Technology Will Help to Smooth Auto Industry's Rough Road

Despite the fact that the auto industry has fallen on hard times, development of innovative technologies holds promise for renewed growth in this sector.

Feb/Mar 10

Suppliers Cautiously Optimistic

Delphi ended four years of bankruptcy in October of 2009, emerging as a private company. Along that arduous path, this major auto parts manufacturer (a former unit of General Motors) cut thousands of workers, divested several businesses, and agreed to sell its steering systems operations and four plants back to GM. Today, Delphi is a much leaner more focused company whose core business will be electronic and safety components; power train, thermal, electrical, and electronic systems; and replacement parts.

Smaller tier-two suppliers, unable to sustain their business as their tier-one customers fell onto hard times, also went out of business. This reduced supply chain has the OEMs worried as they struggle with how to prop up badly needed suppliers with a much reduced vehicle inventory. According to industry experts, the "suppliers that survive will be those with varied customers around the world, contracts to build parts on different types of vehicles, and the best technology."

Craig Fitzgerald, a partner with Plante & Moran LLC for the automotive industry segment, estimates that "in three to five years the average [automotive] supplier will see profits, before interest and taxes, climb to 7-9 percent of their sales. That compares with the 3-5 percent suppliers have averaged in the last five years. It will take until about the first quarter of 2012 to reach auto production in North America of 12.6 million vehicles."

In their November 2009 Automotive Suppliers Sentiment survey, the Original Equipment Suppliers Association (OESA) noted that this index had slipped to 68.5 from September's 70.8, as the number of respondents who are "significantly more optimistic" fell and the number of "unchanged" expectations increased. While Q1 2010 vehicle sales and production is uncertain, suppliers appear to be stabilizing and recovering. However, the majority of suppliers responding to the survey forecast their 12-month revenue and operating profits would decrease by more than 20 percent on a year-over-year basis. Going forward, noted the report, year-over-year and month-over-month comparables will begin to improve.

Maurice Sessel, vice president of product engineering for International Automotive Components (IAC), a global conglomerate of manufacturing companies that produce a range of components and assemblies for the automotive industry, gave the keynote address at the Society of Plastics Engineers Automotive TPO (thermoplastic olefins) Conference in Detroit in October. His presentation, "The Interior Challenge," was optimistic as he shared real-world examples of how IAC has turned many of the challenges of 2009 into business opportunities. "At IAC, we've used these variables [mounting industry, regulatory, and economic challenges] into outlets of opportunity, rather than recoiling from them," said Sessel.

Sessel addressed three key demands that will impact the future of the automotive industry: (1) the unprecedented economic and industry times that include the lowest production volume in decades, reduced cash flow, and increased prices; (2) demand in consumer trends for sustainable and natural materials and transition to smaller, more fuel-efficient vehicles; and (3) the tough government mandates for increased fuel efficiency and increased safety that continue to put automakers and their suppliers under tremendous pressure to find ways to reduce vehicle mass, while improving crash performance.

Future Looking Brighter for the OEMs

Yet, despite all the negative news of plant closures and unemployed auto workers, the automotive industry, including parts manufacturing, continues to be one of the largest employers in the United States. According to the Federal Reserve, over eight million motor vehicles were assembled in the United States in 2008. Building and assembling the thousands of components of these vehicles requires a huge supply chain and a complex design, manufacturing, and assembly process, said a report from the U.S. Bureau of Labor Statistics (BLS) for Motor Vehicle and Parts Manufacturing.

In 2008, the latest year for which full-year data are available, about 9,100 establishments manufactured motor vehicles and parts, said the U.S. BLS. These ranged from small parts plants with only a few workers to huge assembly plants that employ thousands. Approximately seven out of 10 establishments in the industry manufactured motor vehicle parts - including electrical and electronic equipment; engines and transmissions; brake systems; seating and interior trim; steering and suspension components; air-conditioners; and motor vehicle stampings, such as fenders, tops, body parts, trim, and molding.

