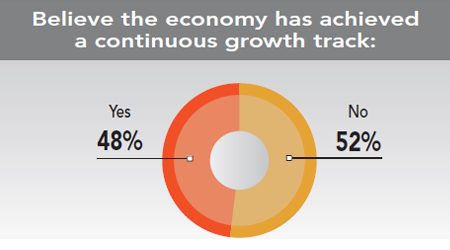

Mark Zandi, chief economist at Moody’s Analytics, commented on the remarkable consistency of employment growth over the last several years. And optimism about employment actually led the Federal Reserve to raise interest rates for the first time since 2008. However, Carl Tannenbaum, chief economist at Northern Trust, told The New York Times (1/8/16), “We certainly see the impact of global conditions in the manufacturing sector, where the strong dollar and weak commodities prices have diminished momentum substantially [although] the service side of the American economy is progressing unabated.”

PwC’s Q4 2015 Manufacturing Barometer indicates U.S. manufacturers are being cautious in their hiring and capital spending plans because of the uncertain global economic outlook. They still anticipate revenue growth, but at a more modest pace. Do our corporate executive readers’ plans reflect this tempered optimism?

30th Annual Corporate Survey Results

-

Figure 1

-

Figure 2

-

Figure 3

-

Figure 4

-

Figure 5

-

Figure 6

-

Figure 7

-

Figure 8

-

Figure 9

-

Figure 10

-

Figure 11

-

Figure 12

-

Figure 13

-

Figure 14

-

Figure 15

-

Figure 16

-

Figure 17

-

Figure 18

-

Figure 19

-

Figure 20

-

Figure 21

-

Figure 22

-

Figure 23

-

Figure 24

-

Figure 25

-

Figure 26

-

Figure 27

-

Figure 28

-

Figure 29

-

Figure 30

-

Figure 31

-

Figure 32

-

Figure 33

-

Figure 34

-

Figure 35

-

Figure 36

-

Figure 36a

-

Figure 37

-

Figure 38

-

Figure 39

-

Figure 40

-

Figure 41

-

Figure 42

-

Figure 43

-

Figure 44

-

Figure 45

-

Figure 46

-

Figure 47

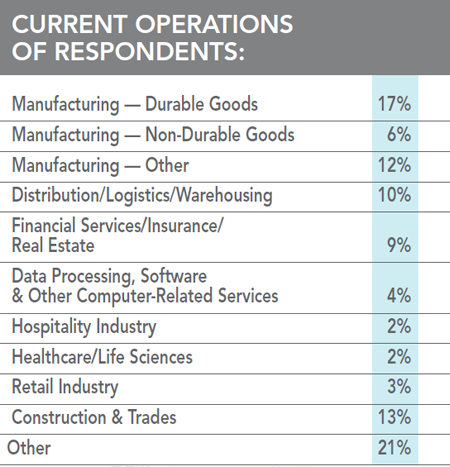

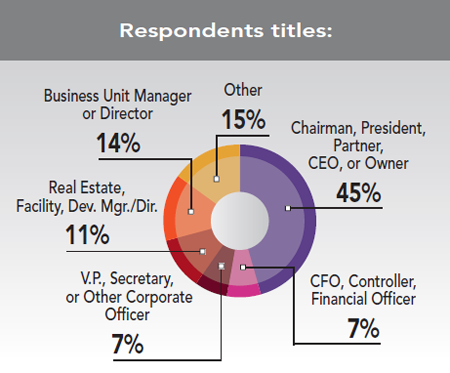

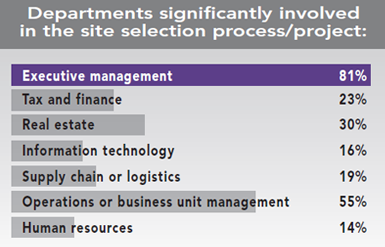

Of those responding to our 30th Annual Corporate Survey, just 35 percent are with manufacturing firms. Nearly 60 percent of these respondents represent the C-suite, i.e., they’re the owners or CEOs, CFOs, or other corporate officers.

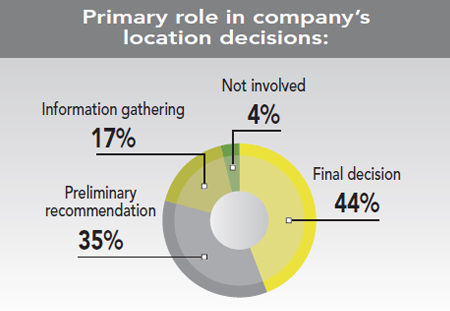

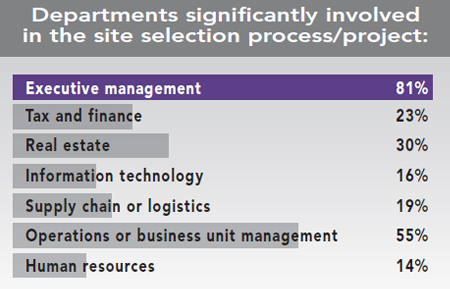

More than three quarters of these respondents make either the final location decision or the preliminary recommendation of where to locate or expand. It stands to reason, therefore, that 80 percent of the corporate respondents say executive management is significantly involved in the site selection process; and it’s no surprise that more than half say management of their operations or business units are also involved in this decision.

