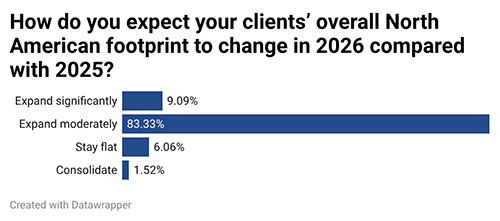

For decades, the bedrock question of corporate site selection was some version of the same calculation: where can we do this most cheaply? Labor arbitrage, tax incentives, real estate costs — the disciplines of location strategy were largely organized around the pursuit of the lowest delivered cost. That era is not simply fading. According to the results of Area Development's 2026 Annual Survey of Site Selection Consultants, it has ended.

What has taken its place is something more complex and, in many ways, more demanding: a relentless focus on operational certainty. The question companies are now asking their advisors is not "where is cheapest?" but "where can we be sure this will actually work?" The shift — from cost optimization to risk mitigation, from lowest-cost to most-reliable — is reshaping how sites are evaluated, how communities compete, and how the profession of site selection itself is practiced.

The survey, completed by leading location advisors across the United States, reveals a profession navigating an environment defined by compressed timelines, constrained infrastructure, a deepening shortage of qualified sites, and a macro backdrop of tariff volatility and political uncertainty that has made certainty itself a premium commodity. The data tell a story that is at once cautionary and instructive — and the voices of the consultants who responded add urgency and texture to every data point.

Speed Has Become a Strategy

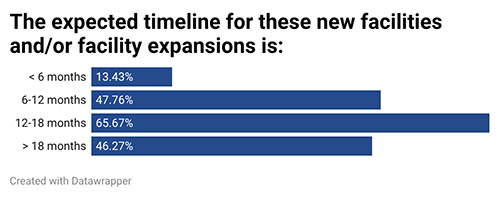

Perhaps no finding in this year's survey is more striking than the near-universal elevation of speed as a primary project driver. Certainty of permitting registered among the top-tier factors for 94% of respondents. Site readiness and due diligence status — a factor that ranked at just 78% in last year's survey — surged to 98.5% in 2026, one of the most dramatic year-over-year gains recorded across the entire dataset. Responsive state and local government held firm at 97%.

Read together, these numbers describe an industry in which the ability to move fast has become a decisive competitive advantage — not just for communities competing for projects, but for the companies pursuing them.

"Permitting speed and the absence of NIMBY activism have truly emerged as pivotal site selection factors here in 2026," says John Boyd, Principal at The Boyd Company. "In corporate location, 'timing is everything.' More and more of our engagements are prioritizing 'speed to market' as an overriding project goal."

Boyd's observation reflects a structural shift in client priorities. Companies are racing to capture market share, secure patents, and establish brand dominance before competitors can react. In some cases the urgency is regulatory: getting a project operational within the window of a time-sensitive federal contract or incentive program. Boyd points to a recent engagement in which fast permitting and strong community support helped identify a site in Middle Tennessee for Moldex-Metric — a Culver City, California-based manufacturer — specifically so the company could qualify for federal contracts from the Department of Health and Human Services for N95 mask production.

"Being first to market helps some of our clients secure patents or establish a brand before competitors can copy or claim similar technologies," Boyd adds. "For some projects, getting up and running sooner can also help clients qualify for certain time-sensitive incentives, especially those coming from federal programs."

