The Boston Consulting Group’s latest research confirms manufacturing executives’ confidence in the U.S. economy. Some 16 percent of the 252 decision-makers at companies with sales of billion or more who were surveyed by BCG said they are already bringing production back from China to the U.S. — up from 13 percent the previous year. In fact, respondents to BCG’s survey said that the U.S. would account for an average of 47 percent of their total production within five years.

How do the aforementioned findings stack up against the plans of those corporate executives who utilize Area Development for their site and new facility planning and informational needs? In order to find out, we surveyed them in late fall 2014. Their responses are illustrated in the accompanying charts.

Some143 executives responded to our 29th Annual Corporate Survey. Of those, 35 percent are with manufacturing firms; 13 percent are in the financial services/insurance/real estate sector; and just 8 percent are with distribution/logistics providers (figure 1). More than two fifths (42 percent) are the chief executives or owners of their companies (figure 2), and more than 50 percent of the Corporate Survey respondents are responsible for their firms’ final location decision, with another 37 percent making preliminary recommendations (figure 3). In addition to executive management (85 percent), other departments involved in the location decision include operations management (61 percent), real estate (35 percent), and tax and finance (32 percent), among others (figure 4).

Nearly two thirds of our Corporate Survey respondents say their firms operate three or more domestic facilities, and half operate five or more foreign facilities (figure 5). More than 30 percent of the respondents also say their firms employ 100–499 people, while another 30 percent claim to employ 1,000 or more individuals (figure 6).

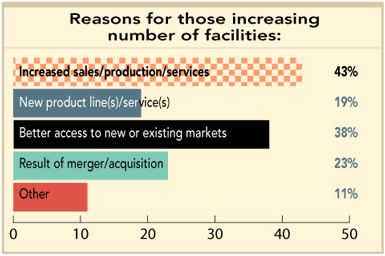

The number of their facilities has not changed over the last year for two thirds of the Corporate Survey respondents. Interestingly, though, 28 percent say they did increase their number of facilities (figure 7) for reasons ranging from increased sales/production (43 percent) to better access to new or existing markets (38 percent) (figure 8).

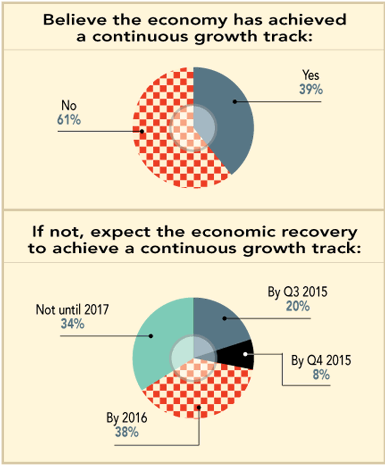

More than a third of the respondents to our 29th Annual Corporate Survey say the economic recovery has had a positive effect on their operations; i.e., they plan to open facilities, increase hiring, and/or increase capital spending. Another 35 percent, on the other hand, say they have no new facility plans resulting from the economic recovery (figure 10). In fact, 61 percent of the respondents believe the economy has not yet achieved a continuous growth track, with more than 70 percent saying it won’t do so until 2016 or 2017 (figure 11) — up from 59 percent of the prior year’s Corporate Survey respondents who expected continuous economic growth two years out.

When asked about their plans for new facilities, only 36 percent of this year’s Corporate Survey respondents say they will open new facilities within the next two years (figure 12). This is down from 45 percent who said they had such expectations at the end of 2013. This is not surprising considering the fact that only 28 percent tell us they expect the economic recovery to achieve a continuous growth track by the end of this year.

