Life science real estate markets are at a reset that’s a historical norm for the sector. The pattern of expansion, overheated peak and uneven correction is familiar both in the Research Triangle and across North America. How do we assess where the market actually stands, the structural forces shaping demand, and what real estate and site selection decision-makers should consider in the near and longer term?

The Oversupply Overhang: What the Numbers Say

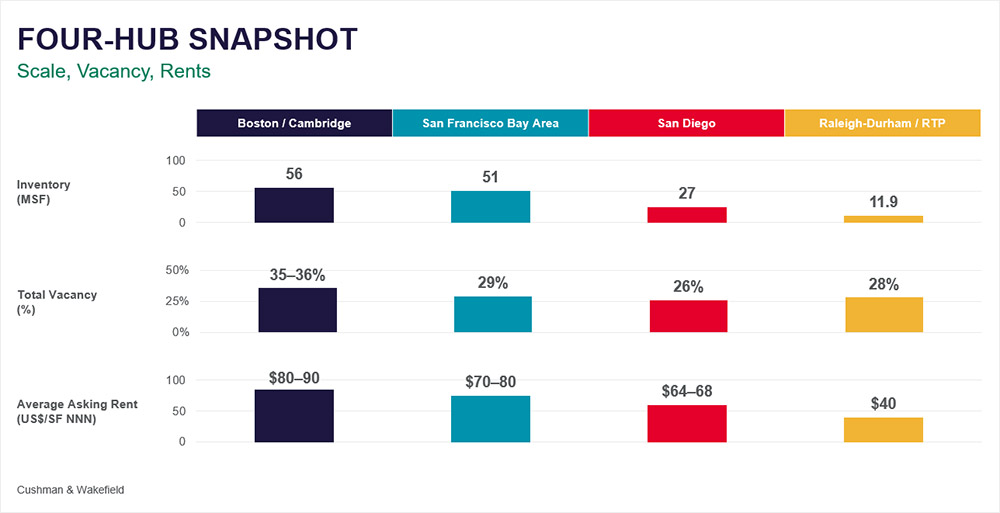

The headline figures remain sobering for anyone with exposure to the top-tier life science markets. Leasable life science inventory across the United States stands at roughly 200 million square feet, with national vacancy running at approximately 23.5 percent. But that aggregate number masks a more acute problem in the markets that matter most. Boston, the San Francisco Bay Area and San Diego collectively account for around 130 million square feet of that inventory — and vacancy in those three markets has climbed above 30 percent, a direct consequence of the speculative development boom that peaked around 2021–2022.

Boston, the global leader in life science venture fundraising — home to roughly 130,000 to 140,000 life science workers, with around 52,000 in pure R&D roles — is experiencing some of the most turbulent real estate conditions in the country. Average asking rents have fallen steadily since late 2023 and recently dropped below $80 per square foot for the first time since 2022. Still high in absolute terms, but the trajectory is unmistakable. There is also roughly 3.5 million square feet of new construction not yet reflected in vacancy counts, plus a significant volume of shadow sublease space expected to come to market over the next two years. When developers and leasing brokers in Boston describe current conditions, the language is grim. The absorption challenge is going to take time to resolve.

The convergence between life science and technology is real — and it is reshaping what demand looks like.

The San Francisco Bay Area presents a similar story, though its geographic spread across multiple submarkets — and the crossover with Silicon Valley’s technology sector — adds complexity (on the bright side, the AI boom has revived San Francisco Bay Area office leasing). San Diego, the third major hub, operates as a two-speed market: a core that has maintained sub-10 percent vacancy alongside an outer ring where rates have spiked sharply.

The silver lining for portfolio managers with assets in secondary and tertiary markets is interesting. Markets that did not attract the same wave of speculative capital find themselves in comparatively healthy supply-demand balance. In Raleigh-Durham, construction halted just as overbuilding took hold — partly by design, partly by virtue of being a smaller-scale market. Since that freeze, significant amounts of that spec-built space have been absorbed. (This accounts for the vacancy difference between 30 percent and low 23.5 percent when you include markets beyond Boston, the San Francisco Bay Area and San Diego.) A range of regional clusters find themselves with less egregious vacancy levels, precisely because they were not the Goliath-sized stars of the speculative boom.

That said, there is a real tension worth flagging for smaller markets. Available product is essential to generating the initial prospect look. Even when a company ultimately moves forward with a ground-up development, they typically need to tour a handful of existing spaces first — it helps crystallize their program and builds familiarity with the region. If ready-to-go inventory gets absorbed and nothing new is built, a market risks becoming less visible at that critical early stage of site selection. It is never a perfect balance. The trick is knowing which imbalance you have and planning accordingly.

