A Low Tax Regime

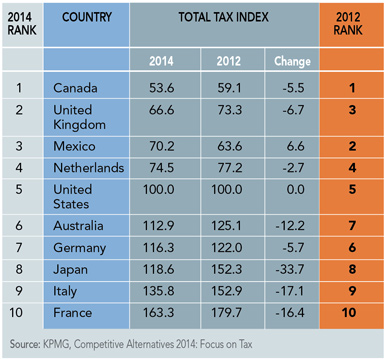

Canada has witnessed a remarkable transformation in the business tax landscape. Once known for having one of the highest corporate income tax rates in the developed world, Canada now has one of the lowest rates of the Group of Seven (G7) leading industrial economies and is near the middle of the pack of OECD countries.

Canada’s corporate tax rate dropped in 2012 as the last phase of federal cuts took effect. This tax cut is consistent with the global trend in the reduction of corporate tax rates, but Canada’s rate fell faster than other countries’ rates during the year, according to KPMG’s Global Corporate and Indirect Tax survey of tax rates affecting business. The combined federal-provincial statutory corporate income tax rate has come down from approximately 42 percent in 2000 to 26 percent today (weighted average), making it more attractive for businesses to locate in Canada. These changes in tax policy have also made it more attractive for businesses to invest in capital goods (new machinery, equipment, and structures). Canada now has the lowest and, hence, the most tax-competitive marginal effective tax rate (METR) on capital investment in the G7 and one that is below the OECD average.

Tax Competitive Cities

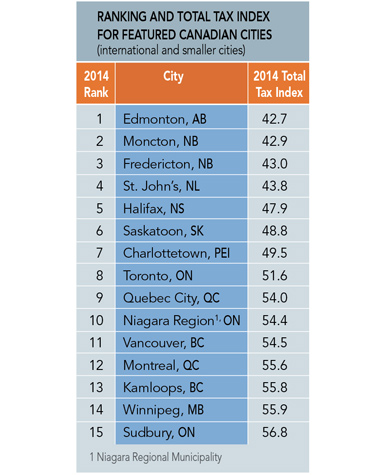

Toronto, Vancouver, and Montreal take the top three spots among major international cities in 2014 (Figure 2). While Toronto ranked first overall among the 51 major international cities studied, Vancouver ranked ahead of Toronto in 2012, but dropped behind Toronto in the 2014 rankings. This change in ranking is due to several factors, including British Columbia’s corporate tax rate increase from 10 percent to 11 percent, the final reversion from HST (harmonized sales tax) to PST (provincial sales tax), and the elimination of the BC industrial property tax credit (which provided a partial exemption from school taxes for industrial property).

Edmonton has moved up from second place in 2012 to first place in 2014 and is the most tax-competitive city in Canada. The reason for this is that former tax leader, Saskatoon, has dropped to sixth place in 2014, primarily because of the changes made to the Saskatchewan R&D tax credit in 2012.

Atlantic Canada remains a highly tax competitive region in Canada with Moncton, Fredericton, St. John’s, and Halifax rounding out the top-five tax-competitive cities in the country. Additionally, when taking overall costs into account, the KPMG study revealed that Moncton (NB) is the lowest-cost business location in Canada and the U.S.

Quebec City moved up to ninth place for TTI this year, primarily due to an innovative property tax provision that rewards owners who improve their properties, thus causing assessed value to increase. Bio-pharma and e-business incentive enhancements also helped Quebec City secure this spot.

Strong Industrial Sector Rankings

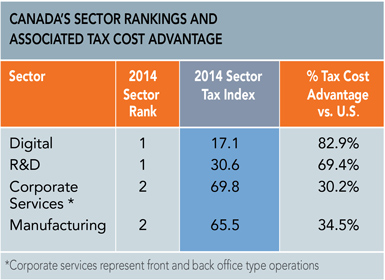

Despite the ever-changing landscape of Canadian industries, Canada’s 2014 sector rankings remained strong.

Canada ranked first in the digital services sector with a low TTI (17.1) (Figure 3). This is primarily due to significant provincial incentives that provide support to video game producers and other digital media industries. Canada remains in first place in this sector because of federal and provincial income tax credits for R&D. Canada’s top ranking for research and development makes it an ideal location for companies involved in the R&D sector. Canada ranked second behind the United Kingdom in the corporate services sector, while it also ranked second behind Mexico in the manufacturing sector.

Canada has implemented a major new initiative that will eliminate tariffs on all manufacturing inputs by 2015 — the first country in the G20 to offer a tariff-free zone for industrial manufacturers. Canada’s initiative applies across the entire country, making the country one large FTZ for firms importing manufacturing inputs.

Canada’s FTZ-type programs offer investors the vitally important advantage of geographic flexibility. Canada’s programs do not restrict investors to a handful of locations that may be distant from their target markets. In effect, programs such as the Duty Deferral Program, the Export Distribution Centre Program, and Exporters of Processing Services Program make it possible to create an FTZ environment exactly where the business needs it, while still offering all the benefits of a traditional FTZ.

Provincial Programs

Provincial incentives have basically remained consistent offering competitive programs for FDI investments. The provinces of Ontario and Quebec have recently undergone elections, and although new programs have been announced, the details of these programs have yet to be articulated. Both Ontario and Quebec are offering competitive incentives for investment projects meeting the new criteria. Once the details of these new programs are announced, the criteria should be similar to those offered in the past.