Of those survey respondents with plans for new facilities, 39 percent expect to open just one domestic facility, and another 30 percent expect to open two (figure 13). The Midwest (Illinois, Indiana, Michigan, Ohio, Wisconsin) will garner a fifth of all the planned domestic facilities — up from 14 percent reported by the prior year’s Corporate Survey respondents. There’s also increased interest in the Southwest (Arizona, New Mexico, Oklahoma, Texas) — up from 11 percent to 14 percent this year — and the Mid-South (Arkansas, Kentucky, Missouri, Tennessee) — up from 9 percent to 11 percent of the planned domestic projects. Meanwhile, the South (Alabama, Florida, Georgia, Louisiana, Mississippi) with 17 percent and the South Atlantic (North Carolina, South Carolina, Virginia, West Virginia) with 12 percent of the planned new domestic facilities are consistent picks. However, less activity is planned for New England (Connecticut, Massachusetts, Maine, New Hampshire, Rhode Island, Vermont) — down from 6 percent to 2 percent of the total — and the Middle Atlantic (Delaware, Maryland, New Jersey, New York, Pennsylvania) — down from 13 percent to 8 percent of the total (figure 14).

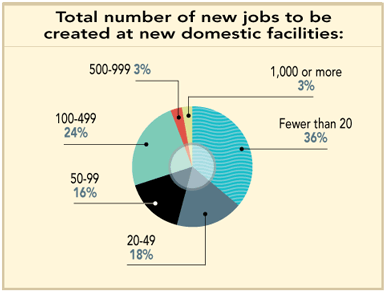

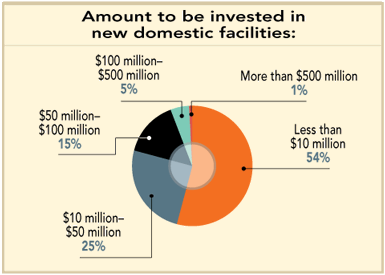

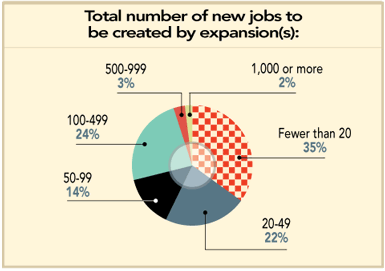

The majority of the new domestic facilities planned by the Corporate Survey respondents will be manufacturing operations (28 percent) and warehouse/distribution centers (23 percent) (figure 15). And only 30 percent of the respondents claim their new domestic facilities will create more than 100 jobs (figure 16). Investment figures are on the low end as well: more than half the respondents say less than $10 million will be invested in new domestic facilities (figure 17).

When it comes to Asia, China is a perennial favorite, accounting for 44 percent of the planned new Asian facilities. Interest in India has increased — up from 17 percent to 33 percent — as has interest in Malaysia, which jumped from 7 percent to 22 percent of the planned total new Asian facilities (figure 20).

A third of the new foreign facilities planned by the Corporate Survey respondents will house manufacturing operations, and 19 percent will be warehouse/distribution centers (figure 21). It also seems these respondents will create more jobs at foreign facilities than at domestic ones — 44 percent say their new foreign facilities will create more than 100 jobs (figure 22). Nevertheless, the total investment in new foreign facilities will be under $10 million for 42 percent of the respondents, with another 37 percent expecting that investment to be between $10 million and $50 million (figure 23).

Relocation plans are up slightly on a year-over-year basis. Thirty percent of the Corporate Survey respondents plan to relocate a domestic facility over the next three years (figure 26). Among the reasons cited for relocation are high taxes (44 percent) and excessive government regulations (29 percent), as well as labor availability (26 percent) and labor costs (24 percent) (figure 27).

Nevertheless, only 2 percent of the respondents expect to relocate a domestic facility to offshore (down from 7 percent claiming they would make such a move in the prior year’s survey). And, as for reshoring a facility back to the U.S., only 4 percent claim they would being making that move (figure 28) — consistent with the prior year’s results and despite all the media reports of a surge in the reshoring movement. Of those few who claim they will reshore, two thirds cite rising foreign labor costs as the impetus for doing so, and half say product quality issues and the costs of transporting supplies/products are to blame (figure 29). On the flip side, among the issues preventing our Corporate Survey respondents from spending more of their earnings on investment in U.S. facilities are, as in years past, excessive government regulation (56 percent), high corporate taxes/tax uncertainty (47 percent), economic instability (46 percent), and healthcare costs under the Affordable Care Act (37 percent) (figure 30).

Next: Corporate Respondents’ Location Priorities