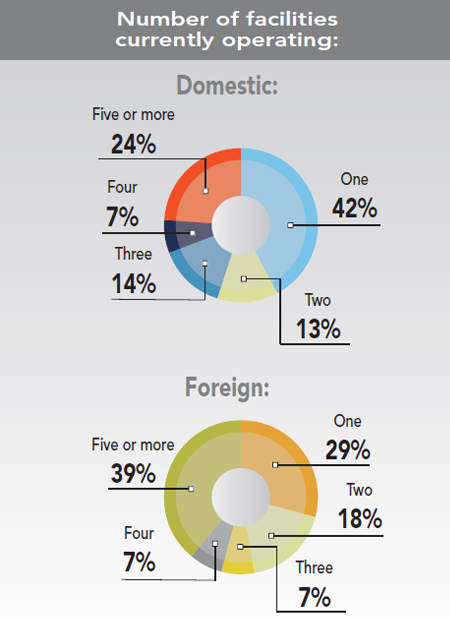

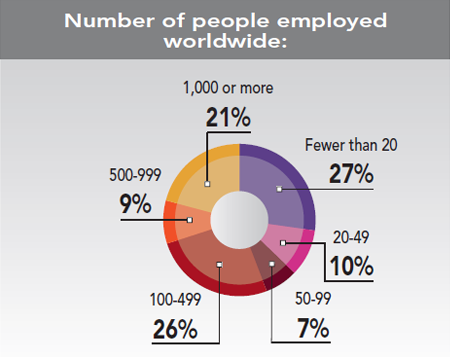

More than 40 percent of the Corporate Survey respondents operate just one domestic facility, with about a quarter operating five or more domestic facilities. The percentages are reversed when it comes to foreign facilities: just 29 percent of the respondents operate one foreign facility, while nearly 40 percent operate five or more. Thirty percent of the respondents employ 500 to 1,000+ people at their facilities worldwide, and 26 percent claim to be mid-sized in terms of employment (100-499 workers worldwide).

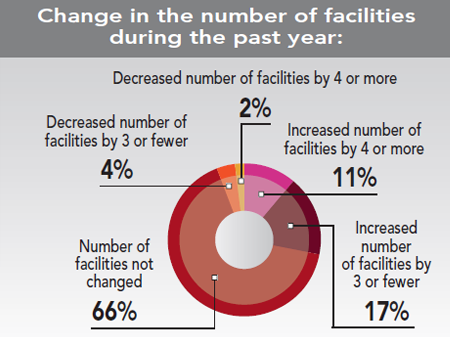

Fully two-thirds of this year’s Corporate Survey respondents say their number of facilities has not changed over the past year. However, 28 percent did increase their number of facilities, with only 6 percent claiming a decrease (these are the same percentages as reported in our prior year’s survey).

New Facilities Plans

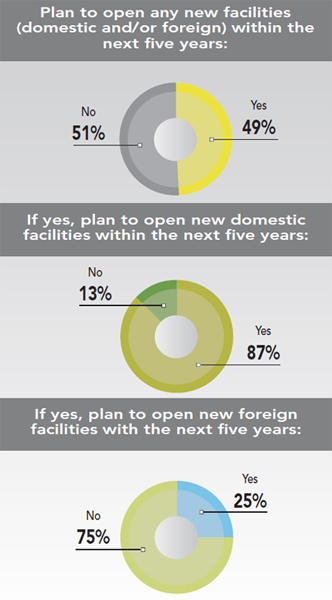

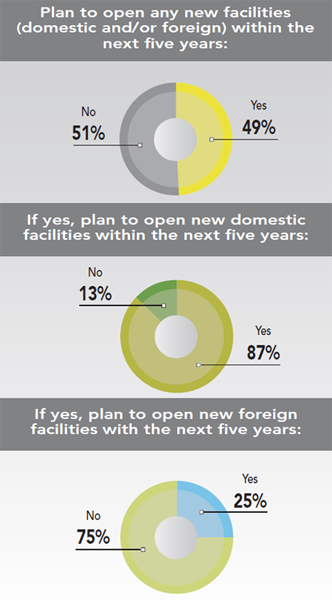

Some 49 percent of those responding to our Corporate Survey say they plan to open new facilities within the next five years (a 3 percent increase over the prior year’s survey). Of those, 87 percent say these facilities will be in the U.S., and just a quarter plan on locating these new facilities in a foreign location.

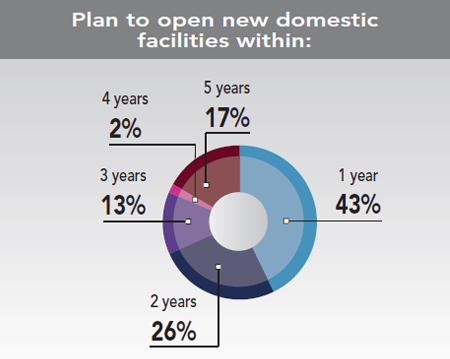

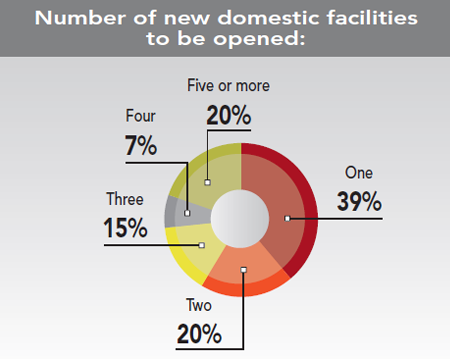

Nearly 70 percent of those with plans for new domestic facilities say they will open them within the next two years. Nearly 60 percent say they’ll open one or two domestic facilities, but a fifth say they’ll open five or more.