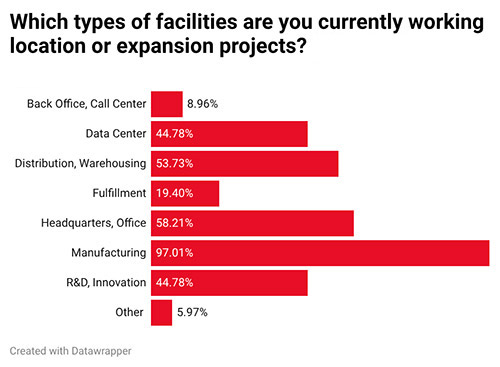

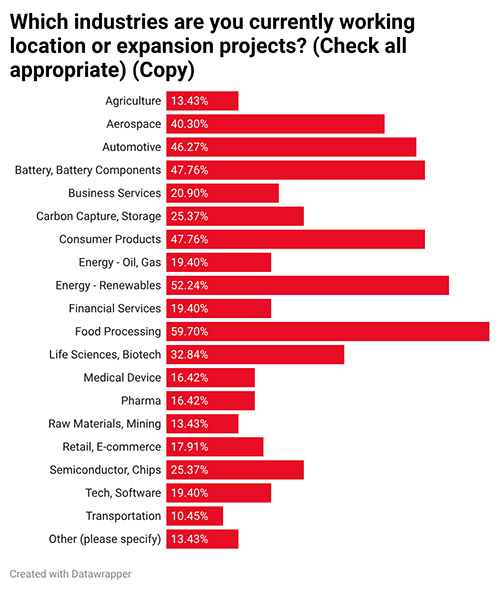

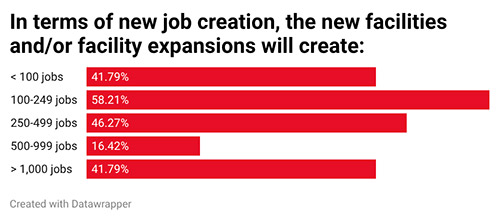

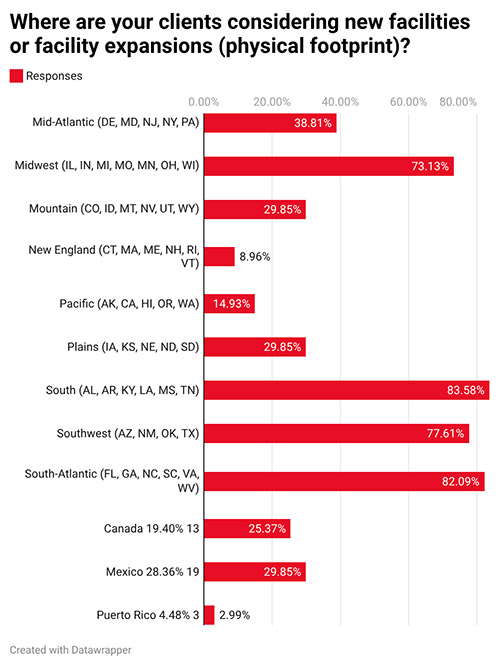

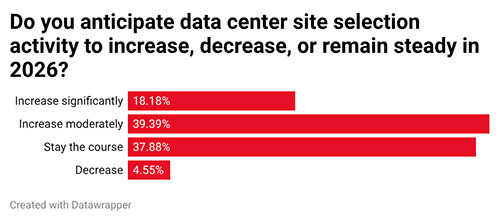

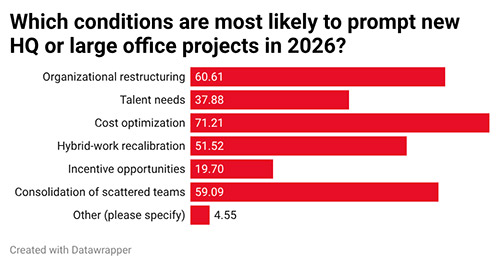

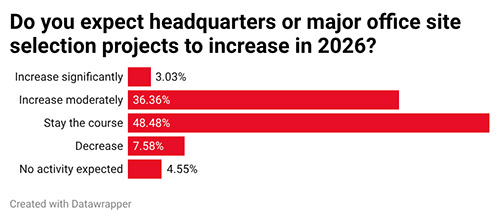

22nd Annual Consultants Survey

-

Chart 1

-

Chart 2

-

Chart 3

-

Chart 4

-

Chart 5

-

Chart 6

-

Chart 7

-

Chart 8

-

Chart 9

-

Chart 10

-

Chart 11

The implication for economic developers is direct: communities that can demonstrate a genuine, documented path from site selection to shovel in the ground — not a marketing claim, but an engineered and legally verified timeline — will increasingly win the projects that matter most.

