Here's a question worth pondering: if AI can reduce your supply chain forecasting errors by 20 to 50 percent, reduce inventory carrying costs by 35 percent, and cut lost sales from stockouts by 65 percent — what does that do to your facility footprint? Because that's the question I think site selectors and corporate real estate executives need to start asking, and many of them aren't asking it yet. Those numbers aren't projections. They're what leading companies are already achieving with AI-enabled demand planning and inventory management systems, according to research from McKinsey, Gartner, and others. And when you stack them together, the implications for real estate are significant. A 35 percent reduction in inventory levels across a distribution network doesn't just improve balance sheet efficiency — it changes how much space you need, where you need it, and how you think about lease commitments.

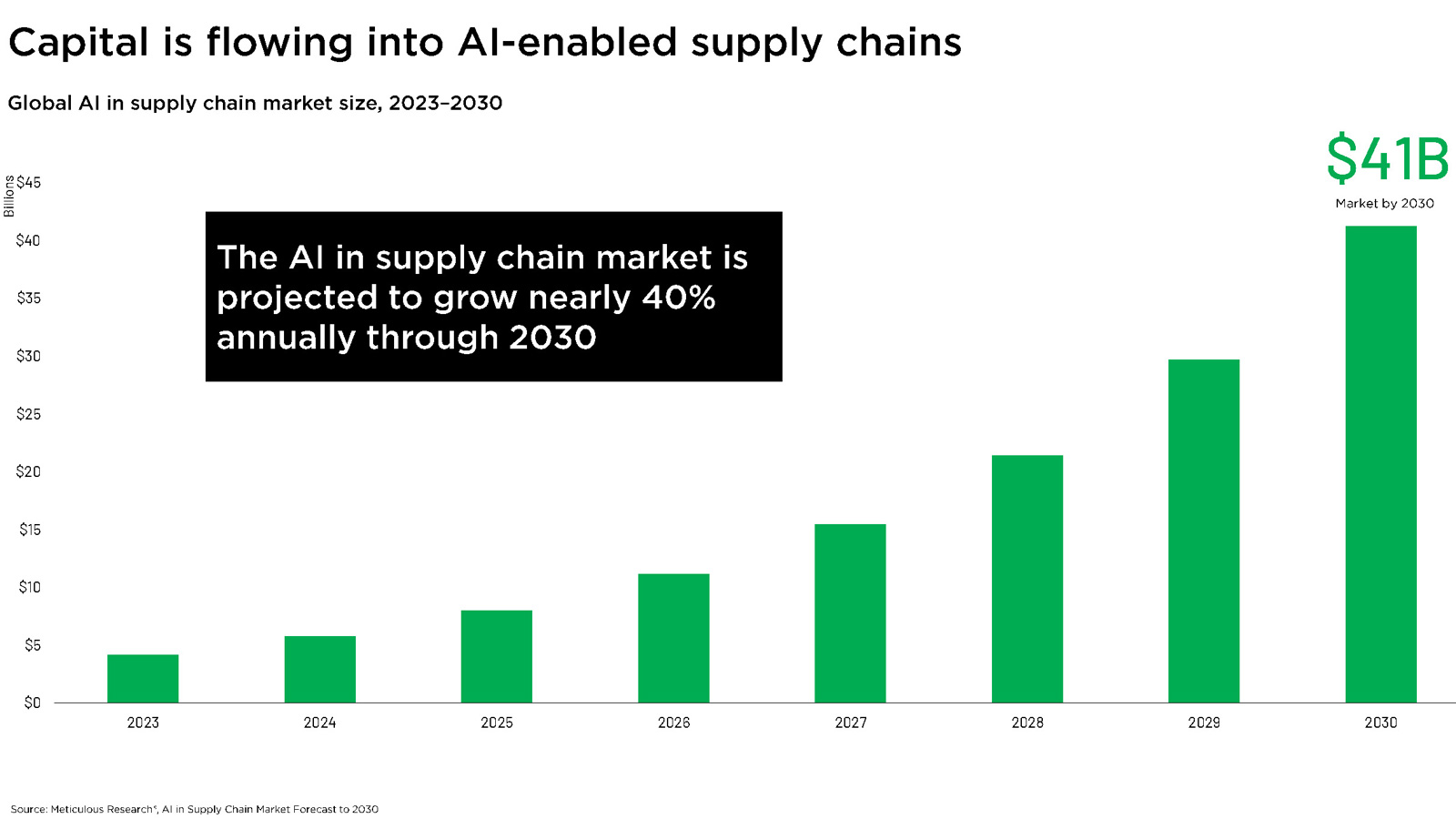

The global AI in supply chain market is currently on a trajectory to reach $41 billion by 2030, growing at nearly 40 percent annually. Gartner projects that 60 percent of supply chain planning will be powered by generative AI by 2027. PwC expects 90 percent of supply chains to be AI-augmented by 2030. These aren't fringe predictions — they represent the emerging consensus among the researchers and practitioners who study this most closely. Machine learning isn't just accelerating supply chain operations; it's accelerating the discovery process itself, compressing timelines that used to play out over years into months.