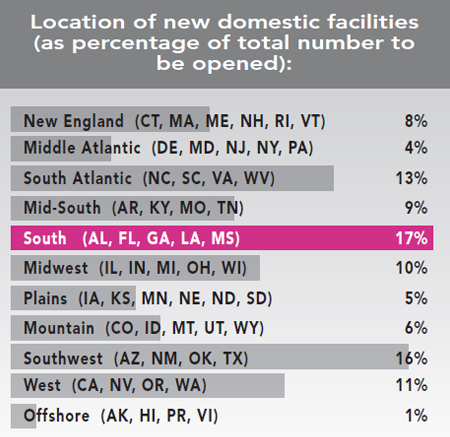

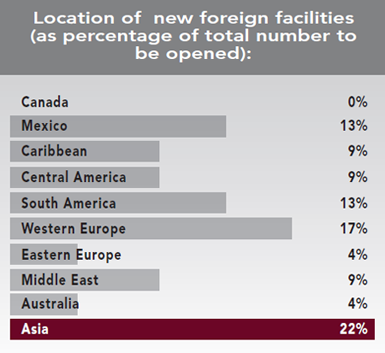

More than half of these new facilities will be in a southern region of the U.S. — 17 percent of the total planned projects are slated for the South; 16 percent for the Southwest; 13 percent for the South Atlantic; and 9 percent for the Mid-South. Whereas the prior year’s Corporate Survey respondents had planned 20 percent of their new facilities for the Midwest, the respondents to the 30th Annual Corporate Survey say only 10 percent of their new facilities are slated for that region of the U.S.

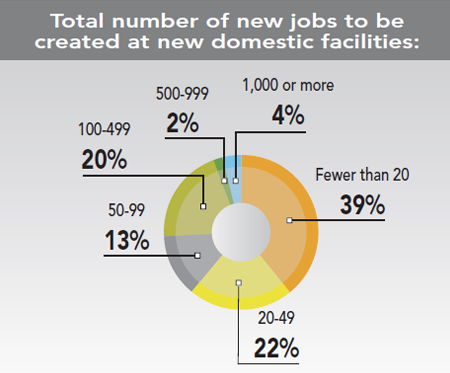

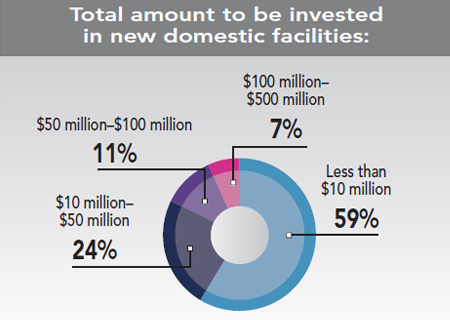

Most of these new domestic facilities will create fewer than 100 jobs, say three quarters of the Corporate Survey respondents. And the majority of the respondents (59 percent) also plan on spending less than $10 million to establish these facilities. Once again, these results are quite similar to those of our prior year’s Corporate Survey.

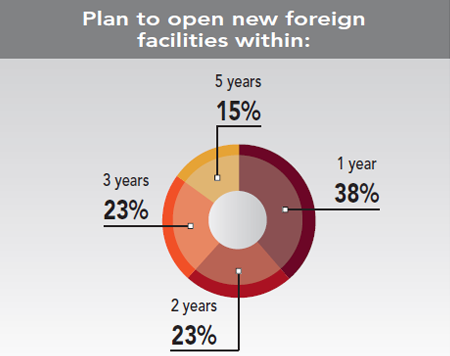

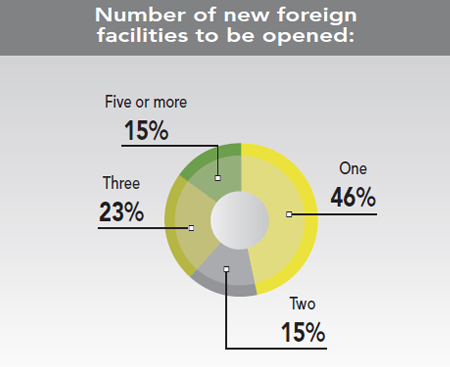

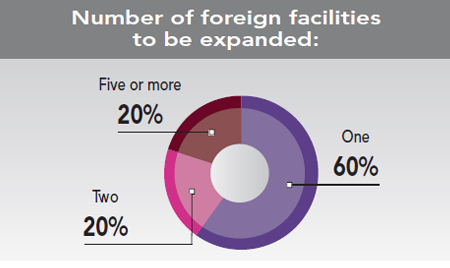

Although fewer of our respondents have plans for new foreign facilities, of those that do, about 60 percent plan to open them within two years, with 46 percent opening just one.