The Selective Recovery: Where Capital Is Actually Going

Precision matters when describing what “recovery” actually means right now, because it is not a broad-based rebound. In 2025, approximately eight percent of funding rounds were mega-rounds exceeding $100 million — yet those rounds represented roughly 50 percent of all venture dollars deployed. About 60 percent of U.S. biotech venture capital is flowing into two geographies: Greater Boston and the San Francisco Bay Area. Overall deal volume has retreated to levels last seen around 2015, a full decade before the bubble.

23.5%

The companies most likely to require significant real estate — new laboratory buildouts, manufacturing facilities, regional R&D campuses — are, for the most part, already well-funded, established organizations. Smaller emerging companies are either operating lean or struggling to access capital. Investors who absorbed losses in the 2020–2022 cycle, and who are still contending with meaningfully higher interest rates than the pre-2022 era, have become what might be called asset-centric: gravitating toward single-focus companies with clean, comprehensible pipelines, smaller teams and clearer M&A optionality.

A single-asset company is simpler to fund, faster to evaluate and easier for a large pharma acquirer to absorb cleanly. That is the profile attracting capital right now — and it has real estate consequences. Lean, focused businesses need less space and can often gravitate toward shorter-term leases. The era of large, long-term speculative lab commitments from early-stage tenants is unlikely to return in the near term.

Three Forces Reshaping Demand: Patents, GLP-1 Maturation, and AI

Despite the challenging near-term supply picture, three structural forces are creating genuine, durable demand — while also reshaping what that demand looks like physically and geographically. The first is loss of exclusivity, or LOE — the patent cliff. Large pharmaceutical companies have spent the past decade largely outsourcing their internal R&D, relying on licensing deals, partnerships and acquisitions to replenish pipelines as blockbuster drugs lose patent protection. The volume of LOE events coming over the next several years creates structural urgency that will not abate. A typical pharma business development team evaluates a thousand small companies to close deals with a handful, hoping one produces a new name-brand therapeutic that justifies the cycle. This drives sustained demand from well-funded pharma and biotech M&A targets and from the dealmaking infrastructure those transactions require.

The pattern of expansion, overheated peak and uneven correction is familiar — but the scale of this cycle is different.

The GLP-1 sector — which two years ago operated on a “slap that label on anything and it gets funded” basis — has matured into something more nuanced and, arguably, more sustainable. The market has moved well beyond the original obesity framing toward addiction, central nervous system indications, inflammation and new delivery modalities, including oral formulations. The easy wins are gone. Companies competing in the crowded core GLP-1 space now must genuinely differentiate: unlock a new indication, reach previously untreatable patients, or shift the care setting in a meaningful way. Even the largest players have felt the pressure — the dynamics between the major incumbents have made clear that even in a massive market, proximity to the category leader is no longer a viable strategy. GLP-1-related development activity remains significant but increasingly favors specialized, focused operators.

The third force — AI-driven drug discovery, or computational biology — may be the most consequential long-term factor reshaping life science real estate. The applications cluster into four areas: AI-assisted drug discovery, which accelerates the identification and optimization of therapeutic molecules; insight platforms and infrastructure, which build the computational foundation for biological understanding; AI diagnostics, which accelerates disease detection and monitoring; and clinical response prediction, which uses computational models to project patient outcomes at scale. What unites these is the potential to compress laboratory timelines and reduce the volume of wet lab work required in early-stage discovery.

Recovery is real, but it is not broad-based — capital is concentrating in fewer companies and fewer markets.

It is too early to draw hard conclusions, and intellectual honesty requires acknowledging that. But early signals are worth watching. The proportion of R&D company footprints allocated to laboratory space — which climbed above 60 to 70 percent during the peak cycle — appears to be retreating toward the traditional 50/50 office-lab split, or below it in some cases. Whether AI is the primary driver is unclear, but the directional shift is real. If computational tools meaningfully reduce bench time requirements over the coming decade, the demand profile for life science real estate could shift in ways that affect both total square footage and the lab-to-office ratios that landlords have been building to. This is not an imminent disruption — but it is something to track now, not later. Separate but related, exponentially advancing AI capabilities will also radically change the landscape of non-bench talent (and thus office space needed) — scientific writing for INDs, clinical trial protocol writing and management, scientific study report creation, etc., may need significantly reduced numbers of humans.

The China Factor: More Complicated Than the Headlines Suggest

The standard narrative — China as pure competitive threat, reshoring as the solution — is incomplete in ways that can lead to poor decisions. China’s life science presence is not going away. The country now accounts for approximately 30 percent of global clinical trial starts, has representation in over 40 percent of the top 50 R&D pipelines globally, and is party to roughly one-third of all life science licensing deals by value. The labor and facility cost advantage is extraordinary.

