Frontline: Sale-Leasebacks Allow Companies to Redeploy Capital

Q2 2016

One recent example was Smithfield Foods Inc.’s $43 million sale and leaseback of a new, 419,052-square-foot cold storage distribution center in Greenfield, Ind. Centurion Investments, LLC, a private real estate investment firm based in Arlington, Va., acquired the property and is leasing it back to a subsidiary of Smithfield.

When the deal was announced earlier this year, Smithfield’s Vice President and Corporate Treasurer Tim Dykstra said the sale-leaseback would allow the company to “redeploy capital and fund strategic initiatives to further enrich our core business offerings” — in other words, use the money where it would do the most good.

When Smithfield built the facility, the company was unsure whether it wanted to keep it long-term or sell it, according to Cushman & Wakefield Vice Chairman Scott Goldman, who helped with the deal. But, the current low-interest-rate environment, combined with strong investor demand for state-of-the-art facilities occupied by solid credit tenants, made for an “excellent” opportunity for Smithfield, Goldman says. Along with freeing up capital, a lease transfers the risk associated with ownership to the investor/owner, according to Goldman.

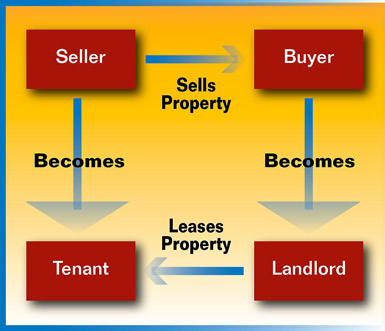

Investors and institutions consider corporate real estate that is leased back to the seller a solid investment. Unique Challenges

The Smithfield deal was not without challenges, Goldman says, noting, “every major project presents unique issues and challenges. Before closing, we had to negotiate easement rights over a nearby water tower. However, there weren’t any monumental setbacks that prohibited Smithfield and Cushman & Wakefield from executing the transaction as planned.“

According to Goldman, the sale-leaseback strategy is suitable for credit-worthy corporate users that occupy high-quality, state-of-the-art facilities and are interested in redeploying capital toward expansion and other higher-return projects. It’s also an excellent exit strategy for companies, he notes.

Investors and institutions consider corporate real estate that is leased back to the seller a solid investment. In the single-tenant, sale-leaseback market there are a number of significantly funded institutional, public, and private groups that exclusively purchase and own single-tenant assets. “It’s a very ‘niche’ market,” Goldman says. Buyers include private and public REITS, private investors, and institutional and foreign investors.

Creative Deal Structuring

In some situations, however, more creativity in deal structuring is required due to specific factors. One example of flexible, creative deal structuring is development financing, which occurs when the sale-leaseback of an existing building that was already under construction is executed. This is a more inclusive approach for a seller and involves a hands-on investor that can buy the land, develop it into a tailored asset, and lease it back to the seller.

Another example of a creative deal structure includes earn-out security deposits; this is a credit-based agreement that eliminates uncertainty for the buyer by linking the risk and return directly to the performance and earnings of the tenant.

-

Dan Emerson, Staff Editor, Area Development

Based in Minneapolis, Dan Emerson has been a freelance writer for business, trade, and consumer publications since 1994.

Logistics / Infrastructure

Frontline: Red Sea Pharma Crisis Pushing Logistics Advancements

-

Logistics / Infrastructure

Front Line: Solutions Needed for Truck Driver Shortage

-

Labor Costs / Organized Labor

Front Line: Impact of the Latest Minimum Wage Increases

-

Sustainable Development

Front Line: Electrification of Industrial Processes

Project Announcements

Kikkoman Foods Plans Jefferson, Wisconsin, Operations

04/26/2024

BWX Technologies Expands Cambridge, Ontario, Nuclear Production Operations

04/26/2024

Greenheck Group Plans Knoxville, Tennessee, Operations

04/26/2024

Local Bounti Plans Pasco, Washington, Indoor Agricultural Operations

04/26/2024

Innovative Construction Group Plans Siler City, North Carolina, Production Operations

04/26/2024

Crystal Window and Door Systems Plans Mansfield, Texas, Headquarters-Production Operations

04/25/2024

Most Read

-

2023's Leading Metro Locations: Hotspots of Economic Growth

Q4 2023

-

2023 Top States for Doing Business Meet the Needs of Site Selectors

Q3 2023

-

38th Annual Corporate Survey: Are Unrealized Predictions of an Economic Slump Leading Small to Mid-Size Companies to Put Off Expansion Plans?

Q1 2024

-

Making Hybrid More Human in 2024

Q1 2024

-

Manufacturing Momentum Is Building

Q1 2024

-

20th Annual Consultants Survey: Clients Prioritize Access to Skilled Labor, Responsive State & Local Government

Q1 2024

-

Public-Private Partnerships Incentivize Industrial Development

Q1 2024