Signs of an economic recovery abound. The Department of Commerce Bureau of Economic Analysis announced that U.S. GDP grew 1.8 percent in the first quarter of 2011. The Department of Labor reported that unemployment rested at 9.0 percent at the end of April - a year-over-year decrease of 0.8 percent. And the Institute for Supply Management's Report on Business® showed that economic activity in the nonmanufacturing sector grew in April for the 17th consecutive month.

Yet, in context, GDP growth actually slowed from 3.1 percent during the fourth quarter of 2010. Unemployment crept up slightly in April (from 8.8 percent in March 2011), and the ISM nonmanufacturing index registered 52.8 percent in April, 4.5 percentage points lower than in March. The conclusion? Yes, things are improving - but slowly and with some bumps along the way. With this guardedly positive outlook for economic expansion, what is the expected impact on the supply chain, also known as the logistics network?

The supply chain consists of suppliers, manufacturing centers, warehouses, distribution centers, and retail outlets, as well as raw materials, work-in-process inventory, and finished products that flow between the facilities. Fierce competition in today's consumer markets is forcing business enterprises to invest in and focus on these variables. In fact, managing logistics has become a major point of focus and differentiation - and the process is increasingly complex. More demand, more shipments, more jobs and more traffic - these issues must be anticipated, prepared for, and taken advantage of for a company to be successful in today's market. Some would argue that the supply chain is not ready.

Logistics Costs on the Rise

Logistics costs are rising now and sure to rise more in the near term. The cost of the U.S. business logistics system declined 18.2 percent in size in 2009 - the largest drop in the history of the Council on Supply Chain Management Professionals' State of Logistics Report®. Add to that a notable drop in 2008, and total logistics costs declined $300 billion during the recession. In fact, 2009 logistics costs as a percent of the nominal GDP hit a historic low of 7.7 percent. This historic low is unsustainable.

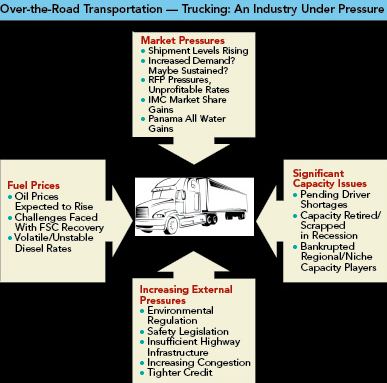

Consider the trucking industry. For domestic distribution, trucking is responsible for 80 percent of all product movement in the United States, followed by rail and then marine transport. Truck freight tonnage in 2010 increased by 6 percent, compared to 2009, while spot market load volume more than doubled.

This "good news" of improvement is accompanied by "bad news." The economic downturn saw load counts for over-the-road shippers reduced by between 30 and 45 percent. By early 2009, carriers were clamoring to compete for limited loads, causing market rates to plummet further, and reducing carrier margins to the point where they could just barely keep their doors open.

As 2009 progressed, many carriers reduced staff and sold excess equipment. Driver capacity was further diminished because many leased operators simply could not afford to pay their bills. As a result, there are 142,000 fewer drivers now than in 2007, according to Con-Way, with a possible net reduction of 400,000 by 2012. Add to that tightening regulations, higher overhead, and increasing highway congestion, and it's easy to see that trucking is an industry under significant pressure.

Now, as demand has started to recover, carriers have been forced to begin increasing rates. By mid-2010, trucking rates in many regions had increased by a factor of 30 to 65 percent over 2009. Currently, we are seeing very tight capacity within the marketplace, with closer to 95 percent of trucks in use. Pricing power will continue to gradually shift from the shipper to the carrier in this new reality.

Fuel prices also will play a key role. Should prices return to the record-breaking levels of 2008, when diesel was $4.78 per gallon and barrel prices were in the $150 range, it could lead to a major jump in transportation costs across the board.

What Happens Next?

The anticipated rise in costs will impact distribution facility networks significantly. On average, the amount of space will increase, the number of distribution centers will rise, and the average distribution center size will be incrementally smaller.

Facilities will be located closer to population centers, overall. Population density will more closely align with distribution square feet density. As networks are defined, average distance to customer will be the most important variable. Many industry experts anticipate that demand will soon outstrip existing inventory supply, which will place upward pressure on rents.

Additionally, with regard to skyrocketing fuel costs, we may see a return to the past in which fuel consumption patterns forced shippers to consider things like bringing more manufacturing operations closer to home - a practice also commonly referred to as near-shoring or near-sourcing.