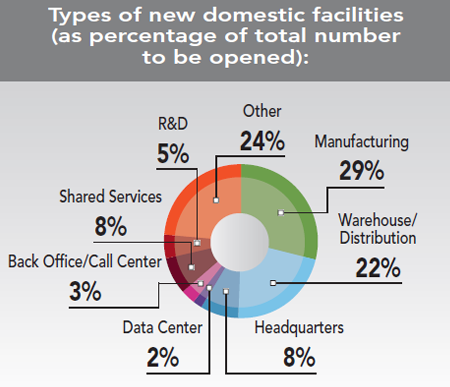

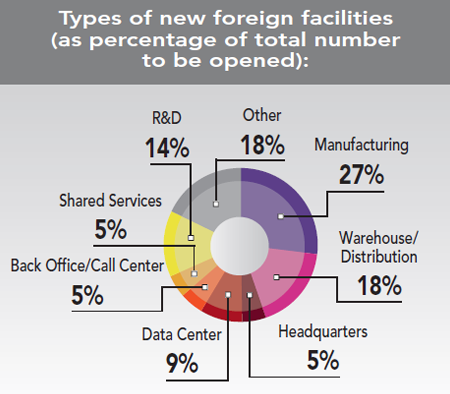

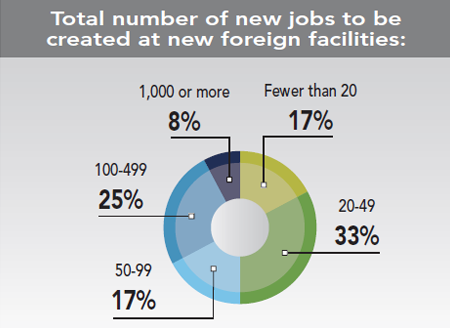

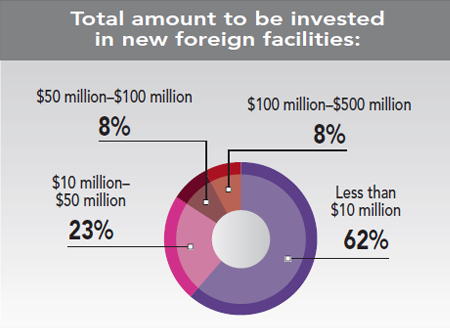

More than a quarter of the new foreign facilities planned by our Corporate Survey respondents will be manufacturing plants, and 18 percent will be warehouse/distribution facilities. The new foreign facilities will create only slightly more jobs than the domestic ones, with two-thirds of the respondents saying fewer than 100 jobs will be created at new foreign facilities. Once again, for the majority of the respondents (62 percent) these new facilities will represent an investment of less than $10 million.

Next: Corporate Respondents’ Expansion and Relocation Plans

Expansion and Relocation Plans

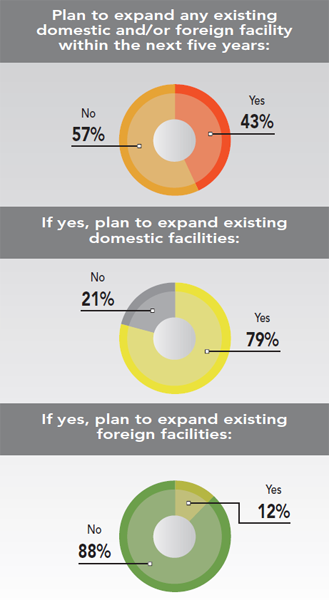

Although expansion plans as reported by corporate respondents have increased slightly on a year-over-year basis (39 percent to 43 percent of the respondents), fewer of the respondents to our 30th Annual Corporate Survey expect to expand an existing facility than open a new facility (49 percent). Of those with expansion plans, 79 percent plan to expand an existing domestic facility, with just 12 percent saying they plan to expand an existing foreign facility.

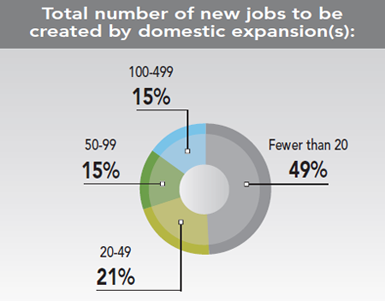

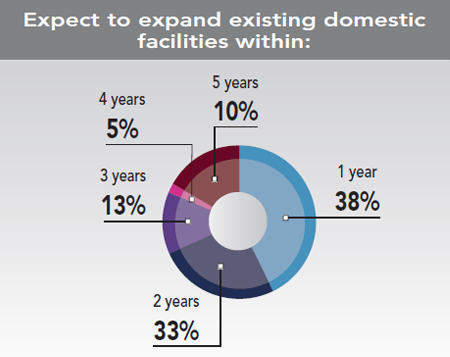

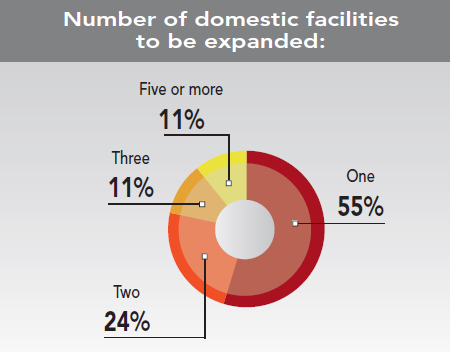

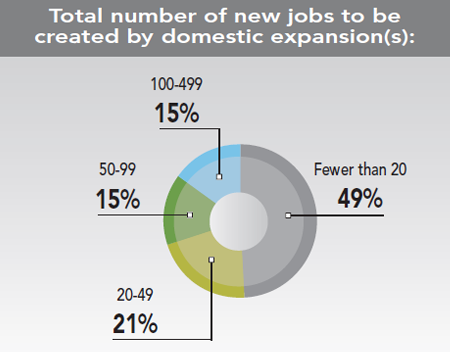

About 70 percent of those respondents who plan to expand an existing domestic facility will do so within the next two years, with nearly 80 percent expanding one or two domestic facilities, and 85 percent of the respondents claiming the domestic expansions will create fewer than 100 jobs.

