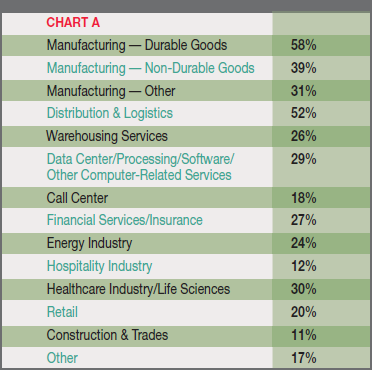

Chart A - Percentage of Respondents Who Have Worked on Projects in the Following Industries(1 of 31)

More than 50 percent of the responding consultants say they have worked on projects for durable good manufacturers as well as for distribution/logistics firms. About a third have also worked with non-durable goods and other manufacturers, as well as with those in the healthcare/life sciences industries and those who provide data - and computer-related services

Next: Chart B - Primary Services Required by their Clients

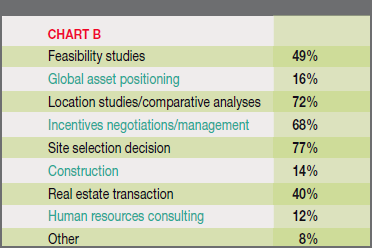

Chart B - Primary Services Required by their Clients (2 of 31)

More than 70 percent of the respondents to our Consultants Survey say they are providing location studies/comparative analyses to their clients; two thirds are negotiating and managing incentives on their clients' behalf; and 40 percent handle their clients' real estate transactions.

Next: Chart C - In Terms of their Employment Numbers, Client Companies Utilizing Consultants' Services

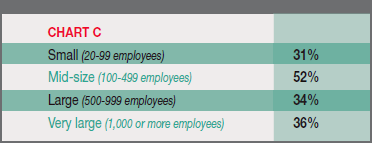

Chart C - In Terms of their Employment Numbers, Client Companies Utilizing Consultants' Services (3 of 31)

About half of the respondents say they work primarily with mid-size firms in terms of their employment numbers (100-499), while more than a third also work with companies employing 500 or more people.

Next: Chart D - Departments of Clients' Organizations that Are Significantly Involved in the Site Selection Process

Chart D - Departments of Clients' Organizations that Are Significantly Involved in the Site Selection Process (4 of 31)

The respondents to our 9th Annual Consultants Survey also say they work with their clients' real estate (63 percent), tax and finance (54 percent), and other business unit management (55 percent).

Next: Chart E - Clients Who Ask Consultants to Perform a Location Search Have

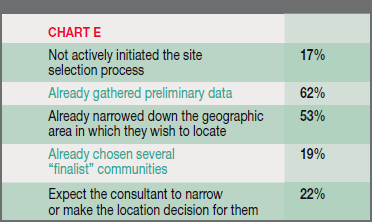

Chart E - Clients Who Ask Consultants to Perform a Location Search Have (5 of 31)

More than 60 percent of the responding consultants say their clients have gathered preliminary data prior to engaging their services. About half also say their client firms have narrowed down the geographic area in which they wish to locate, and a fifth actually claim their clients defer to them on the final location decision.

Next: Chart F - Expect the Economy to Improve Significantly By

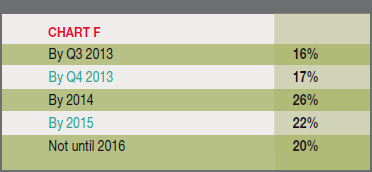

Chart F - Expect the Economy to Improve Significantly By (6 of 31)

The consultants who responded to our survey are slightly more optimistic about the state of the economy than the respondents to our 27th Annual Corporate Survey: 33 percent of the consultants expect the economy to improve by the end of this year

Next: Chart G - Effects of the Sluggish Recovery on Clients' Facility Plans

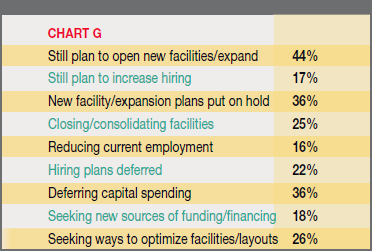

Chart G - Effects of the Sluggish Recovery on Clients' Facility Plans (7 of 31)

A third of the responding consultants also acknowledge that some clients are putting facility plans on hold and deferring capital spending as a result of anemic economic growth.

