. states for new capital-intensive manufacturers due to generous incentives such as the Quality Jobs withholding tax rebate program, industrial tax exemption, and inventory tax credit for Louisiana; and the High Performance Incentive Program, Promoting Employment Across Kansas (PEAK) program, and a sizeable property tax abatement for Kansas. Louisiana also benefits from having the lowest corporate income tax burden due to favorable apportionment factors and the absence of a throwback rule, as well as the second-lowest unemployment insurance tax burden. Kansas does not have favorable apportionment factors or the absence of a throwback rule, but it ranks well due to a low property tax burden, important to capital-intensive manufacturing companies, as well as a low corporate income tax burden, thanks to the High Performance Incentive Program, one of the most substantial investment tax credits.

Not surprisingly, states that lack property tax abatements have a higher tax burden, and several of these also impose a tax on inventory. Yet, among those that impose an inventory tax, Louisiana, Oklahoma, and Georgia offer generous credits and incentives that more than compensate for this specific tax burden.

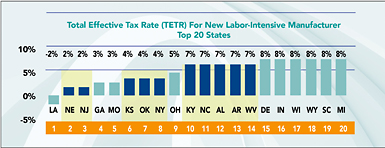

Incentives for Labor-Intensive Manufacturers: Louisiana again ranks number 1 for new labor-intensive manufacturers due to generous incentives such as the Quality Jobs withholding tax rebate program, industrial tax exemption, and inventory tax credit, as well as having the lowest corporate income tax burden due to favorable apportionment factors and the absence of a throwback rule, as well as the some of the lowest unemployment insurance and property tax burdens.

Generally, the states that perform well for labor-intensive manufacturing offset the costs associated with labor through substantial withholding tax rebates, such as the Nebraska Advantage Act Wage Credit, or generous jobs tax credits, such as the Grow New Jersey Assistance Program. Sixteen states offer withholding tax rebates, 24 states offer investment tax credits, and 24 states offer jobs tax credits to new labor-intensive manufacturers, which in some cases completely eliminate income tax burdens, at least for the first few years of operations.

Fighting to win back manufacturing jobs to the Garden and Empire states, New Jersey and New York have introduced the Grow New Jersey Assistance Program and the New York Excelsior Program, two of the most significant incentive programs currently available in the U.S. Effective beginning with the 2014 tax year, New York also applies a zero percent business income tax rate on qualifying manufacturers. These improvements have led New Jersey to move from 28 to 3 and New York to move from 26 to 8 for new labor-intensive manufacturing companies, since the previous Location Matters study.

In Sum

Manufacturing companies are starting to expand in the United States, thanks in part to competitive labor rates, reasonable business costs, and substantial state and local incentives. But just as manufacturing companies differ in their composition, such as labor-intensive or capital-intensive, states also differ in the types of taxes they impose and methodology in computing these taxes. In addition, each state applies different types of credits and incentives to help lower business costs and entice companies to invest in its state. A state with a low corporate income rate may create a substantial tax burden for a new firm, while a state with a high corporate income rate may, in actuality, impose only a minimal tax burden on the new investing firm.

States are also constantly changing their tax policies, as they compete for new jobs and investment. The decision to establish a manufacturing plant is a serious and costly one, generally requiring significant capital and a long-term commitment. It is critical that new manufacturing companies carefully assess all state and local costs of doing business before making a final decision.

Hartley Powell (whpowell@kpmg.com) is a Principal in the State and Local Tax practice of KPMG LLP in the Global Location and Expansion Services group; he is based in Charlotte, NC. David Padykula is an Associate in the State and Local Tax practice of KPMG LLP in the Global Location and Expansion Services group; he is currently based in Montreal, Canada. The GLES group provides U.S. and global site selection services. This article represents the views of the authors only, and does not necessarily represent the views or professional advice of KPMG LLP. The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be determined through consultation with your tax advisor. KPMG LLP, the audit, tax and advisory firm (www.kpmg.com/us), is the U.S. member firm of KPMG International Cooperative (“KPMG International”). KPMG International’s member firms have 162,000 professionals, including more than 9,000 partners, in 155 countries.