In the wake of shifting tariff policies, softening electric vehicle mandates, and reductions in EV tax credits, automotive OEMs and parts suppliers are rethinking risk strategies and identifying new opportunities for growth. These macroeconomic and policy changes are forcing leadership teams to recalibrate where and how they invest in production capacity.

Vehicle development timelines are long — often five years or more — but the current pace of political and regulatory change makes long-term planning a moving target. As of mid-July 2025, manufacturers face multiple layers of tariffs, including a 10 percent baseline reciprocal tariff on imports unless country-specific exemptions apply. Vehicles and parts imported from Canada and Mexico that comply with USMCA face tariffs of 25 percent on their non-U.S. content, with a potential increase to 30 percent on Mexican content pending in August, according to the “Trump 2.0 Tariff Tracker” published by Reed Smith.

These changes are already hitting certain vehicle segments and brands. European premium automakers, for instance, have seen weighted tariff rates rise sharply — from 1.7 percent in May 2024 to 18.2 percent in May 2025. Volkswagen, which imports about 43 percent of its U.S. sales, is particularly exposed, according to S&P Global Mobility.

Meanwhile, EV demand is tapering. A suite of early 2025 executive orders eliminated federal EV mandates and rescinded California’s longstanding emissions waiver and zero-emission vehicle roadmap. Congress subsequently reversed several EPA waiver approvals under the Congressional Review Act. BEV adoption is now expected to drop from 61 percent to 30 percent by 2035, according to Roland Berger.

At the same time, a new interest deduction for automotive loans could stimulate renewed interest in internal combustion engine (ICE) vehicles — especially those assembled in the U.S.

Across the board, OEMs are adjusting strategies to navigate the volatility.

Supply chains are being restructured. Automakers are tightening inventory management and seeking ways to limit working capital exposure to tariffs. Some are exploring nearshoring in Mexico to produce USMCA-compliant components that can enter the U.S. duty-free, according to a Q2 2025 article in Area Development by Alexandra Segers and Michael Johnson.