In 2008, 22 percent of all workers in the overall vehicle manufacturing industry were engaged in vehicle assembly, with a large number of these assembly plants owned by foreign automakers known as the "foreign domestics." That same year - of the 877,000 jobs lost - 62 percent were in the firms that manufacture vehicle parts.

According to the latest report from PricewaterhouseCoopers (PwC), the game has changed for this industry. "The aftereffects of the worldwide economic and financial downturn have altered the business landscape and have challenged longstanding assumptions about successful operating structures," said a PwC press release. "During the last decade, the underlying competitive landscape has changed dramatically because of the emergence of new markets and new industry players, as well as fundamental changes in the economic environments of the mature markets," said Richard Hanna, global auto leader, PwC. "The global recession has challenged the core operating models responsible for delivering the business strategy of many companies."

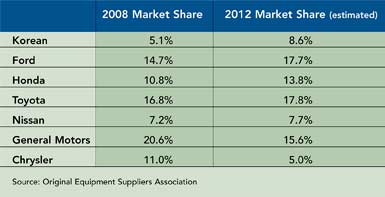

In a 2007 report, Honda projected that between 2008 and 2011, it would introduce 120 new or redesigned models. The new "foreign domestics" nearly doubled their market share from 1997 to 2007, going from 28.9 percent to 50.2 percent. Meanwhile, the Detroit Big 3 (General Motors, Ford, and Chrysler) lost market share during that same10-year period, decreasing from 71.1 percent to 48.8 percent.

What's on the Horizon?

While the future of the automotive industry is uncertain, a November 2009 presentation by John Murphy, senior director of Bank of America Merrill Lynch, for the Original Equipment Suppliers Association Conference, was quite optimistic. According to Murphy, "The recovery is just beginning to recover," with the upside to auto demand and supply greater than most expect. The leaders, he noted, are Hyundai, Ford, and Honda, which will be the ones to follow.

As to the supplier landscape, "It should get better from here," he noted, but consolidation will continue to accelerate. "Success hinges on proprietary technology, diversification, and a strong balance sheet," Murphy pointed out. "Restructuring, recapitalization, and reorganization of the value chain have made significant progress with more to come. We are not `cautiously optimistic'; we are flat out bullish."

There are several examples of positive news, including some developments coming out of Canada. For instance, Magna International -in conjunction with the National Research Council Canada - is setting up an R&D facility to develop lightweight, strong composite parts for the next-generation vehicles. Called the Magna-NRC Composite Center of Excellence, it will be located at Magna's Exteriors & Interiors facility in Concord, Ontario. The Center is expected to be operational by summer of this year.

And, in the United States, there's also light at the end of the tunnel for ailing GM. At the recent Detroit Auto Show, GM's President Mark Reuss said that plants that build the Cadillac SRX, Chevrolet Equinox, and Buick LaCrosse are at full capacity and can't meet demand. To help that situation, GM is considering reopening some closed facilities. The company, said Reuss, has placed its Janesville, Wis., and Spring Hill, Tenn., plants on standby in the event it needs more capacity when the U.S. auto industry begins to improve. The Spring Hill plant was recently upgraded, at the cost of millions of dollars, to build the Chevrolet Traverse. The facility is flexible and can build other models as well.

Automakers are holding out hope for alternative-fuel and "green" vehicles. Delphi announced plans in December to implement an $89.3 million award from the U.S. Department of Energy (DOE) to support expansion of engineering capabilities in the manufacture of advanced "green" technologies. A vacant manufacturing site in Kokomo, Ind., has been selected for production of power electronics components for global customers, with initial products to be built for Allison Transmission in partnership with two Indiana technology leaders. Delphi will match the award for a total of $178.6 million to advance the development of low-cost manufacturing of electric-drive vehicles (EDV) in the United States.