Next: Chart H - Most of the Clients that Expect to Open New Facilities Plan to do so Within

Chart H - Most of the Clients that Expect to Open New Facilities Plan to do so Within (8 of 31)

A quarter of the respondents to our 9th Annual Consultants Survey say most of their clients who expect to open new facilities plan to do so within one year; more than half say their clients will open new facilities within two years.

Next: The Number of New Facilities the Average Client Plans to Open

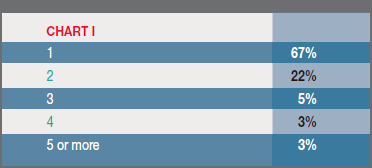

Chart I - The Number of New Facilities the Average Client Plans to Open (9 of 31)

Two thirds of the responding consultants also say their clients will open just one new facility.

Next:Chart J - The Domestic Location Projects Consultants Are Working on Are Slated for the Following Regions (as a percentage of total new domestic projects)

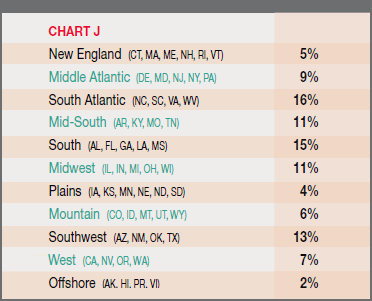

Chart J - The Domestic Location Projects Consultants Are Working on Are Slated for the Following Regions (as a percentage of total new domestic projects) (10 of 31)

The respondents to our Consultants Survey are primarily working on domestic projects slated for the South Atlantic - North Carolina, South Carolina, Virginia, West Virginia (16 percent of the projects); the South - Alabama, Florida, Georgia, Louisiana, Mississippi (15 percent); and the Southwest (Arizona, New Mexico, Oklahoma, Texas (13 percent).

Next: Chart K - Types of New Domestic Facilities Clients Are Opening (as a percentage of total new domestic projects)

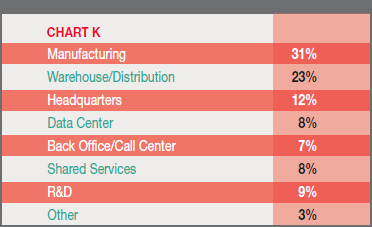

Chart K - Types of New Domestic Facilities Clients Are Opening (as a percentage of total new domestic projects) (11 of 31)

When considering all of the new domestic facilities projects the responding consultants are working on, about 30 percent will be manufacturing plants and a quarter will house warehouse/distribution operations

Next: Chart L - The Foreign Location Projects Consultants Are Working on Are Slated for the Following Regions (as a percentage of total new foreign projects)

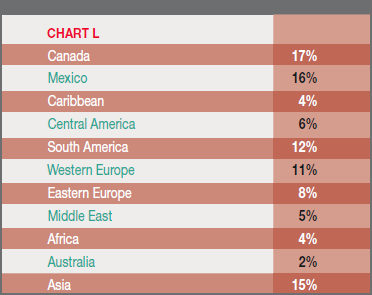

Chart L - The Foreign Location Projects Consultants Are Working on Are Slated for the Following Regions (as a percentage of total new foreign projects) (12 of 31)

As for expected new foreign facilities, the respondents to our Consultants Survey say many of the ones they are working on will be in Canada (17 percent) as well as Mexico (16 percent); 15 percent in Asia; and more than 10 percent in Western Europe as well as South America.

Next: Chart M - New Facilities Planned for Asia Will Be Located in the Following Locations (as a percentage of total new Asian projects)

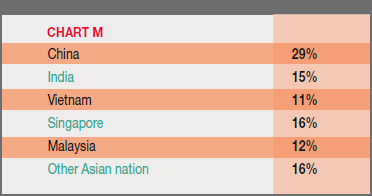

Chart M - New Facilities Planned for Asia Will Be Located in the Following Locations (as a percentage of total new Asian projects) (13 of 31)

The respondents to our 27th Annual Corporate Survey also slated more than 10 percent of their foreign projects for each of these latter two regions, but far fewer for our neighbors to the north and south. Of those clients' projects slated for Asia, China will garner the largest share - 29 percent.