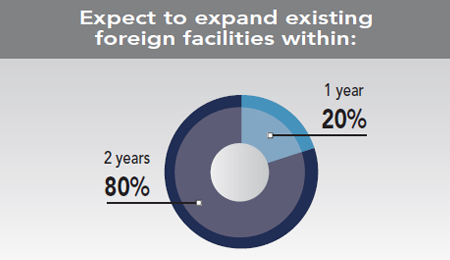

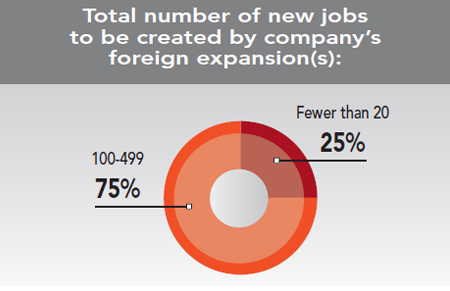

All of the respondents with plans for expanding foreign facilities will do so within one to two years, with 80 percent of these respondents saying they plan to expand just one or two foreign facilities. Interestingly, though, these expansions of foreign facilities will create between 100 and 499 jobs, according to three quarters of the respondents to this question.

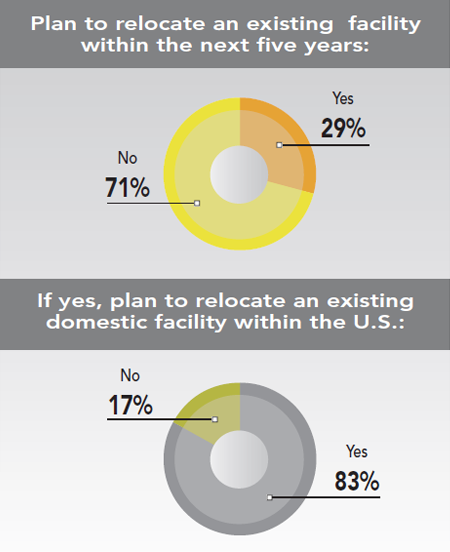

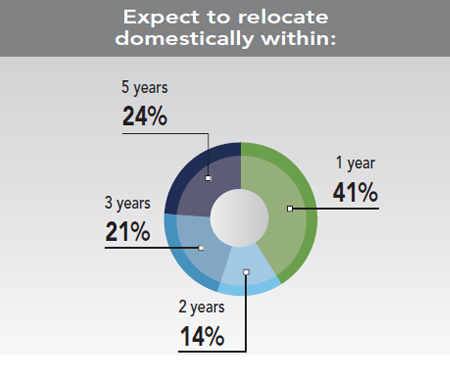

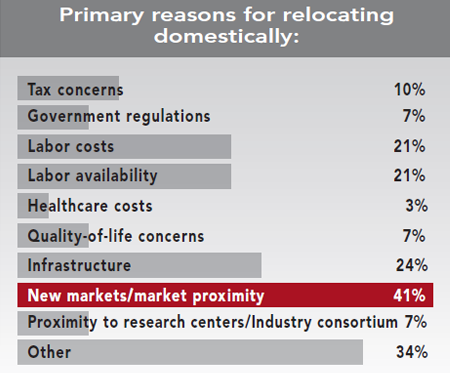

Overall relocation plans, on the other hand, are not as robust. Just 29 percent of the respondents to our 30th Annual Corporate Survey say they plan to relocate an existing facility within the next five years. Of those respondents with relocation plans, 83 percent say they plan to relocate an existing domestic facility within the U.S., with more than half having one- to two-year plans to do so. The primary reasons for relocating domestically are new markets/market proximity (cited by more than 40 percent of the respondents), and labor availability and labor costs (each cited by a fifth of the respondents).

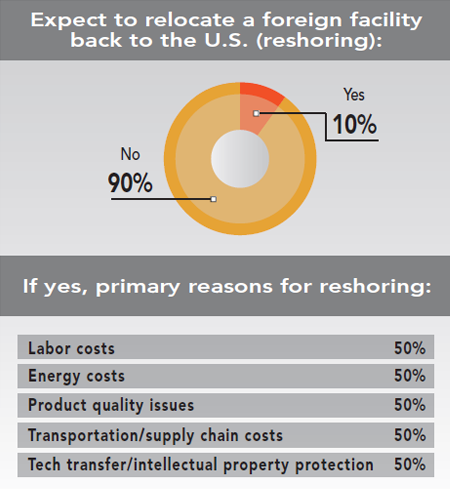

Nearly all (94 percent) of the Corporate Survey respondents have no plans to relocate a domestic facility to an offshore or near-shore location. The slight percentage who do plan to relocate offshore cite tax concerns as their incentive to move.