Energy: From Background Factor to Deal-Breaker

If speed is the new competitive frame, energy is the new filter through which every location is first evaluated. Electric power availability at scale appears at 98.5% in the 2026 survey — essentially universal — with 82.6% of respondents rating it "very important," the highest intensity score of any factor in the infrastructure category. Transmission and substation capacity comes in at 97%, with nearly three-quarters of respondents at the "very important" level. Grid reliability and redundancy follows at 92.5%.

These are not incremental changes. They represent a wholesale repositioning of energy infrastructure from a background utility concern to a front-of-process qualifying criterion.

"Our clients, especially those with loads over 25 MW, need us to evaluate the availability, cost, and timing of electricity much earlier in the site selection process than in previous searches," says Mark Williams, Founder and President of Strategic Development Group. "In many cases, it's no longer a given that these 'have to have' variables will work, so they are addressed earlier in the search process. More frequently now, first contacts on searches are electricity providers."

That sequence — reaching out to utilities before almost anyone else — would have been unthinkable in most searches a decade ago. Today it is standard operating procedure for a growing share of major projects.

Gray Swoope, President and CEO of VisionFirst Advisors, describes a recent international manufacturer search where the top criterion was identifying communities capable of supporting 295 megawatts by 2030. "That requirement immediately triggered transmission studies to evaluate feasibility, timing, and cost," Swoope explains. "Even with those results, the differentiator was risk — which locations could realistically deliver power within the client's timeline, including procuring long-lead equipment and, where needed, incorporating bridge solutions while major upgrades came online."

Swoope is direct about what this means for market selection: "We are seeing markets fall out of consideration early when utilities cannot provide a clear path to power on the client's timeline, including firm milestones and risk mitigation options. In many cases, locations are eliminated not because demand is impossible to serve, but because the schedule risk is too high."

Larry Gigerich, Executive Managing Director at Ginovus, frames the underlying problem in structural terms. "Energy demand is outstripping supply in most places in the U.S. We have had the perfect storm — the federal government has not invested in the national electric grid in nearly 60 years, the aggressive push to reduce energy derived from fossil fuels impacted supply and reliability, zoning and planning regulations make it very difficult to build transmission lines to distribute power where it is needed, and data center and reshored manufacturing projects require significant power to operate." Gigerich calls for an "all of the above" energy strategy — including nuclear — and notes that "massive investments will be required to ensure reliability and availability of power."

Charles Sexton, Founder and CEO of Strategic Location Advisers, points to the data center sector as particularly illustrative of how energy concerns are reshaping location decisions. "Data centers, especially hyper-scale, are highly focused on energy availability combined with quality of sites and potential constraints such as natural gas access and public opinion for their own power plant construction." For communities that previously viewed industrial and manufacturing recruitment as their primary focus, the data center boom is reordering infrastructure priorities in ways that have cascading effects on every other sector competing for the same scarce power capacity.

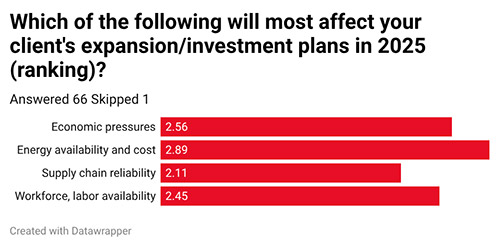

40th Annual Corporate Survey

-

Chart 1

-

Chart 2

-

Chart 3

-

Chart 4

-

Chart 5

-

Chart 6

The Site Shortage Is Real — and Getting Worse

Behind the urgency around speed and energy lies a more fundamental constraint: there are simply not enough qualified sites. Site readiness and due diligence status, as noted, saw one of the survey's most dramatic year-over-year jumps — a 20-point gain from 2025 to 2026. Availability of contiguous and developable acreage with expansion potential sits at 92.5%. Zoning compatibility and environmental and land-use risk both register above 88%.

"During the past decade, many of the best real estate sites have been developed for industrial projects throughout the U.S.," Gigerich observes. "As a result, it is more challenging than ever to find an ample number of good sites for projects. With many states having different standards for what constitutes a certified or shovel-ready site, there is inconsistency in the marketplace when it comes to a site being ready to develop."