Next: Chart N - Types of New Foreign Facilities Clients Are Opening (as a percentage of total new foreign projects)

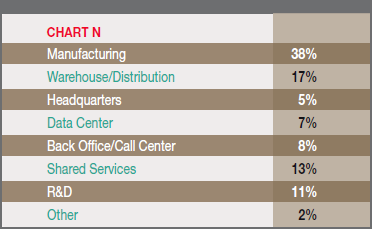

Chart N - Types of New Foreign Facilities Clients Are Opening (as a percentage of total new foreign projects) (14 of 31)

More than a third of the responding consultants' clients' new foreign facilities will be manufacturing operations, with 17 percent expected to house warehouse/distribution centers.

Next: Chart O - Number of Companies Establishing Foreign Facilities as Opposed to Domestic Ones

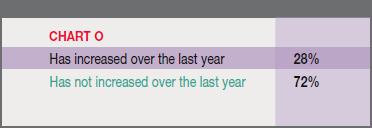

Chart O - Number of Companies Establishing Foreign Facilities as Opposed to Domestic Ones (15 of 31)

Twenty eight percent of the consultants say they have seen an increase in the number of companies establishing foreign facilities as opposed to domestic ones.

Next: Chart P - Clients Expect to Relocate a Foreign Facility Back to the U.S.

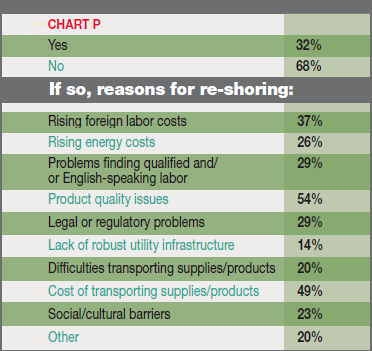

Chart P - Clients Expect to Relocate a Foreign Facility Back to the U.S. (16 of 31)

More than a third cite rising foreign labor costs, and nearly 30 percent say their clients are encountering rising energy costs as well as having problems finding qualified and/or English-speaking labor.

Next: hart Q - Most Clients that Expect to Relocate Facilities Plan to do so Within

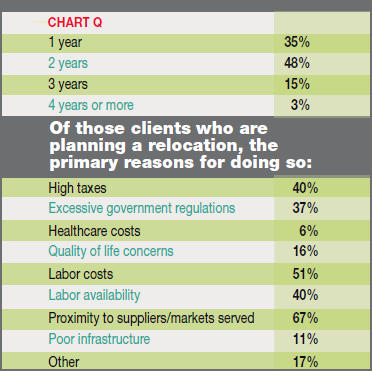

Chart Q - Most Clients that Expect to Relocate Facilities Plan to do so Within (17 of 31)

Of their clients planning relocations, proximity to suppliers/markets served as well as the need to lower labor costs, seems to be driving the decision.

Next: Chart R - Issues Preventing Clients from Spending More of their Earnings on Investment in U.S. Facilities

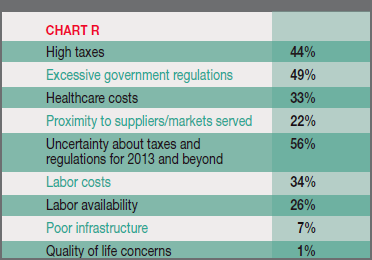

Chart R - Issues Preventing Clients from Spending More of their Earnings on Investment in U.S. Facilities (18 of 31)

When asked why their clients are not spending more of their money on investment in U.S. facilities, about half of the responding consultants blamed high taxes and excessive government regulations, as well as uncertainty about taxes and regulations for 2013 and beyond.

Next: Chart U - High Unemployment Rates Are Making it Easier for Clients to Find the Necessary Labor

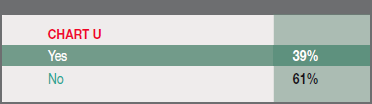

Chart U - High Unemployment Rates Are Making it Easier for Clients to Find the Necessary Labor (19 of 31)

The responding consultants agree with the Corporate Survey respondents in that 61 percent say unemployment rates are not making it easier for their clients to find the labor they need.

Chart V - Many Unemployed are Lacking

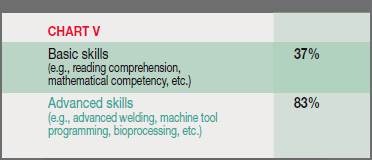

Chart V - Many Unemployed are Lacking (20 of 31)

More than 80 percent of the consultants also say the unemployed are lacking the advanced skills their client companies require.