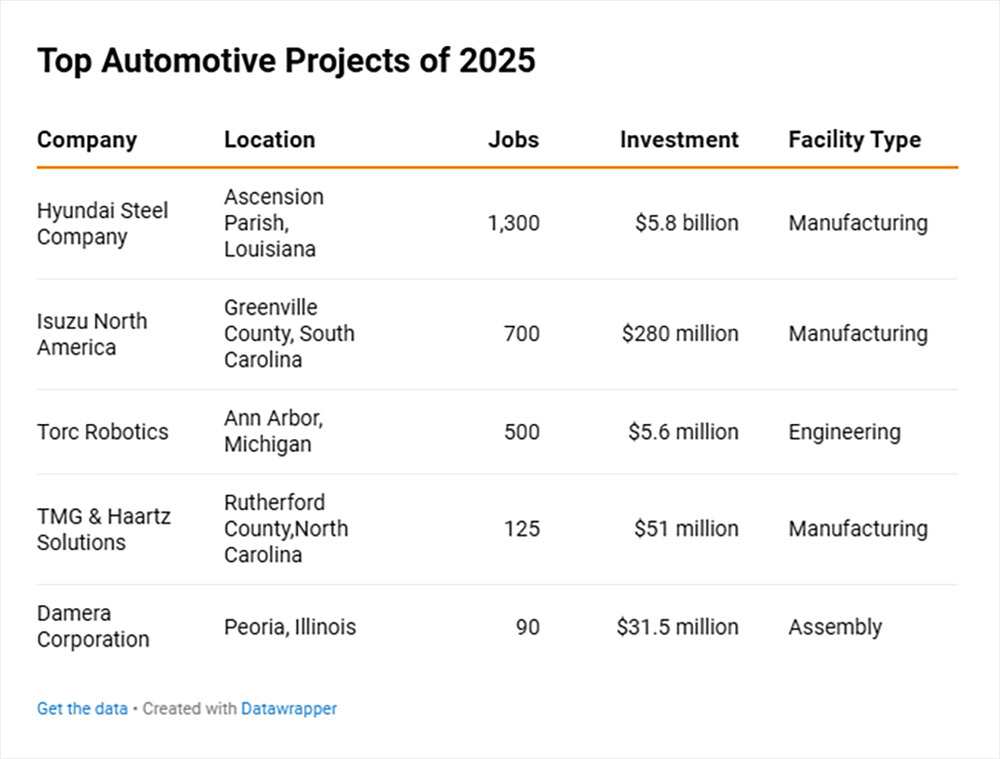

Production plans are shifting. As automakers face new cost pressures and demand signals, they are reassessing what to build, where, and when. General Motors recently announced $4 billion in domestic investment to expand its ICE and EV output. Nissan has paused QX50/55 production in Mexico and is exploring U.S. production for Infiniti, according to Automotive News and industry sources.

Powertrain flexibility is gaining traction. With federal tax credits for BEVs off the table and mandates rolled back, the rate of EV adoption is slowing. Many OEMs are expanding their lineup to include ICE, hybrids, plug-in hybrids (PHEVs), and extended-range EVs (EREVs). Hybrids and EREVs are expected to grow significantly due to reduced charging anxiety, improved range, and smaller battery packs, according to S&P Global Mobility.

New manufacturing technologies are reducing risk. To enable greater production flexibility and reduce complexity, manufacturers are embracing innovations that support multiple powertrains on a single line. One example is Toyota’s “K-Flex” system, deployed at its Georgetown, Kentucky, plant, which can assemble Camry and RAV4 models with ICE, hybrid, or PHEV powertrains, according to Automotive News.

For companies in this shifting environment, the real estate and site strategy implications are far-reaching.

Emerging supply chains are creating new siting targets. Electric motor technologies, especially rare-earth-free variants, are reshaping the supplier ecosystem. While China holds about 45 percent of global market share, new suppliers — particularly in Europe and North America — are rapidly gaining ground. Europe is projected to produce 17 percent of rare-earth-free motors by 2030, with 16 new market entrants expected over the same period, according to S&P Global Mobility.

Companies that stay agile and align their site strategies with emerging risks and opportunities will be best positioned to lead.

Historical site assumptions deserve a fresh look. In 2012, Boston Consulting Group predicted that rising costs in China would spur a “tipping point” for U.S. reshoring in transportation goods. At that time, the sector’s import value stood at $6 billion. By 2024, imports had ballooned to $44 billion. While that initial prediction didn’t fully materialize, the combined effects of rising labor costs, logistics pressures, and tariffs may now accelerate a shift back to U.S. manufacturing. BCG noted that the U.S. would attract reshored production due to its skilled labor force, R&D ecosystem, customer proximity, and more secure operating environment.

Clustering around existing plants is accelerating. With logistics costs rising and just-in-time inventory systems under pressure, OEMs are increasingly drawing suppliers closer to major production hubs. More Tier 1, Tier 2, and Tier 3 vendors are locating near assembly plants to enhance supply chain resilience and reduce transit costs.

Workforce development is becoming a critical success factor. As new technologies are adopted and lines retooled, incumbent worker retraining is essential. Toyota’s Production to Skills (P2S) program in Mississippi, launched in partnership with a local community college, is a strong example of aligning workforce development with new manufacturing demands, according to the National Institute of Standards and Technology.

Incentives that mitigate uncertainty are regaining relevance. Foreign Trade Zones (FTZs), bonded warehouses, and special economic zones can help offset tariff impacts by offering tax deferrals and duty exemptions. These tools are particularly useful in high-risk trade environments, according to previous reporting in Area Development.

With the automotive sector representing more than $1 trillion in U.S. GDP, companies that stay agile and align their site strategies with emerging risks and opportunities will be best positioned to lead. For real estate and operations executives, this is a moment to proactively review assumptions, challenge legacy models, and leverage every tool — policy, workforce, and technology — to navigate an evolving global landscape.