If the scramble for data center development feels unprecedented, it’s because it is. The US is in the middle of the largest infrastructure buildout since the construction of the interstate, impacting investors and communities across the US.

While profit-seeking motives are, naturally, a key driver for this market, there are geopolitical factors that structurally support this expansion. Indeed, data centers are so central to geopolitical competition and national well-being that the US and U.K. governments have both recently labeled them as critical infrastructure. Their criticality has been underscored in recent weeks when data centers became military targets in Russia and the Persian Gulf.

AI is an essential part of global competition, ensuring that geopolitics will continue to drive related infrastructure development.

Three Models, One Race

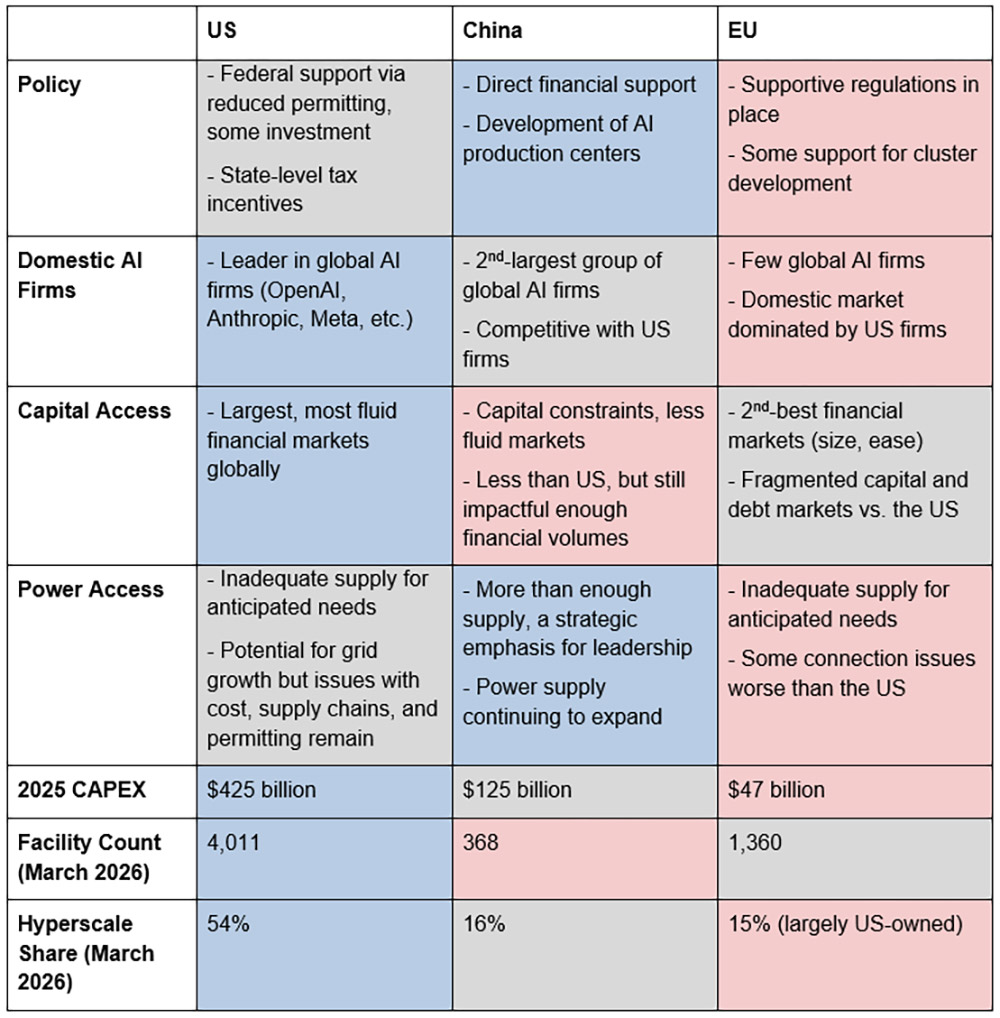

There are three main geographies for AI infrastructure development – the US, China, and the European Union – that have made this a strategic emphasis with geopolitical ramifications. As with broader global competition, it is the US and China that lead the way.

Broken down by key categories, here is how each of these actors stand:

In the US, private sector-led AI infrastructure development is booming. Government policy is supporting this by lowering barriers and risks rather than direct investment. Federal actions, such as the AI Action Plan and a spate of executive orders, and state-level incentives (available in at least 37 states) aim to ease the development of large-scale data centers. American-based AI companies are world leaders, easing domestic scaling. And capital is more accessible and abundant in the US. The key constraint is power, where a spike in demand after years of flat growth is running into cost, supply, and permitting challenges.

China’s approach bears more signs of state direction. Government development of AI production centers, incentives for subnational governments, and direct funding for AI firms helps de-risk and guide investment from private entities. As in the US, local AI firms, such as Alibaba, Huawei, Tencent, and others, allow for ease of local scaling. While China has more rigid structures around capital and total AI investment volumes lag the US (see below), Chinese AI development focuses on more compute for less cost – something DeepSeek has notably modeled. Power is China’s strongest asset in this competition, as years of grid and generation expansion give the county room for data center additions.

Data centers are so central to geopolitical competition that governments are beginning to treat them as critical infrastructure.

Lastly, the European Union. The EU AI Act, active since 2024, is the world’s first comprehensive legal framework for AI, providing a structured regulatory environment for AI tools. Still, the physical environment remains challenging. AI firms in the EU lag behind global peers, evidenced by the fact that US firms hold an estimated 70% of the local EU data center market.[1] The EU has more capital potential than China, but still less than the US due to fragmented financial regulations. Constraints on power echo those in the US, as wait times for grid connection have been cited as 7 to 10 years.[2]

For investors and economic developers, the US case offers the most financial and development opportunity at a scale and pace that is generational.