Next: Chart W - Clients' Dependency on Contract Workers or Contingent Labor

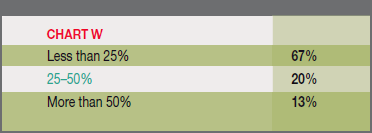

Chart W - Clients' Dependency on Contract Workers or Contingent Labor (21 of 31)

This may be why only 49 percent of the respondents to our Consultants Survey rate availability of unskilled labor as "very important" or "important," similar to our corporate respondents, and placing this factor 24th in priority. Nevertheless, fully two thirds of the responding consultants believe that their clients are less than 25 percent dependent on contract or contingent labor.

Next: Chart X - Importance of the Existence of an Available Building in Clients' Site Searches

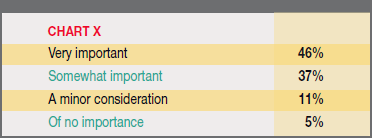

Chart X - Importance of the Existence of an Available Building in Clients' Site Searches (22 of 31)

More than 80 percent claim the existence of an available building is very or somewhat important in their clients' site searches.

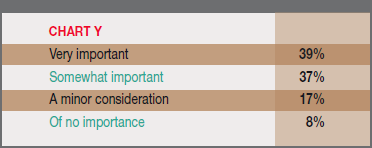

Next: Chart Y - Importance of the Existence of a Shovel-Ready/Pre-Certified Site in Clients' Site Searches

Chart Y - Importance of the Existence of a Shovel-Ready/Pre-Certified Site in Clients' Site Searches (23 of 31)

More than three quarters affirm the importance of a shovelready or pre-certified sites.

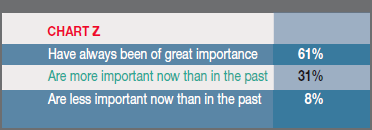

Next: Chart Z - Relative Importance of Incentives to Clients when Making Location Decisions

Chart Z - Relative Importance of Incentives to Clients when Making Location Decisions (24 of 31)

Sixty one percent of the consultants say incentives have always been of great importance to their clients.

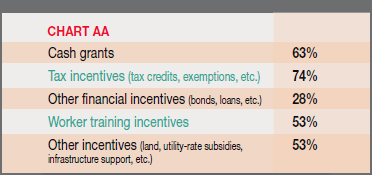

Next: Chart AA - Type(s) of Incentives Clients Consider Most Important when Making a Location Decision

Chart AA - Type(s) of Incentives Clients Consider Most Important when Making a Location Decision (25 of 31)

Three quarters of the responding consultants say tax credits, exemptions, and the like are most important to their clients, and more than half say worker training incentives are equally important.

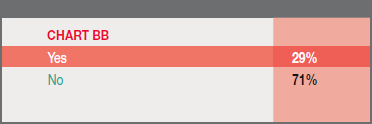

Chart BB - Clients Have had to Repay Incentives Monies because Investment and/or Job Creation Obligations Were not Met:

Chart BB - Clients Have had to Repay Incentives Monies because Investment and/or Job Creation Obligations Were not Met (26 of 31)

Unfortunately, almost 30 percent of the consultants claim that their clients have had to repay incentives monies because job creation or investment obligations were not met

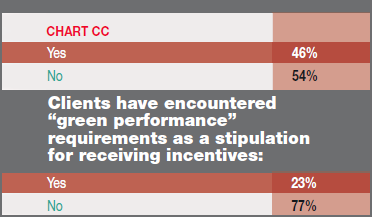

Next: Chart CC - Communities are Offering Specific Incentives for "Green" Initiatives

Chart CC - Communities are Offering Specific Incentives for "Green" Initiatives (27 of 31)

Nearly half of the consultants responding to our 9th Annual Consultants Survey also have found communities offering incentives for "green initiatives," although only 23 percent say their clients have encountered "green performance" requirements as a stipulation for receiving incentives.

Next: Chart DD - Impact of High Energy Costs on Clients' Facility Plans

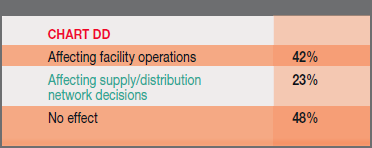

Chart DD - Impact of High Energy Costs on Clients' Facility Plans (28 of 31)

Energy availability and costs is considered "very important" or "important" by 89.3 percent of the responding consultants, placing this factor in ninth position. In fact, more than 40 percent of the consultants say high energy costs are affecting their clients' facility operations

Next: Chart EE - Sustainable Development Is More Important to Clients Now than in the Past

Chart EE - Sustainable Development Is More Important to Clients Now than in the Past (29 of 31)

Two thirds also say sustainable development is more important to their clients now than in the past.