A recent firsthand experience illustrates the scale of that disparity. Working with a top Chinese CDMO that was seriously evaluating a U.S. brick-and-mortar operation, the numbers told a stark story: all-in costs — operational labor, facility expenses, the full picture — would run approximately 10 percent in China of what the same operation would cost in Raleigh-Durham, which is itself far from the most expensive U.S. market. The company ultimately passed on the U.S. location, and the debrief left no ambiguity about why.

30%

That cost reality has direct implications for the “reshoring” conversation. Domestic manufacturing of some active pharmaceutical ingredients for patent-protected, high-value therapeutics is economically viable and is happening. But commodity API production cannot be competitively manufactured in the U.S. at the scale the drug substances are being used — the U.S. will not eliminate imported API anytime soon. Domestically manufactured demand is real, but it is concentrated in specialized, high-margin production, not broad-based pharmaceutical reshoring. Site selectors and portfolio managers should calibrate expectations accordingly.

The more actionable insight is that well-capitalized Chinese life science companies are actively seeking U.S. market access. Several major CDMOs and research organizations are evaluating U.S. real estate right now, looking for domestic footholds for regulatory, partnership and commercial purposes. China will be an important contributor to the world’s therapeutic technologies that ultimately the U.S. market will want access to. The U.S. will need to find ways to both compete and collaborate with China. Economic development organizations and corporate real estate teams should be prepared to engage seriously with inbound interest.

Strategic Implications: What to Do Right Now

Several practical principles emerge for site selectors and portfolio managers navigating this environment.

Know your market’s actual strengths — not the aspirational version. The impulse to position every emerging market as a future Boston is understandable but often counterproductive. The more useful question is what specific research capabilities, university assets or talent pipelines actually exist in a region — and which life science companies would genuinely benefit from proximity to those assets. Building direct, ongoing relationships with technology transfer offices and active university researchers is essential. These people are not thinking about economic development; their world is their science. The economic development professional has to be the translator — building a working database of institutional strengths and identifying companies in relevant fields that might benefit from being nearby.

Expand the definition of the ecosystem. An AI-enabled life science company may need nothing more than high-quality office space and proximity to computational talent. It is not a traditional lab tenant, but it is increasingly essential to the drug discovery pipeline. Life science campuses and parks that can accommodate both wet lab occupiers and data science-oriented companies will be better positioned to attract the full range of relevant tenants. The convergence between life science and technology is real, and being fluent in both the traditional life science pitch and the tech pitch is becoming a competitive differentiator.

Rethink the incentive toolkit. In markets where landlords are already offering substantial concessions to fill vacant lab space, cash incentives from economic development organizations may be partially duplicative. The more strategic approach is to preserve that financial capacity for situations where it is genuinely decisive, and invest instead in non-cash value drivers: streamlined permitting, clear regulatory pathways, pre-negotiated utility agreements and well-documented site readiness packages. Speed and process clarity have real monetary value to life science companies navigating internal approval processes that are often staggeringly complex. Demonstrating the ability to move fast — without bureaucratic friction — is worth more than many organizations realize, and it costs comparatively little to deliver.

For corporate real estate managers, the parallel question is whether portfolio positions reflect where life science activity is actually concentrating today, rather than where it peaked several years ago. Secondary markets with healthy supply-demand balance, supportive research infrastructure and competitive cost structures deserve fresh evaluation. Positions in oversupplied primary markets should be assessed against realistic absorption timelines.

Finally, act as an ecosystem steward, not merely a transaction facilitator. Life science cluster development is a multidecade commitment requiring the sustained coordination of universities, hospitals, developers, utilities and corporate partners. RTP is a useful model — but it did not happen overnight, and it required deliberate, durable governance structures. The clearest competitive advantage a market can offer sophisticated occupiers — who arrive with plenty of internal complexity of their own — is simplicity and clarity on the outside. Clean governance, transparent processes and well-connected local liaisons reduce friction at exactly the moments when it matters most.

Lean, focused businesses need less space and are gravitating toward shorter-term commitments.

The Road Ahead

The life science real estate market of 2026 is neither the euphoric expansion of 2021 nor a sector in collapse. It is in a genuine reset — working through a supply overhang while the underlying scientific and commercial drivers remain intact. The patent cliff will sustain pharma acquisition activity for years. AI will continue reshaping the discovery process and, with it, the physical requirements of R&D. Capital will flow, but toward companies with clear differentiation and manageable complexity.

The organizations that emerge strongest from this period will be those that used the correction wisely: deepening market intelligence, sharpening positioning around specific research niches, and building the governance and stakeholder relationships that make them credible partners for sophisticated occupiers. The pendulum has swung. Knowing where it is heading — and being positioned accordingly — is the work of the present moment.

Cushman & Wakefield Vice Chair Deb Boucher leads a specialty practice group of local and national experts dedicated to all aspects of science and technology real estate. She is especially experienced advising users of technically complex, highly improved spaces as they navigate layered occupancy and exit strategies, spanning multiple markets throughout North America and the world.