30th Annual Corporate Survey Results

-

Figure 1

-

Figure 2

-

Figure 3

-

Figure 4

-

Figure 5

-

Figure 6

-

Figure 7

-

Figure 8

-

Figure 9

-

Figure 10

-

Figure 11

-

Figure 12

-

Figure 13

-

Figure 14

-

Figure 15

-

Figure 16

-

Figure 17

-

Figure 18

-

Figure 19

-

Figure 20

-

Figure 21

-

Figure 22

-

Figure 23

-

Figure 24

-

Figure 25

-

Figure 26

-

Figure 27

-

Figure 28

-

Figure 29

-

Figure 30

-

Figure 32

-

Figure 33

-

Figure 34

-

Figure 35

-

Figure 36

-

Figure 37

-

Figure 38

-

Figure 39

-

Figure 40

-

Figure 41

-

Figure 42

-

Figure 43

-

Figure 44

-

Figure 45

-

Figure 46

-

Figure 47

Interestingly, the latest U.S. Reshoring Index for A.T. Kearney indicates that offshoring of U.S. manufacturing production continues to grow at a faster pace than reshoring of production to the United States (although some, including those with the Reshoring Initiative, take issue with A.T. Kearney’s finding of lackluster reshoring).

A.T. Kearney could only identify 60 factory operations returning from offshore to the U.S. in 2015, with many returning to an existing facility. According to A.T. Kearney Partner Patrick Van den Bossche, “The reshoring phenomenon, once viewed by many as the leading edge of a decisive shift in global manufacturing, may actually have been just a one-off aberration.” Contributing to this lack of reshoring, he adds, is a lack of skilled workers and “service provider ecosystems that had disappeared years ago.”

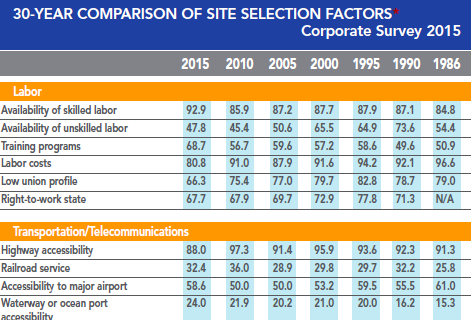

Site Selection Priorities

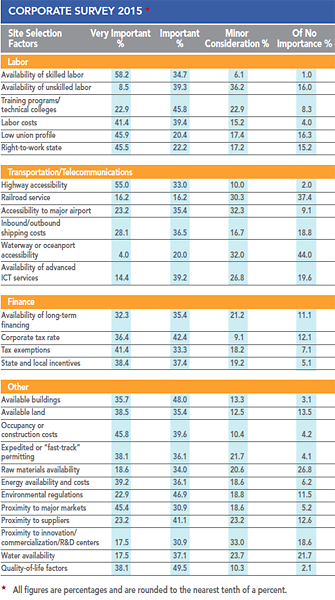

We asked those responding to our 30th Annual Corporate Survey to rate the factors they consider when making their new facility, expansion, and relocation plans as either “very important,” “important,” “minor consideration,” or “of no importance.” We then added the “very important” and “important” ratings in order to rank the factors in order of importance.

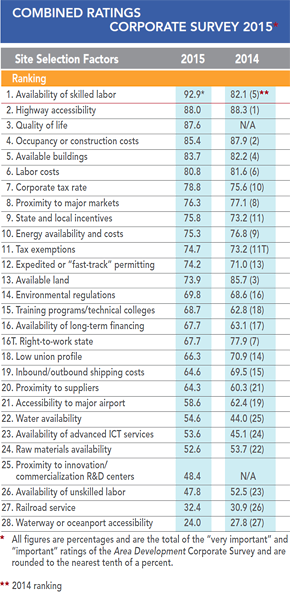

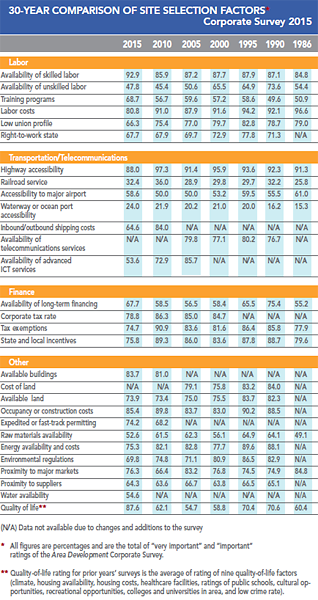

Our Corporate Survey respondents’ number-one concern is availability of skilled labor, considered “very important” or “important” by 92.9 of the respondents, up 10.8 percentage points (the greatest increase overall) from the prior year’s survey, in which this factor had ranked fifth — a ranking that we considered somewhat of an aberration. This factor also trumps labor costs, ranked sixth by our survey respondents with an 80.8 percent combined importance rating. With lower unemployment and a slowly growing economy, wages are starting to rise — but finding workers with the right combination of skills still takes precedence.