Shannon O'Hare of Cushman and Wakefield adds another dimension to the site scarcity problem: the compounding effect of rising costs on project timelines. "Cost escalations are proving difficult to manage. With rising costs and the uncertainty of budgets growing, we are seeing 'approved' projects revert for additional approvals. Multiple layers of approval add time, and with limited site availability, adding time is always a gamble. Will the project's preferred site still be available when the project is approved to move forward?" It is a question, O'Hare notes, that companies are increasingly unable to answer with confidence.

Greg Burkart, Principal in Site Selection Services at Walbridge, describes the compounding pressure in stark terms: "The nationwide demand for data center development is tightening the market for power, sites, and skilled labor, which historically was distributed across large manufacturing projects. This is forcing some companies to reconsider where and when they can move forward. Additionally, community acceptance has become a top consideration affecting capital-intensive projects, including data centers. Site selectors will need plenty of lead time for engagement to get the local community comfortable with your project."

Labor: Still No. 1, But the Definition Is Changing

Availability of skilled labor retained its position at the very top of the survey rankings, cited by 100% of respondents as important or very important. Depth of technical talent pipelines — including community colleges and trade schools — came in at 95.5%, up sharply from 79.7% a year ago. The message is not merely that labor matters; it is that the nature of the labor that matters is changing.

"Labor cost and availability continue to play a major role in site selection because they affect how quickly a project can get up and running and how competitive it will be over time," says Alex Miller, Manager of Client Services at KSM Advisers. "Automation is helping address some labor challenges, but companies still need a dependable workforce to launch and run their operations. As a result, many location decisions are leaning toward markets with balanced labor conditions that allow companies to scale without putting pressure on margins."

Gigerich frames the talent challenge in generational terms. "The need for fewer undergraduate degrees and more associate degrees, along with industry-recognized credentials and certifications, has impacted the delivery of education and training across the U.S. With the significant growth of AI, automation, and robotics, there will be further disruption in the area of talent." The communities that invest now in training pipelines aligned to technical credentials — welders, machinists, automation technicians — will be better positioned to compete for the high-value manufacturing and advanced industrial projects that are reshaping the location landscape.

NIMBYism, Volatility, and the New Weight of Community Acceptance

Among the survey's most telling findings is the emergence of political and regulatory stability — cited by 94% of respondents — as a core site selection factor. Responsive state and local government held near the top of the overall rankings at 97%. And several consultants identified community opposition as a rising constraint that demands proactive management from the earliest stages of a project.

"The rise of NIMBYism in many locations in the U.S. is having a significant impact on how companies are evaluating potential locations," says Gigerich. "NIMBYism started with people pushing back on distribution centers and then spread to data centers — now we are seeing pushback on manufacturing projects. As a result, site selectors and companies are being more proactive in sharing the benefits of a proposed project earlier in the process."

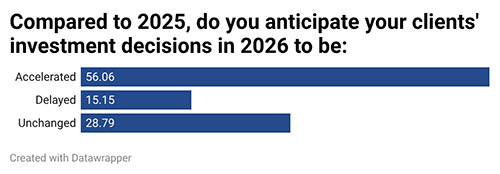

At the macro level, the survey reflects an environment of broader uncertainty. Sexton notes that companies are making decisions "prior to or in light of potential federal administrative impacts — the right or wrong tweet or decision in the middle of the night can have a major impact on risk tolerance." The observation captures something that does not easily fit into a percentage ranking but pervades every conversation in the profession: the background hum of political and policy volatility that has made operational certainty harder to achieve and therefore more valuable when it can be found.

