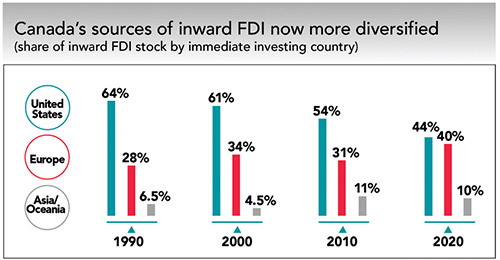

Canada’s foreign direct investment (FDI) performance remains strong by global standards. According to the latest data from Statistics Canada, the stock of FDI rose by $77.8 billion in 2024, reaching a record $1.5 trillion.

Investment was particularly robust in manufacturing and natural resources, reflecting sustained international interest in these sectors. Notably, Canada now holds the second-highest FDI-to-GDP ratio among G20 nations, a testament to its strong economic fundamentals, open markets, and reputation for political and regulatory stability.

As geopolitical tensions rise and global industrial policy shifts, Canada’s supply chain reorganization in 2025 is becoming more than a response — it is a strategic pivot to enhance domestic resilience and position Canada as a more attractive destination for FDI.

The Canadian Manufacturers & Exporters (CME) has emphasized the urgent need to redesign supply chains for resilience, not just efficiency. Global disruptions, escalating protectionism such as U.S. tariffs, and raw material volatility have exposed critical vulnerabilities in Canada's manufacturing base.

In its Spring 2025 Manufacturing Outlook Report, CME highlighted that 68 percent of Canadian manufacturers experienced supply chain disruptions in the past year. Only 20 percent reported full visibility into their Tier 2 and Tier 3 suppliers. Seventy-two percent support government incentives to near-shore or re-shore supply chains.

Federal and Provincial Action Is Underway

Although calls continue for a formal Supply Chain Resilience Office and a National Industrial Supply Chain Strategy similar to the U.S. Office of Supply Chain Preparedness, governments at both levels are already responding.

68%

The National Trade Corridors Fund (NTCF) is investing in infrastructure and digital tools to enhance logistical efficiency and reduce bottlenecks. The Strategic Innovation Fund is targeting domestic manufacturing, including Canada’s steel sector, to pivot into new, resilient product lines. The Critical Minerals Strategy supports domestic extraction, processing, and circular supply chains for rare earths and battery materials.

From North American to “Dual-Market” Supply Chains

Until now, Canada often functioned as a North American gateway, especially for automotive, agri-food, and advanced manufacturing. But tariff risks are shifting this model. Canadian firms are now redesigning supply chains into two distinct streams: Canada-focused chains, aimed at domestic use and diversified export markets; and U.S.-focused chains, with some production moved or co-located in the U.S. to maintain tariff-free access and qualify for Buy American procurement.

Vertical Integration and Domestic Rebuilding

The reorganization is spurring renewed interest in vertical integration and domestic sourcing. We’re seeing early moves to localize critical inputs in sectors like auto and aerospace parts, clean tech and battery components, agri-food processing, and rare earths and mining services.

Firms are reshoring previously offshored processes and forming new partnerships with Canadian suppliers to blunt tariff exposure and ensure security of supply.

Investor confidence is no longer a given, it must be earned, project by project. Canada’s reboot is not just defensive — it’s a long-term play for industrial resilience.

Infrastructure and Regional Pressure Points

As firms reconfigure operations, demand is rising for industrial land and logistics hubs outside traditional export corridors; cold storage, clean energy capacity, and rail interconnectivity for domestic distribution; and interprovincial trade infrastructure to support diversified market access.

To support this shift, provincial governments are accelerating permitting processes, including in British Columbia, Ontario, Saskatchewan, and Alberta.

Strategic Co-Manufacturing With U.S. Partners

Another adaptation underway is cross-border co-manufacturing. Canadian firms may increase joint ventures or assembly-sharing agreements with U.S. partners where components are built in Canada and final assembly, or compliance happens under U.S. jurisdiction. This strategy preserves U.S. market access and eligibility for government procurement programs.

FDI in Flux but Opportunity Ahead

As Canadian site selectors working closely with international investors, we see both the drivers of interest in Canada and the reasons for hesitation. On the surface, Canada continues to check the right boxes: a highly skilled workforce, a diverse industrial base, world-class infrastructure, and preferential access to more than 50 countries through free trade agreements. These strengths still resonate with corporate decision-makers.

The question has shifted from “Is Canada a good place to do business?” to “Can Canada stay competitive?”

Yet beneath this positive outlook, caution is growing. In recent months, global investors have become more reluctant to commit to large-scale projects in Canada, largely due to escalating trade frictions, particularly the latest wave of U.S. tariffs and the uncertainty of what may follow.

While these trends point to long-term strength, some FDI has paused in the short term. International investors are watching tariff developments closely, hedging decisions between Canadian expansion and U.S. onshoring.

From an investor’s perspective, Canada is no longer evaluated in isolation. Increasingly, companies compare its value proposition not only to the United States, but also to emerging alternatives in Europe and Asia.

Canada continues to offer a compelling mix of talent, incentives, and market access. However, the growing influence of U.S. protectionism casts a long shadow over investment decisions. This uncertainty affects everything from capital budgeting to site selection for North American manufacturing.

72%

For many investors, the question has shifted from “Is Canada a good place to do business?” to “Can Canada remain competitive if trade friction becomes the new normal?”

Conclusion: Resilience Now, Advantage Later

Canada’s 2025 supply chain reorganization is more than defensive — it’s laying the foundation for a next-generation industrial strategy. While short-term uncertainty may temper FDI inflows, the long game is clear: a more resilient, vertically integrated, digitally mature manufacturing ecosystem with reduced overdependence on U.S. trade flows.

If executed well, this transition could make Canada a global benchmark for industrial security and sustainability and an even more attractive place to build the supply chains of the future.

Global investors are paying close attention. While Canada is still viewed as a stable and reliable jurisdiction, it now faces growing external pressures. Investor confidence is no longer a given — it must be earned, project by project.

As site selectors helping companies evaluate locations and deploy capital, we believe Canada has the tools to remain competitive. But doing so will require a proactive, strategic, and realistic approach to the evolving global trade landscape.