When you examine levels of manufacturing employment in 1992, 2002, and 2012, Ross Perot looks like a prophet. All told, the United States lost approximately 1.5 million manufacturing jobs during the 1990s. To add to the catastrophe, the United States lost another 3.5 million jobs during first decade of the 21st century (Figure 1).

Some of the manufacturing loss may have been attributed to one-sided trade agreements, as Perot suggested during his campaign. However, other factors contributed to this unsettling outcome; for one, the strong dollar during the 1990s made imports cheap. Management also gave lucrative contracts to labor unions and agreed to specialized work rules that later handcuffed the manufacturing industry. And until Toyota introduced its lean manufacturing techniques, companies were comfortable holding larger amounts of inventory to cushion disruptions in the supply chain.

Recently the employment picture in the United States has started to change. During the past two years, the United States has added approximately 370,000 new jobs; by 2015, some experts predict that the United States could add a total of 1.1 million new manufacturing jobs (Figure 2).

Repatriating Manufacturing

Some attribute stabilization and growth forecasts in the manufacturing sector to a new phenomenon that is more and more frequently referred to as "in-sourcing." In a January 2012 report on Investing in America - Building an Economy that Lasts, The White House describes in-sourcing as "bringing activities and jobs back to the U.S. or choosing to invest in the U.S. instead of overseas."

According to recent surveys, U.S. companies are looking to repatriate their manufacturing. In a study by David Simshi-Levi, an engineering professor at MIT who runs a program for supply chain executives, 14 percent of companies surveyed indicate certain plans to move at least a portion of their manufacturing back home. In an earlier survey, the executives at the Boston Consulting Group found that 37 percent of 106 companies surveyed planned to re-shore or were actively considering the option.iv

Anecdotally, we are seeing the same results in recent news accounts. At this year's North American Auto Show in Detroit, Honda, Nissan, Toyota, and BMW announced plans to use the United States as an export base. Honda announced that it would export as many as 400,000 vehicles from the United States, while Toyota said that the 100,000 vehicles exported in 2011 are just the tip of the iceberg.

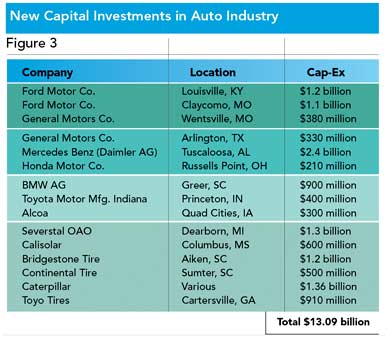

New Capital Investments

The auto industry, if not explicitly endorsing "in-sourcing," has supported the movement with almost $14 billion in new capital investments. Of the 15 largest projects receiving a CICI Award for Corporate Investment in 2011, eight projects were related to the auto industry. Notable projects are as follows:

- Ford Motor Co. invested $2.3 billion in two plants near Louisville and one in Kansas City. The investment in Louisville Assembly and Kentucky Truck will create 3,100 new jobs, while the investment in Kansas City will create 1,600 jobs over the next four years. One of the notable mentions in the press release is that Louisville Assembly has become one of Ford's most flexible, high-volume and state-of-the-art production facilities.

- Not to be outdone, General Motors announced not long ago that it was re-opening its Wentzville, Missouri, facility and investing $380 million to build the new Chevrolet Colorado mid-size pickup as well as the Chevy Express and GMC Savana vans. The investment will create 1,650 production jobs at the facility.

- Daimler announced that it would be investing $2 billion in Vance, Alabama, to add a fifth model to that production facility. The new investment will create 400 new jobs. Suppliers, following the lead of their OEM customers, have placed big bets in the United States:

- Bridgestone is investing $1.2 billion in Aiken, South Carolina.

- Continental is investing $500 million in Sumter, South Carolina.

- Michelin is investing $750 million in Lexington, South Carolina.

- Severstal is investing $1.3 billion in Dearborn, Michigan (Figure 3).

What's Driving In-Sourcing?

There are five primary factors driving "in-sourcing" in the U.S. auto industry:

- 1. Favorable exchange rates - The Wall Street Journal has reported that favorable exchange rates are helping the United States become a competitive producer of cars and trucks and a favored location for making vehicles for exportation to markets around the world.vi In 2002 one U.S. dollar purchased 133 Japanese yen, while today that same dollar purchases only 82 yen. The same is true with the euro, as today one dollar buys 0.75 euros compared to 1.14 euros a decade ago. Honda, BMW, and VW have publicly stated that they believe the exchange rate will remain relatively low for a while. Additionally, Honda's changing production behavior and North America's increased capacity for handling production for Toyota Motor Corporation and Nissan Motor Company signal a longer-term move by Japan's automakers to protect against currency-related losses.

