From Background Risk to Primary Filter

Geopolitics used to sit at the edges of site selection—a risk factor to note, a scenario to model, but not a driver of the decision. That has changed. For foreign direct investment projects in particular, geopolitical risk has moved to the center of the analysis.

Trade tensions across North America, the European Union, and key Asian trading partners are creating real hesitation among international investors. The question companies are asking before committing capital to a U.S. manufacturing location is no longer just whether the site meets technical requirements—it is whether the broader environment is stable enough to justify a 20- or 30-year operational commitment.

The USMCA Review: A Structural Uncertainty

The United States–Mexico–Canada Agreement approaches its first major review in July 2026. This is not a formality. Built into the agreement is a checkpoint at which all three countries must decide whether to extend the deal for another 16 years, renegotiate its terms, or allow it to move toward expiration in 2036.

For manufacturers, particularly in the automotive sector, this review matters enormously. North American automotive supply chains cross borders multiple times before a vehicle is completed. Parts manufactured in Mexico ship to U.S. assembly plants; Canadian suppliers feed both. The trade rules that govern those flows—tariff structures, content requirements, rules of origin—are what make those supply chains economically viable.

If the agreement is extended cleanly, that stability allows investment planning to proceed. If it is renegotiated with significant changes, companies must reassess. If the outcome is uncertain for months, investment decisions slow. The uncertainty itself is a cost.

If the outcome is uncertain for months, investment decisions slow. The uncertainty itself is a cost.

Supply Chain Exposure and the Chokepoint Problem

Geopolitical disruptions also affect the raw materials that manufacturing depends on. Critical inputs—copper, nickel, cobalt, aluminum—move through global trade routes that are increasingly subject to disruption. Supply chain planners who once treated those routes as reliable are now building in redundancy, nearshoring where possible, and evaluating sourcing strategies with geopolitical scenarios in mind.

This has direct implications for site selection. A location's proximity to domestic or nearshore suppliers matters more than it did a decade ago. Dependence on long or politically exposed transit routes is now a risk to be assessed, not assumed away.

Where Investment Is Going—and Why

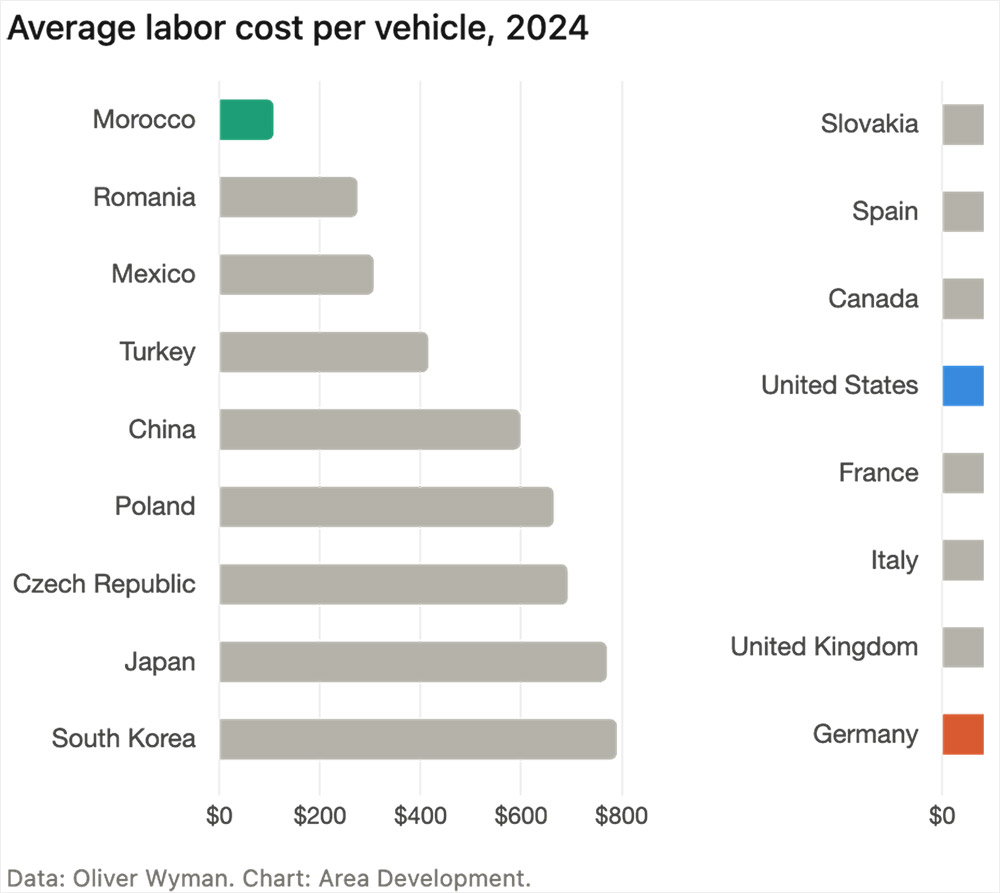

The United States remains a compelling manufacturing destination: deep infrastructure, skilled workforce, large domestic market, and a legal framework that supports long-term investment. But companies are evaluating it in context. Mexico offers lower labor costs and USMCA-connected trade access. Emerging manufacturing hubs in Southeast Asia and North Africa offer targeted incentives and competitive cost structures. Each option carries its own geopolitical profile.

16

For foreign investors—particularly those from countries currently in trade tension with the United States—the calculation is more complex. Regulatory scrutiny through mechanisms like CFIUS (Committee on Foreign Investment in the United States) can add timeline uncertainty and cost. Some investors have redirected capital to Mexico or Canada for exactly this reason, seeking locations where geopolitical friction is lower even if other factors are less ideal.

Long-Term Commitments in a Short-Term Policy Environment

Manufacturing investments are inherently long-term. A new plant represents a 20- to 30-year operational commitment, with capital deployed upfront and returns realized over time. Geopolitical conditions can change substantially within that window.

This mismatch—between the permanence of the investment and the volatility of the policy environment—is one of the defining tensions in site selection today. Companies must evaluate not just current conditions, but plausible scenarios: What happens to this site's economics if a trade agreement changes? What happens to supply chain access if tariffs are introduced or withdrawn? What is the regulatory risk if political leadership shifts?

These are not hypothetical questions. They are now part of the due diligence process. Geopolitics has become a site selection variable—not because it always determines the outcome, but because ignoring it now carries costs that cannot be hedged away later.