Meanwhile, commodity prices continue to drag on the economies of the Oil Patch and Plains States. Still, only four states are in recession as of January — Alaska, North Dakota, Wyoming, and West Virginia. All of them are energy producers.

Manufacturing outside of the energy regions is less of a drag now on local economies than one month ago, and homebuilding and home sales remain one of the most important economic drivers across all of the country.

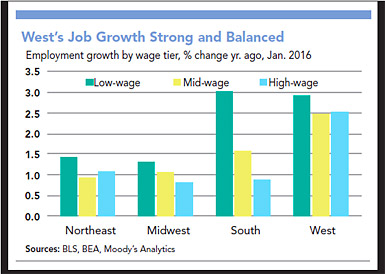

The West leads in the pace of job growth, but it also leads in terms of the types of jobs being created. Its growth is evenly spread across the range of income streams that outpace those of nearly all other regions of the country. Thus aggregate income growth far outpaces that of the other three regions from the combination of the absolute rate of job growth and the even mix of jobs across the spectrum of skills and wage rates.

While job growth in the South is well ahead of that in the Northeast and Midwest, its aggregate wage and salary income growth is no different than that of the other two because the South’s job creation is heavily concentrated in low-wage industries. The South’s mix of jobs is also shaped by the loss of mid- to high-wage jobs in energy and related manufacturing and services.

Manufacturing Rebound

A rebound in manufacturing is in sight, however. The regional Federal Reserve surveys of purchasing managers have turned more positive since February. New orders are improving rapidly, and indicators of production, backlogs, and trade have generally improved modestly. The most disappointing component of the surveys has been employment, which will be the last to turn around. The greatest losses have been concentrated, however, in the Oil Patch. Smaller losses have occurred in the Plains States, and even fewer in the Great Lakes States. The Southeast has shown the most resilience as auto production and demand for construction materials has risen.

Trade

The impact of soft global trade adds to the weakness of the midsection of the country. The fall in demand and price for agricultural goods compounds the fall of energy commodities in the region, and much of its manufacturing is tied to domestic and global demand for agricultural equipment and supplies. Further, the primary destination for much of the region’s goods is Canada, where the economy is weak and the currency has weakened by 11 percent versus the dollar over the past year, and 36 percent from its peak in mid-2011. The Great Lakes States, on the other hand, have not suffered greatly from global markets. With more diverse export destinations and its domestic market tied to demand for consumer goods such as autos and light trucks, as well as for aerospace and construction-related goods, the industrial Midwest has weathered the lull in manufacturing over the past year rather well.

Still, only four states are in recession as of January — Alaska, North Dakota, Wyoming, and West Virginia. All of them are energy producers. Outlook

The West and Southeast will remain the strongest economies in the coming year, but there is a good chance the Southeast will outperform the West. Equity market volatility and caution among venture capital funds are likely to slow the pace of growth of new enterprises in tech-producing areas of the West. Combined with the high costs and tight labor markets in places such as the San Francisco Bay Area, this means growth will continue but at a slower pace.

Without such constraints and with improving population growth and housing markets, the Southeast is poised to challenge the West as the leading region of the country, at least for job growth. Income growth will likely remain the strongest in the West given its better mix of job creation across industries and wage tiers.

The industrial Midwest should remain stable. Many manufacturing industries will benefit from improved demand and an ultimate reduction of inventories so that production will rise.

The oil- and commodity-producing regions of the nation’s central corridor are likely at their nadir. Energy prices have rebounded from cyclical lows, although they have not yet breached break-even values that would entice a return to new exploration. That likely will take at least another year.

Slower income growth will keep the Northeast from breaking out of its current slow pace of growth.