- 2. Competitive labor costs - Two key components explain why the U.S. labor force proves more competitive: increasing U.S. worker productivity and increasing Chinese labor costs.

According to The Boston Consulting Group, worker productivity has been growing faster in the United States than in Western Europe and China. From 2005 to 2010, worker productivity in the United States grew 2 percent per year, while the major economies of Western Europe averaged only 0.4 percent productivity growth. Compared with China, U.S. workers are nearly three times more productive. In 2010 real output was $120,000 per worker in the United States versus $35,000 per worker in China. In fact, U.S. manufacturing output has increased by more than 2.5 times since the 1970s - even though the labor force is 30 percent smaller.

In 2000, when the "giant sucking sound" shifted to China, factory wages in China were only $0.52 per hour. According to The Boston Consulting Group, labor costs have been increasing by 18 percent per year in China versus 4 percent in the United States for the same period (2005 to 2010); it should also be noted that labor costs have stalled in the United States since 2010. By 2015, the average fully loaded hourly wage in China will reach $4.50 per hour. In the Yangtze River Delta, where autos and electronics are produced, the hourly rate will rise to $6.30 per hour. Even though Chinese productivity is increasing by about 8.4 percent per year, their productivity is not rising fast enough to offset wage increases of 18 percent per year. The Boston Consulting Group estimates that by 2015, the total labor-cost savings of manufacturing goods in China will be only 10 percent to 15 percent when factoring in productivity-adjusted labor. - 3. Logistics costs - The 10-15 percent labor savings is not enough to offset China's logistics costs, which are now 18 percent of its GDP. Moreover, the total cost of China's logistics rose by 18.5 percent in the first half of 2011 due to the rising price of raw materials, labor, and lending rates. Transportation costs rose by 15.5 percent, storage costs soared 22.7 percent, and interest-related expenses jumped 24 percent. China's logistics costs are more than double the average in Western Europe, Japan, and the United States. Not only are logistics costs high, but also the recent floods in Thailand and the tsunami in Japan demonstrate the prudence of mitigating risks in the supply chain associated with natural disasters.

- 4. Regional manufacturing strategies - China is its own giant consumer market, and U.S. executives are more and more frequently faced with a choice: (1) expand Chinese factories to manufacture goods for both U.S. and Chinese markets or (2) expand U.S. factories for the U.S. market and dedicate Chinese production exclusively to Chinese markets. Dr. Simchi-Levi noted that "companies are moving toward a regional-manufacturing model in which Asian plants serve Asian customers; North American ones serve Americans."xi

- 5. Well-established supplier networks - Dr. Simchi-Levi further noted that established expertise and supplier networks are rather difficult to move. Fortunately, automotive suppliers are already well-entrenched in the United States. Some of the more progressive communities are linking R&D, engineering centers, and production centers.

A good example is ICAR and its 250-acre integrated research park. According to Dr. Thomas Kurfess, a professor at Clemson and BMW Chair of Manufacturing, "Our faculty team of world-class engineers has developed a first-class research and educational program in Automotive Engineering that focuses on the vehicle from a systems integration perspective. Under the rubric of systems integration, we concentrate our education and research programs on product design and development, manufacturing, and electronic systems."

Next: What three things companies should consider when making an automotive site selection decisionMaking a Site Selection

All of this talk about in-sourcing can better inform future site selection activity. When deciding where to locate new facilities, companies should consider three things:

- 1. If companies are willing to repatriate projects where labor content is less than 25 percent of the total manufacturing costs, and if labor productivity is key to their competitiveness, then they should look at states and local communities with a highly skilled work force capable of handling their jobs. In addition, states that encourage flexibility in their work rules will foster companies' productivity.

- 2. To enhance the productivity of workers, companies are investing large sums in capital-intensive equipment. They should look for states and local communities that reward these investments by lowering property taxes associated with personal property. Remember the economic axiom: "If you tax something, you receive less of it."

- 3. Since the goods that will be manufactured in the United States have lower labor content but relatively higher logistics costs (i.e., steel, aluminum, and plastics), efficient and reliable infrastructure is critical. One of the reasons that Toyota, Honda, and Ford are investing in the United States is that their production in Thailand was shut down for an extended period of time because the floods disrupted both their supply chain and their actual production operations. Good freeway access, efficient rail yards (with dual access to multiple carriers), and a port with efficient and predictable labor relations are essential to efficient management of logistics costs.

It's an exciting time again in the automotive industry. For all of those who bled during the dark days of 2009 and 2010, it's especially nice to hear what one might describe as a louder sucking sound right here at home.