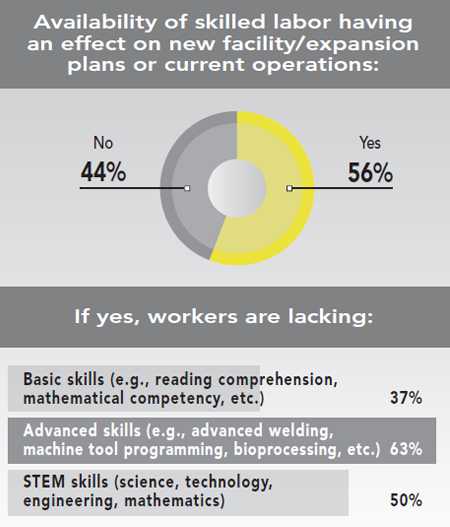

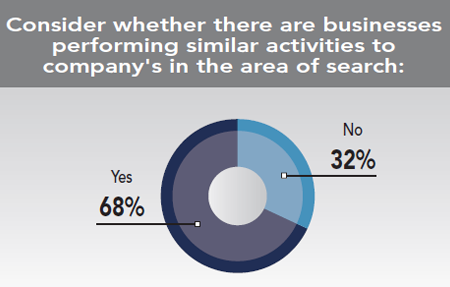

This explains why more than half (56 percent) of our Corporate Survey respondents say that availability of skilled labor is having an effect on their new facility and expansion plans. It’s also why 68 percent of the respondents say they consider whether there are businesses performing activities similar to those of their company in the area of search.

When it comes to labor skills, nearly two-thirds of our Corporate Survey respondents say workers are lacking advanced skills such as advanced welding or machine tool programming. Half the respondents also say workers are lacking the critical STEM skills.

The second-ranked factor in our 30th Annual Corporate Survey is highway accessibility, which has historically been ranked as a top factor (last year it was ranked first). Fully 88 percent of the survey respondents rated this factor as “very important” or “important.” Infrastructure factors “will continue to grow in importance as we become even more of an economy where just-in-time manufacturing and distribution of goods are more critical,” says Larry Gigerich, managing director of location consulting firm Ginovus.

Related to distribution is proximity to major markets, considered “very important” or “important” by more than three quarters of the survey respondents and ranking eighth among the factors. Remember, the main reason the survey respondents say they are relocating domestically is new markets/market proximity, cited by 41 percent of the respondents.

For our 30th Annual Corporate Survey we did not ask our survey-takers to separately rate the importance of quality-of-life factors including climate, housing availability and costs, healthcare facilities, ratings of public schools, cultural and recreational opportunities, colleges and universities in area, and crime rate. In the prior year’s survey none of these factors was considered “very important” or “important” by fewer than 60 percent of the respondents. Our current survey respondents give overall quality of life an 87.6 percent combined importance rating, placing in third among all the site selection factors! It seems the importance of quality of life has steadily been creeping up.

Although occupancy and construction costs vary among markets, these cost factors are always top of mind for companies building or expanding facilities. This factor received an 85.4 combined importance rating from our Corporate Survey takers and ranked fourth among the site selection factors.

With companies requiring quick turnaround times once the decision to open a new facility or expand is made, they often look for available buildings. This factor ranked fifth, considered “very important” or “important” by 83.7 percent of the respondents to our Annual Corporate Survey. If a company can find an existing facility that works for them, and they can upgrade and occupy it quickly, they will often choose the existing building instead of constructing a new one.

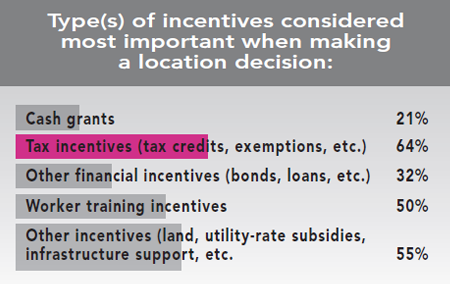

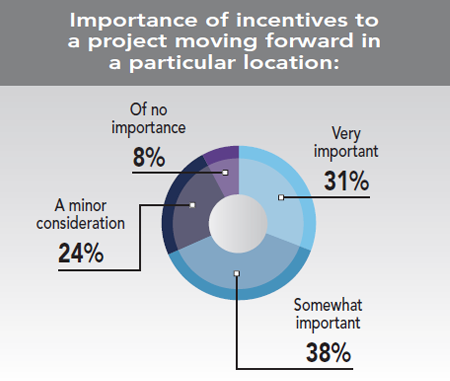

The “tax” factors also rank highly: Corporate tax rate is ranked seventh by the respondents, with a 78.8 percent combined importance rating; state and local incentives is ranked ninth, with a 75.8 percent combined rating; and tax exemptions is ranked 11th, with a 74. 7 percent combined rating. Nearly two thirds of the respondents say tax incentives are considered most important when making a location decision, with nearly 70 percent saying incentives are very or somewhat important to a project moving forward in a particular location.

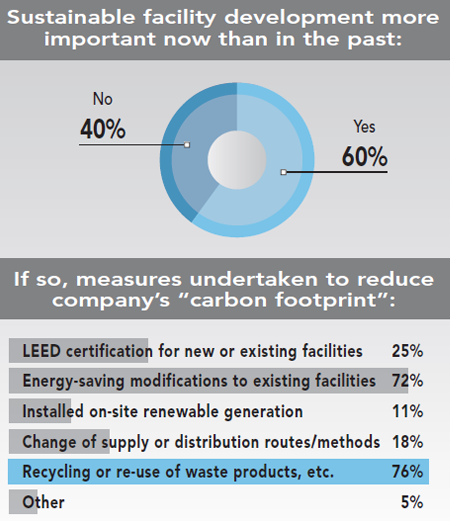

Rounding out the top-10 factors is energy availability and costs, with a 75.3 percent combined importance rating. In fact, more than 70 percent of the Corporate Survey respondents say they are making energy-saving modifications to their facilities to keep costs down.