Rising Resistance

On the surface, AI infrastructure tailwinds and geopolitical competition paint a picture of extended growth. However, rising political and policy constraints mean that the window for this large-scale buildout could be closing soon.

Over only 2 years, from 2023 to 2025, project cancellations due to local opposition jumped from 2 to 25 (with 21 of those coming in Q3-Q4 2025).[3] In the same timeframe, community opposition, previously limited and fragmented, coalesced into nearly 200 formal groups across 40 states.[4] State legislation that had focused on attracting data centers shifted to restricting them, with over 250 bills introduced regulating the use of energy, water, and zoning.[5]

250

Proposed state-level policies to restrict data centers that previously fizzled out are starting to lead to breakthroughs. Illinois recently paused data center tax incentives for two years, with 12 states, including Virginia, Georgia, and Oklahoma, considering similar measures. The bipartisan makeup of these states underscores the widespread appeal of this pushback.

In time, greater federal regulation of data centers and their development looks likely. The AI-friendly US administration nodded to public concerns by trying to get ahead of issue. This March, they secured a “Ratepayer Protection Pledge” by large AI firms to insulate consumers from data center-related power price hikes, although it has no enforcement mechanism.

Because federal policy designates data centers as critical infrastructure, economic assets that overlap with core national interests are ripe for regulatory oversight. The widescale introduction of electricity in the early 20th century may serve as an example. Initially led by private firms, its centrality to national growth and security was such that power generation soon evolved into the regulated environment we still use today.

Community opposition to data center development has rapidly evolved from fragmented concerns into organized movements across dozens of states.

Federal legislation to enact a data center moratorium has already been proposed in Congress, although it is unlikely to make any progress this year. Still, with midterm elections approaching and local opposition increasingly informing legislative agendas, this issue will reassert itself again. Regardless of who controls Congress in 2027, the bipartisan pushback seen at the state level could also emerge at the federal level.

What Comes Next

Politically, the future is clear: a shift away from the more permissive regulatory environment of today and towards greater oversight and restrictions. How can we reconcile the geopolitical necessity and domestic constraints for future growth?

To answer this question, communities and companies are exploring an ecosystem approach, one that builds on the financial focus of the past by expanding into the broader economic environment.

Wisconsin’s experience with Microsoft over the past few years charts exactly this path. An initial hyperscale investment in 2023 evolved into a collaborative ecosystem development by 2024. Microsoft partnered with a local technical college to establish a sustainable workforce pipeline. Educational and private sector partners developed with Microsoft an innovation lab that has already supported 23 manufacturing-focused AI startups. Microsoft launched AI skills training for 114,000 local residents in partnership with area nonprofits, and worked to improve environmental impacts.[6]

4,011

Although this kind of ecosystem-wide project is not the norm, it is in line with emerging trends from other industry actors. OpenAI has proposed “AI Economic Zones”, where in exchange for expedited permitting for data center construction, communities receive support for research, workforce, and local tech industry development. Microsoft is following its Wisconsin experience with the launch of the “Community-First AI Infrastructure” framework this year, addressing community impacts and local ecosystem development.

There were good reasons to formalize this structure, as it was launched after community opposition stopped a separate, proposed Microsoft data center in Wisconsin. To reduce the likelihood of such risks in the future, Microsoft is already implementing their framework in Washington state, Georgia, and Canada.

The current wave of AI infrastructure investment may represent a finite window before regulatory and political constraints reshape the landscape.

This approach to AI infrastructure build-out evolves from a transactional mode to an ecosystem mode, benefiting both investors and economic development along the way. The data center gets built and investment risks are mitigated with political durability and reducing the probability of opposition. The local community gets both a local project and a sustainable boost to future-facing growth. The Wisconsin initiative is already creating success, as Microsoft has announced a second, similar data center project in Wisconsin and community feedback has broadly been positive.

The Finite Window

An ecosystem approach is not a panacea, as the traditional model can still be relevant for the right location. It will be communities with leverage that are best placed to seek out this kind of model, and that leverage is not equally distributed. But where this can be applied, investors and communities may be able to increase long-term growth and reduce risks.

vAs the data center buildout reaches a fever pitch before these constraints arrive, stakeholders need to consider a range of approaches. The pace and scale of change that data center developments bring are inherently challenging, so navigating that reality with local stakeholders will always come with tension.Because geopolitical competition is a core feature of our world, it will continue to drive radical changes in technology, the economy, and our communities. The locations that get this right will be positioned for the next wave of investment when it comes.

[1] Cushman & Wakefield, European Data Center Market Report, 2025.[2] International Energy Agency (IEA), "Overcoming Energy Constraints is Key to Delivering on Europe's Data Centre Goals," November 2025.

[3] Baird equity research, analyst Justin Hauke, 2025; corroborated by Heatmap News independent review.

[4] Data Center Watch (10a Labs), opposition group tracking report, mid-2025.

[5] MultiState legislative tracking service, 2025; corroborated by WilmerHale, Data Center Legislative and Regulatory Update, 2025.

[6] Microsoft On the Issues, "Expanding Our Investment in Wisconsin," May 8, 2024; Microsoft On the Issues, "Microsoft's $3.3 Billion Investment in Wisconsin," September 2025. Additional detail: Racine County Economic Development Corporation (RCEDC) project updates; Brookings Institution, AI and Community Development in the Midwest, February 2026.