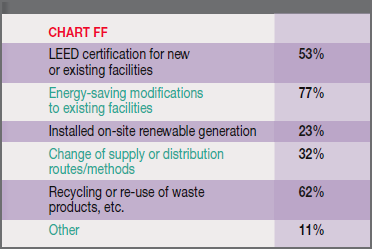

Next: Chart FF - Measures Being Undertaken by Clients to Reduce Company's "Carbon Footprint"

Chart FF - Measures Being Undertaken by Clients to Reduce Company's "Carbon Footprint" (30 of 31)

In response to this, three quarters of the consultants say their clients are making energy-saving modifications to their facilities; about two thirds say their clients are also recycling or re-using waste products; and more than half claim clients are seeking LEED certification for new or existing facilities.

Next: Chart GG - Existence of Businesses Performing Similar Activities in the Area of Search is Taken into Consideration by Clients

Chart GG - Existence of Businesses Performing Similar Activities in the Area of Search is Taken into Consideration by Clients (31 of 31)

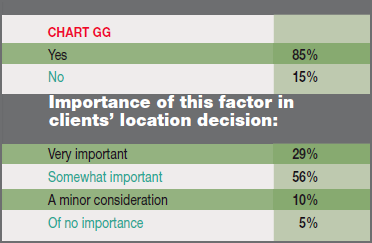

Eighty five percent of the responding consultants say their clients consider the existence of businesses in the area of search performing similar activities to theirs, with the same percentage considering this factor as very or somewhat important.

Survey Results Point to a "Positive Hold"

Survey Results Point to a "Positive Hold"Brett Hunsaker, executive vice president and regional managing director at Newmark Grubb Knight Frank

Emergence of Big Data Affects Corporate Survey Respondents' Priorities

Emergence of Big Data Affects Corporate Survey Respondents' PrioritiesBill Luttrell, senior locations strategist at Werner Enterprises

Corporate Survey Results Mirror General Market Trends

Corporate Survey Results Mirror General Market TrendsChristopher B. Schastok, vice president at Jones Lang LaSalleg

Corporate Survey Reflects the New Economic Normal

Corporate Survey Reflects the New Economic NormalThomas Stringer, Business Advisory Services, Ryan & Company

More than 50 percent of the responding consultants say they have worked on projects for durable good manufacturers as well as for distribution/logistics firms. About a third have also worked with non-durable goods and other manufacturers, as well as with those in the healthcare/life sciences industries and those who provide data- and computer-related services (Chart A).

More than 70 percent of the respondents to our Consultants Survey say they are providing location studies/comparative analyses to their clients; two thirds are negotiating and managing incentives on their clients’ behalf; and 40 percent handle their clients’ real estate transactions (Chart B).

About half of the respondents say they work primarily with mid-size firms in terms of their employment numbers (100-499), while more than a third also work with companies employing 500 or more people (Chart C).

Needless to say, nearly 90 percent of the responding consultants say executive management at their client firms is involved in the site selection process. The respondents to our 9th Annual Consultants Survey also say they work with their clients’ real estate (63 percent), tax and finance (54 percent), and other business unit management (55 percent) (Chart D). In fact, more than 60 percent of the responding consultants say their clients have gathered preliminary data prior to engaging their services. About half also say their client firms have narrowed down the geographic area in which they wish to locate, and a fifth actually claim their clients defer to them on the final location decision (Chart E).

Interestingly, the consultants who responded to our survey are slightly more optimistic about the state of the economy than the respondents to our 27th Annual Corporate Survey: 33 percent of the consultants expect the economy to improve by the end of this year (Chart F), whereas only 21 percent of the corporate respondents expect it to do so. In fact, more than 40 percent of the responding consultants say their clients still plan to open new facilities or expand despite the sluggish U.S. economic recovery (less than a quarter of the Corporate Survey respondents made that claim). Yet, a third of the responding consultants also acknowledge that some clients are putting facility plans on hold and deferring capital spending as a result of anemic economic growth (Chart G).