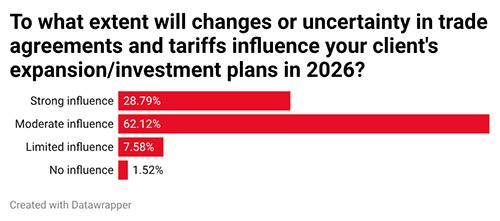

Steve Tozier of EY addresses tariff uncertainty directly. "Trade-related tax considerations have historically been a consideration for businesses as they evaluate where to locate new operations. However, the subject has elevated in importance over the last year in light of new tariff policy around the globe. In some cases, changes in the tariff landscape have prompted — and even accelerated — business investment into new jurisdictions. In other cases, site selection decision-making has slowed as companies analyze alternative options, including rethinking the sourcing of key equipment or production inputs from more tariff-optimal locations." The ambidextrous effect — tariffs simultaneously accelerating some investments and paralyzing others — captures the fundamental challenge of operating in an environment where the rules keep changing.

Gregg Healy of Savills puts it plainly: "Our clients are realizing that it's less about finding the cheapest location and more about minimizing disruption risk. Nearshoring and supplier realignment are pulling companies toward established supplier clusters, reliable power, and logistics certainty — often through phased expansions rather than all-at-once commitments. In 2026, political, regulatory, and financial volatility isn't a side consideration — it's directly influencing where companies go, how fast they move, and how much optionality they demand."

Or, in Healy's most distilled formulation: "In North America, site selection is no longer about cost — it's about certainty."

The Defense Sector: A Market Apart

No survey of the current location environment would be complete without acknowledging the sector that stands in sharpest contrast to the general mood of caution: defense and aerospace. Jeff Troan of Vista Site Solutions describes a market that is, in his words, "booming."

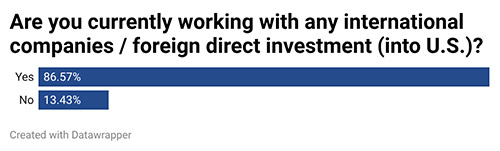

With the U.S. defense budget approaching $1 trillion and executive branch proposals seeking $1.5 trillion — plus the pending SHIPS Act, which would establish a 25% federal tax credit for shipyard investments — Troan identifies a cascade of facility requirements flowing from military shipbuilding, aircraft maintenance and overhaul, drone warfare technology, and Army weapons production. "I haven't spoken to a military contractor in the past year or two that isn't being taxed to significantly expand production, resulting in a requirement for new facilities and tooling." From the Gulf Coast to the Great Lakes, maritime-adjacent communities are finding that the Navy's drive toward a 350-ship fleet — combined with new financing mechanisms for commercial shipbuilding — is creating location opportunities that did not exist five years ago.

The drone and autonomous systems subsector, Troan notes, is particularly notable because its requirements differ fundamentally from traditional defense manufacturing. "In many cases, this subsector requires more innovative software minds than capital investment, and we are seeing a whole new generation of aerospace companies emerge." The location implications are distinct: proximity to university research ecosystems and deep software talent pools may matter as much as traditional defense-industrial infrastructure.

What Communities Must Do Now

The aggregate picture that emerges from this year's survey is one of structural tightening — in energy, in qualified sites, in talent, in timelines — against a backdrop of heightened volatility in trade policy, regulatory environment, and community sentiment. For economic developers, the message is both challenging and clarifying.

The communities that will win in this environment are not necessarily those with the most aggressive incentive packages or the lowest tax rates. They are the ones that have done the hard preparatory work: engineering-validated, genuinely shovel-ready sites; utilities with a documented and credible path to large-scale power delivery on a defined timeline; community engagement processes capable of getting ahead of NIMBY opposition; and governments that can respond with the speed and competence that compressed project schedules now demand.

"Site readiness, good infrastructure capacity, and competent local professionals continue to grow in importance for corporate decision makers," Sexton observes. It is a short sentence that summarizes, perhaps better than any other in this year's survey, what has fundamentally changed about site selection in 2026.

The old question — where can we do this cheapest? — has not disappeared. Cost still matters; operating cost structure registered at 97% in the survey, and incentive competitiveness remains near the top of the rankings. But cost has been reframed. It is no longer the organizing principle of a location decision. It is one variable in a broader assessment centered on a more demanding question: where can we be certain this will work?

That certainty — of power, of sites, of permits, of talent, of community support, of regulatory stability — is what companies are paying for in 2026. And the locations that can deliver it are, increasingly, the ones that will define the next decade of American industrial geography.