"Electric-drive vehicles hold the promise of meeting two critical government and industry goals - reducing dependence on petroleum and reducing greenhouse gas emissions," said Delphi Electronics & Safety President Jeff Owens. "Delphi has a long history of successfully developing and commercializing automotive electronics. With this DOE partnership, we will apply our proven expertise to develop technologies and processes that will help lower the cost of electric-drive vehicles and make them more attractive to a broad range of consumers."

Additionally, General Motors has high hopes for hydrogen vehicles. Daniel O'Connell, director of fuel cell commercialization for GM, is working to make hydrogen vehicles a reality. "We currently have 100 hydrogen fuel cell Equinox cars on the road that to date have accumulated 1.2 million miles in customers' hands," he said in a recent interview.

The company has 30 of these hydrogen vehicles in New York State. The big challenge, noted O'Connell, is putting in the filling stations. Currently, there are five hydrogen filling stations in New York City and three in Rochester. "We're exploring ways we can put enough stations from Buffalo to Long Island, a route that will be called the NYSERDA Hydrogen Highway," he explained. Since the cars only have a 200-mile limit, customers testing the cars are constrained to driving within a 100-mile radius of a filling station. Other challenges, said O'Connell, include getting the cost of the vehicles down to make them affordable for large numbers of consumers and increasing the durability of the vehicles.

GM's hydrogen R&D facility is located in Honeoye Falls, N.Y., where the company employs 400 people. Currently, said O'Connell, there are nearly 1,000 people working on the hydrogen technology in various areas. "These are the kind of jobs you want - high-skilled, high-tech jobs," stated O'Connell. "We have a world-class employee base worldwide that we've brought to the New York area to work on this technology for GM. We also have close relationships with all the colleges in the area. Rochester offers a unique opportunity thanks to companies like Kodak and Xerox; there's a lot of talent in this area. And there's also a lot of hydrogen in New York State. This technology - wells to wheels - will result in an 85 percent reduction in CO2 from a renewable source - Niagara Falls."

It is hoped more positive automotive news is on the horizon for 2010.

Recent Project Announcements

Clarios Expands St. Joseph, Missouri, Operations

05/09/2026

LEV Manufacturing Plans Putnam County, Tennessee, Assembly-Logistics Operations

05/05/2026

GMB USA Plans Opelika, Alabama, Production Operations

04/20/2026

Dakota Bodies Expands Liberty, Missouri, Operations

04/17/2026

Mercedes-Benz Expands Tuscaloosa County, Alabama, Production Operations

04/14/2026

AXN Automotive Systems Relocates-Expands Louisville, Kentucky, Operations

04/10/2026

South Korea-Based Hyundai Translead Plans Will County, Illinois, Manufacturing Operations

04/07/2026

France-Based Valeo Plans McAllen, Texas, Manufacturing Operations

04/03/2026

Toyota Motor Manufacturing Kentucky Expands Georgetown, Kentucky, EV Vehicle Production Operations

03/31/2026

Autokiniton Expands Bellevue, Ohio, Manufacturing Operations

03/24/2026

BorgWarner Plans Hendersonville, North Carolina, Manufacturing Operations

03/23/2026

Japan-Based Newman Technology Expands Mansfield, Ohio, Operations

03/22/2026

Minth Group Limited Plans Gadsden, Alabama, Manufacturing Operations

03/19/2026

Fukoku Korea Plans Henry County, Virginia, Manufacturing Operations

03/13/2026

Most Read

-

Top States for Doing Business in 2024: A Continued Legacy of Excellence

Q3 2024

-

Where Workforce Capacity Is Being Built — and Where It’s Being Deployed

Q1 2026

-

40th Annual Corporate and 22nd Annual Consultant Site Selection Survey Results

Q1 2026

-

Economic Developer Role Shifting from Deal-Making to Systems Stewardship

Q1 2026

-

2025’s Top States for Business: How the Winners Are Outpacing the Rest

Q3 2025

-

The Workforce Bottleneck in America’s Manufacturing Revival

Q4 2025

-

Advanced Manufacturing Isn’t a Buzzword—It’s a Different Location Strategy

Q1 2026