Without Utilities, It Could Have Been Worse

After an unusually mild December, the weather was more typical in January helping to support a 3.5 percent jump in utilities output. It was the largest monthly gain in eight months. Utilities comprises just under 10 percent of overall output, but the gain in this small component helped offset declines in other categories and soften the headline decline in today’s otherwise weak report.

Generally a Weak Report

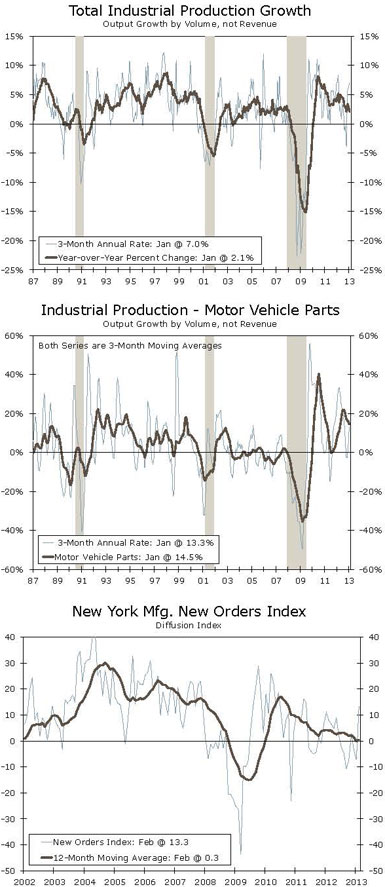

Manufacturing production fell 0.4 percent in January. December’s initially reported gain of 0.8 percent was revised higher to a 1.1 percent gain, so on an absolute level basis, factory output is actually little changed from what the Federal Reserve had first reported in December. What bears noting here is the directional change for a number of key components.

Motor vehicle and parts production, for example, was off 3.2 percent on the month. That was enough to swamp the 2.9 percent gain in this component in the prior month. Computer and electronics production fell 0.5 percent in January as well. Consumer products production, which makes up 27.3 percent of all output, fell 0.2 percent.

One month does not make a trend, but it seems as though the manufacturers of consumer products and automobiles dialed back production in anticipation of weaker demand. Consumers are adjusting to smaller after-tax income in the wake of income tax increases and the end of the payroll tax holiday which both went into effect in January.

That said, the weakness was not isolated to consumer-related parts of the economy. Information processing equipment for businesses fell 0.3 percent on the month and materials output fell 0.2 percent. Output at U.S. mines, which comprises about 15 percent of total industrial production, fell 1.0 percent in January as well. Capacity utilization fell to 79.1 percent from an upwardly revised 79.3 percent in December.

What Does This Mean For the Outlook?

Our Industrial Production & Business Spending Outlook published in December laid out our base case scenario which is essentially a very weak start to 2013 as businesses and consumers come to grips with tax increases and spending cuts before orders and production pick up speed as the year goes on. Today’s report is right in line with that thinking. A separate report, released this morning from the New York Federal Reserve, offers a silver lining. The Empire Manufacturing Index jumped to 10.04, the highest reading since May 2012. Among the positives in that report was a jump in the new orders component to its highest level in more than a year. While these regional PMIs can be volatile, the ISM index has cautiously moved to expansion territory as well.