Recently, in an effort to anticipate the impact of higher transportation costs, Cushman & Wakefield chose the top 82 industrial markets as options in a network model, with population as the proxy for demand. The model "optimized" for a distribution center network servicing the United States. We ran scenarios for anywhere from one to 15 distribution centers, trying to do diligence around the effect of rising transportation costs on networks and industrial markets. We used market-to-market freight rates, meaning they were rate- and equipment-level specific, and we ran the model for outbound shipments only. We did not model other costs, which are significant, such as labor, occupancy, and utilities.

For industrial markets to perform well in this forward-looking exercise, they need to be in more dense markets, have good access to population in an immediate proximity or region, and have expected freight rates that are reasonably beneficial.

Interestingly, Indianapolis was the chosen location for a single-distribution-center model. In this model, this location offers the lowest weighted average distance and freight-rate-based transportation cost to an American household if only one distribution center were allowed.

Increasing the target number of distribution centers, Los Angeles was the most commonly chosen distribution hub, and Sacramento, Newark (NJ), Houston, Seattle, Chicago, Oklahoma City, and Tampa also performed well. As fuel costs increase, these are the markets potentially better positioned to benefit as users shift their distribution center composition. Beyond Trucking

Looking forward, container volumes are rising as world trade recovers. Additionally, U.S. exports are strong. This translates into increases in outbound containers loaded with machinery and semi-finished goods. Agricultural products, in containers or dry bulk form, have been flowing from the United States to the four corners of the globe, helped by the weak dollar and strong demand.

Coupled with the high fuel prices and strong regulatory and driver constraints on trucking, we foresee greatly recovered demand for port-proximate space. This will increase the need to be intermodally served. Traditional port cities such as Savannah, Norfolk, Charleston, and Los Angeles will see growth, as will emerging gateways like Jacksonville, Miami, and Prince Rupert, British Columbia.

New East Coast-to-Midwest rail corridors and the Panama Canal expansion in 2014 will drive special advantage to the Atlantic ports. Markets that will see dampened growth due to the Panama Canal effect include the port of Los Angeles, as well as the land-bridge markets of Chicago, Indianapolis, and, potentially, Columbus (OH). Additionally, user demand will likely result in smaller physical requirements on the West Coast and larger requirements on the East Coast.

Network Shifts: Easier Said Than Done

Today's unprecedented volatility in logistics variables, and in the commercial real estate market, is creating challenges and opportunities for U.S. companies. While many decision-makers, understandably, adopted a "wait and see" position late in 2008, now may be the best time to make supply chain strategy shifts that capture the upside of this unique climate, in both the logistics and the real estate markets.

Yet sweeping network changes can be challenging. They require capital investment. They generate asset and personnel changes and potential costs of migration. They can disrupt business flow. And new space commitments can lessen flexibility. In short, the value of change and the certainty that things will change again makes the ROI of network changes less clear.

The multiple conflicting priorities surrounding location and market selection - including labor, real estate, incentives, and others - must be managed concurrently. Take labor, for example. Generally speaking, preferred industrial labor pools - those with greater densities of target workers to support industrial operations and lower occupancy costs - typically are further from population centers. Generally speaking, moving your operations closer to the city, to reduce transportation costs, could represent significant employment risk.

What To Do?

It is not an easy time to be a supply chain executive. Finding solutions to reduce costs and raise service levels is concerning company boardrooms today more than at any time in recent history. The question is, what do you do, when do you execute, and what is it worth?

Oftentimes, it helps to know what other companies are doing. At Cushman & Wakefield, we are seeing several major trends emerging in clients' approaches to and prioritization of industrial location decisions. They include:

- The rising importance of transportation costs and infrastructure (i.e., getting closer to customers and suppliers), with an emphasis on the value of mode flexibility

- More attention paid to the quality and availability of critical labor profiles and skills, with some types of labor becoming scarcer and human resources being an increasing point of competitive differentiation

- An increasing priority in location decisions on per-unit utility costs, in a U.S. market where utility cost variances by geography can be significant

- A jump in less-than-optimal decisions (from a locational perspective) being made in order to catch real estate opportunities

- Shifting of manufacturing location decisions from "offshore" to "near shore," i.e., Mexico and/or the U.S. Southeast, as labor cost arbitrage available in China, India, etc. has a declining marginal value for some companies

For every company, though, it is critical to quantify and understand the cost of change and the value of change. A sophisticated network study can answer these questions. It does not take long or cost much to understand the various options. If a company decides to stay on the sidelines during this market opportunity, when so many variables are in transition, they should at least know the present value of their decision not to act.