Clients’ New Facilities & Relocation Plans

A quarter of the respondents to our 9th Annual Consultants Survey say most of their clients who expect to open new facilities plan to do so within one year; more than half say their clients will open new facilities within two years (Chart H). Two thirds of the responding consultants also say their clients will open just one new facility (Chart I) — fewer new facilities than our Corporate Survey respondents say they are planning, but perhaps this is because the responding consultants are only engaged by their clients on one project at a time. The respondents to our Consultants Survey are primarily working on domestic projects slated for the South Atlantic — North Carolina, South Carolina, Virginia, West Virginia (16 percent of the projects); the South — Alabama, Florida, Georgia, Louisiana, Mississippi (15 percent); and the Southwest (Arizona, New Mexico, Oklahoma, Texas (13 percent) (Chart J), regions that are also heavily favored by our Corporate Survey respondents. When considering all of the new domestic facilities projects the responding consultants are working on, about 30 percent will be manufacturing plants and a quarter will house warehouse/distribution operations (Chart K).

As for expected new foreign facilities, the respondents to our Consultants Survey say many of the ones they are working on will be in Canada (17 percent) as well as Mexico (16 percent); 15 percent in Asia; and more than 10 percent in Western Europe as well as South America (Chart L). Interestingly, the respondents to our 27th Annual Corporate Survey also slated more than 10 percent of their foreign projects for each of these latter two regions, but far fewer for our neighbors to the north and south. Of those clients’ projects slated for Asia, China will garner the largest share — 29 percent (Chart M).

More than a third of the responding consultants’ clients’ new foreign facilities will be manufacturing operations, with 17 percent expected to house warehouse/distribution centers (Chart N). Additionally, 28 percent of the consultants say they have seen an increase in the number of companies establishing foreign facilities as opposed to domestic ones (Chart O). Nonetheless, two thirds say their clients are not expecting to locate a foreign operation/facility back to the United States. Of the third of the consultants who say their clients will re-shore, more than half explain that this is because their clients are having product quality issues at their foreign facilities and are also concerned about the cost of transporting supplies/products from overseas. More than a third cite rising foreign labor costs, and nearly 30 percent say their clients are encountering rising energy costs as well as having problems finding qualified and/or English-speaking labor (Chart P).

We also asked the Consultants Survey-takers about their clients’ domestic relocation plans. More than 80 percent say that their clients who expect to relocate a domestic facility will do so within one or two years. Of their clients planning relocations, proximity to suppliers/markets served as well as the need to lower labor costs, seems to be driving the decision (Chart Q).

When asked why their clients are not spending more of their money on investment in U.S. facilities, about half of the responding consultants blamed high taxes and excessive government regulations, as well as uncertainty about taxes and regulations for 2013 and beyond (Chart R). The respondents to our 27th Annual Corporate Survey had similar concerns.

Clients’ Site Selection Priorities

We also asked our Consultants Survey-takers to rate the site selection and quality-of-life factors as “very important,” “important,” “minor consideration,” or “of no importance” in their clients’ location decisions. The importance ratings and corresponding rankings, along with last year’s consultants’ ratings and rankings of the factors, are shown in Chart S and Chart T.

Before examining the specific factors, it should be noted that eight of the top-10 factors are rated “very important” or “important” by at least 90 percent of the responding consultants. However, only two factors (labor costs and highway accessibility) received importance ratings of more than 90 percent by the respondents to the 27th Annual Corporate Survey. Nevertheless, the respondents to our Consultants Survey consider the same three site selection factors as top priorities as do the respondents to our Corporate Survey — in slightly different order.

The responding consultants rank highway accessibility as the number-one factor, with a 98.3 percent combined “very important” or “important” rating, exactly the same as the prior year’s Consultants Survey’s respondents. Availability of skilled labor is ranked second with a 96.5 percent importance rating, and labor costs is ranked third with a 93 percent combined importance rating.

In keeping with the importance of labor costs, the consultant’s tenth-ranked factor is low union profile, with an 89.2 percent combined rating, representing a seven percentage point year-over-year increase — the third-largest jump in importance among the site selection factors in the Consultants Survey. Nonunion labor is traditionally lower-cost than organized labor with its concomitant benefits. The responding consultants agree with the Corporate Survey respondents in that 61 percent say unemployment rates are not making it easier for their clients to find the labor they need (Chart U). More than 80 percent of the consultants also say the unemployed are lacking the advanced skills their client companies require (Chart V). This may be why only 49 percent of the respondents to our Consultants Survey rate availability of unskilled labor as “very important” or “important,” similar to our corporate respondents, and placing this factor 24th in priority. Nevertheless, fully two thirds of the responding consultants believe that their clients are less than 25 percent dependent on contract or contingent labor (Chart W).