Although only rated “very important” or “important” by slightly more than half of the respondents to our 30th Annual Corporate Survey, water availability shows the second-largest increase in combined importance, increasing 10.6 percentage points and now considered “very important” or “important” by 54.6 percent of the survey respondents. This factor keeps rising in importance as problems with water availability and quality — take for example the crisis now occurring in Flint, Michigan — keep drawing the attention of companies making location decisions.

A 2014 survey of major U.S. corporations by the Pacific Institute and VOX Global found that 60 percent of companies believe water challenges will negatively affect business growth and profitability within five years, as reported by the U.S. Chamber of Commerce Foundation. More than 80 percent said it would affect their location decisions. Five years prior, fewer than 20 percent responding to the organizations’ survey expressed concern about water risks.

The factor showing the largest decrease in importance rating (11.8 percentage points) and dropping from third in the rankings to 13th is available land, considered “very important” or “important” by 73.9 percent of the Corporate Survey respondents. Available land is much more important to a large manufacturing project going forward than to an office facility, for example, where an available building might be a better fit. Considering the fact that manufacturers represent just 35 percent of the survey respondents, the decrease in importance of this factor is more understandable than its high rating and ranking in the prior year’s survey.

The right-to-work state factor shows the second-largest drop in the ratings (decreasing 10.2 percentage points) and rankings (from seventh to 16th). Our Corporate Survey respondents give this factor a combined importance rating of 67.7 percent. Half the states now have right-to-work laws in place, and others — like Kentucky — have local right-to-work laws at the county level. Additionally, in many states that are not right-to-work, unionization rates are low, making this factor more of a non-issue.

Next: The Location Decision ProcessLocation Decision Process

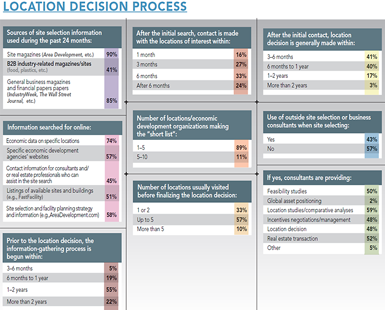

Ninety percent of our 30th Annual Corporate Survey respondents get their site selection information from magazines like Area Development. Nearly 60 percent also search online sources (e.g., AreaDevelopment.com) for this type of information, with about three quarters looking for economic data on specific locations, and half looking for listings of available sites and buildings.

More than half of these respondents begin the information-gathering process one to two years before making a location decision. Three quarters make contact with the locations of interest within one to six months of beginning their initial search.

About 90 percent say they put between one and five locations on their “short list.” A third only visit one or two of the location finalists, but more than half visit up to five locations before making their final decision. About 80 percent say the final site selection decision is made within three months to one year of initial contact.

Fewer than half (43 percent) use outside location or business consultants when site selecting. Of those that do, about half say they are providing feasibility studies, location/comparative analyses, incentives negotiations/management, and help with the real estate transaction, as well making the final location decision.

30th Annual Corporate Survey Results

-

Figure 1

-

Figure 2

-

Figure 3

-

Figure 4

-

Figure 5

-

Figure 6

-

Figure 7

-

Figure 8

-

Figure 9

-

Figure 10

-

Figure 11

-

Figure 12

-

Figure 13

-

Figure 14

-

Figure 15

-

Figure 16

-

Figure 17

-

Figure 18

-

Figure 19

-

Figure 20

-

Figure 21

-

Figure 22

-

Figure 23

-

Figure 24

-

Figure 25

-

Figure 26

-

Figure 27

-

Figure 28

-

Figure 29

-

Figure 30

-

Figure 32

-

Figure 33

-

Figure 34

-

Figure 35

-

Figure 36

-

Figure 37

-

Figure 38

-

Figure 39

-

Figure 40

-

Figure 41

-

Figure 42

-

Figure 43

-

Figure 44

-

Figure 45

-

Figure 46

-

Figure 47

The conclusion’s made in our prior year’s survey — i.e., that our 30th Annual Corporate Survey would reflect increased new facility and expansion activity — appear to hold true. Economists also are predicting U.S. GDP growth of 2.4 percent for 2016, according to The Conference Board, propelled by growth in employment and wages.

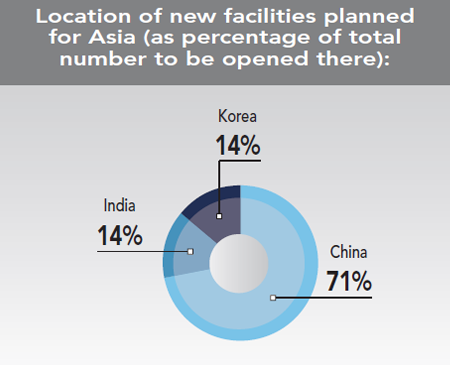

And according to Deloitte’s Q4/2015 CFO SignalsTM Report, there is considerable optimism in CFOs’ expectations and plans for 2016. Growing existing businesses and getting more efficient are the CFOs’ dominant focuses, but new markets are very significant for some industries, says the report. The CFOs say they will increase their investment in North American markets, with little additional focus on Europe or China.

Our next Corporate Survey will be conducted at year’s end, with a new president elected. The results will, no doubt, reflect our corporate executive readers’ confidence in the president-elect’s ability to help their businesses prosper and grow.