This lack of skilled labor has resulted in huge increases in the importance of proximity to technical college/training as well as training programs in general. These two factors show the greatest increases among site selection factors in their importance ratings by the consultants — jumping 19.4 and 13.2 percentage points, respectively, and now considered “very important” or “important” by more than three quarters of the responding consultants. Proximity to technical college/training also showed the largest percentage increase in importance in the Corporate Survey.

The factor showing the biggest jump in the consultants’ rankings is expedited or fast-track permitting — up five spots from 10th place in the prior year’s Consultants Survey to fifth position this year. Consultants know the importance of speed to market and getting a client’s project up and running quickly. Consequently, in a related question, more than 80 percent claim the existence of an available building is very or somewhat important in their clients’ site searches (Chart X), and more than three quarters affirm the importance of a shovel-ready or pre-certified site (Chart Y).

Proximity to major markets is ranked fourth by the consultants, with a combined “very important” or “important” rating of 92.9 percent. Two other market-access factors — railroad service and waterway or ocean port accessibility — also show increases in their importance ratings, although the consultants still rank them at the bottom of the list of site selection factors considered by their clients in the location search.

State and local incentives is ranked sixth among the site selection factors, and tax exemptions and corporate tax rate are tied for seventh position; all three of these factors are considered “very important” or “important” by more than 90 percent of the responding consultants. This is not surprising considering 61 percent of the consultants say incentives have always been of great importance to their clients (Chart Z). Remember, 70 percent of the Corporate Survey respondents say incentives are very or somewhat important to moving a project forward in a particular location.

Three quarters of the responding consultants say tax credits, exemptions, and the like are most important to their clients, and more than half say worker training incentives are equally important (Chart AA). Unfortunately, almost 30 percent of the consultants claim that their clients have had to repay incentives monies because job creation or investment obligations were not met (Chart BB).

Nearly half of the consultants responding to our 9th Annual Consultants Survey also have found communities offering incentives for “green initiatives,” although only 23 percent say their clients have encountered “green performance” requirements as a stipulation for receiving incentives (Chart CC).

This is important since energy availability and costs is considered “very important” or “important” by 89.3 percent of the responding consultants, placing this factor in ninth position. In fact, more than 40 percent of the consultants say high energy costs are affecting their clients’ facility operations (Chart DD). Two thirds also say sustainable development is more important to their clients now than in the past (Chart EE). In response to this, three quarters of the consultants say their clients are making energy-saving modifications to their facilities; about two thirds say their clients are also recycling or re-using waste products; and more than half claim clients are seeking LEED certification for new or existing facilities (Chart FF).

Finally, in a response similar to that given by the Corporate Survey respondents, 85 percent of the responding consultants say their clients consider the existence of businesses in the area of search performing similar activities to theirs, with the same percentage considering this factor as very or somewhat important (Chart GG).

In the separate ranking of quality-of-life factors, the respondents to our 9th Annual Consultants Survey consider colleges and universities in area the number-one factor, with nearly 80 percent rating it as “very important” or “important” — a 10.2 percentage point increase over this factor’s ranking in the year-prior survey.

The responding consultants consider low crime rate nearly as important, ranking it second, followed by educational and housing factors. With housing costs having dropped dramatically over the last few years in many parts of the country, this factor showed the largest decrease in its combined importance rating among all factors considered by the consultants — site selection and quality-of-life (-19.4 percentage points). And the cultural opportunities factor showed a 14.8 percent decrease in importance, achieving only a 43.8 percent combined importance rating and ranking last among quality-of-life factors on the consultants’ list.

Consultants’ Sources

of Information Similar to the Corporate Survey respondents, nearly three quarters of the responding consultants have used magazines like Area Development as a source of information when site selecting for their clients over the past two years. A similar percentage has used economic data aggregators. Needless to say, personal visits to areas of interest remain the top source of information as claimed by 84 percent of the consultants.

More than half of the consultants who took our survey maintain their own site selection database; yet nearly all (90 percent) also search the Internet for site and facility planning information. They are primarily looking for data on specific locations and contact information for economic development agencies (87 percent). Two thirds are seeking listings of available sites and buildings, e.g., utilizing FastFacility. More than 80 percent say between one and five locations make their clients’ “short list,” and nearly 60 percent say they and their clients generally visit up to five locations before making a final site selection decision. And, 88 percent of the respondents claim their clients usually reach a site decision within one year of engaging their services.