The most consequential near-term application, from a real estate standpoint, is inventory and production forecasting. Traditional forecasting models are built on historical patterns. They're reasonably good in stable environments and fall apart in volatile ones — which is to say, they've been falling apart pretty consistently for the past five years. AI-driven models ingest a far wider range of inputs: real-time demand signals and customer/consumer behaviors, supplier lead times, geopolitical risk indicators, port throughput data, even weather patterns. They update continuously rather than in periodic planning cycles. And in an environment defined by disruption, that matters enormously.

For a site selector or corporate real estate executive, this translates into a practical planning challenge. The assumptions underlying a facility decision — how much space, what clear height, how many dock doors, what lease term makes sense — are increasingly being shaped by AI-enabled operational models that your clients may still be in the process of or contemplating adopting. If their AI implementation reduces required inventory by a third, the 500,000-square-foot distribution center you're underwriting today may need to look different than it would have three years ago. That conversation is worth having proactively.

A Landscape of Compounding Disruption

Of course, AI doesn't exist in a vacuum, and neither do the supply chains it's being asked to optimize. The backdrop against which all of this is happening — tariffs, geopolitical risk, cost volatility, nearshoring pressure — is genuinely difficult to plan around, even with better tools. At Savills, a significant portion of what my team does is network optimization: helping companies figure out where their facilities should be, which markets they should serve, and how to balance proximity to suppliers against proximity to customers. The math is always about transportation — minimize distance, maximize service levels, keep costs manageable. What's changed is the volatility of the inputs and variables.

$41B

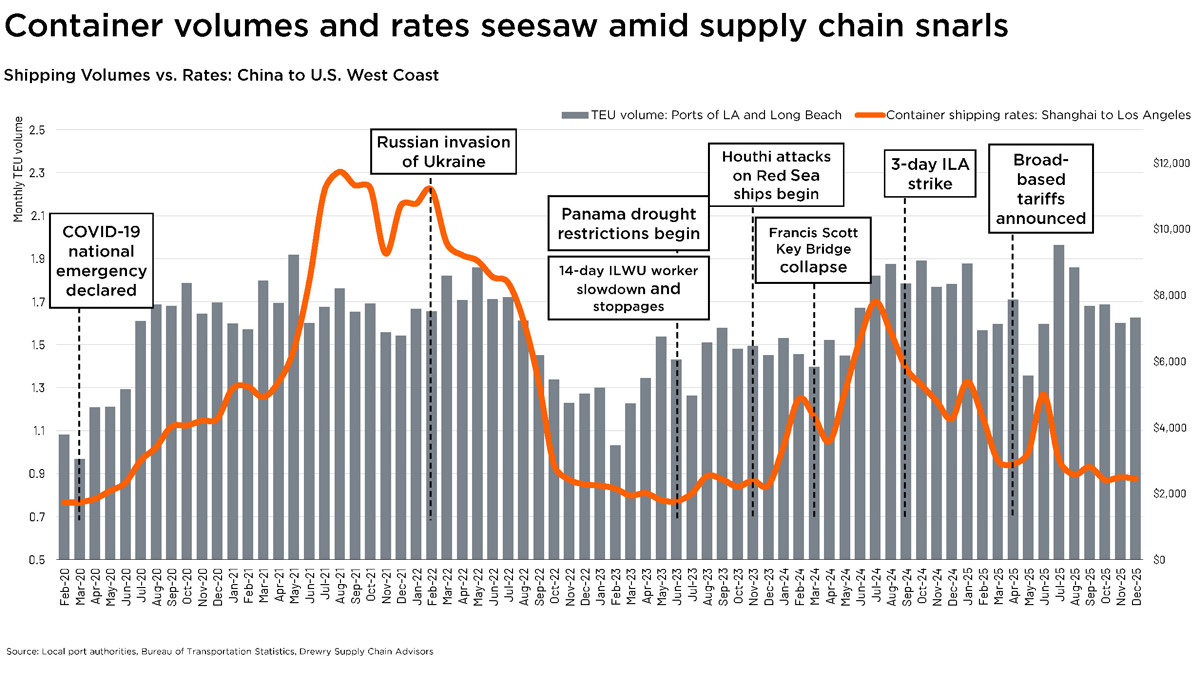

Consider what's happened to container shipping rates on the China-to-U.S. West Coast corridor since 2020. A container that cost $3,000 to $4,000 to ship pre-pandemic spiked dramatically during COVID, crashed back down, then spiked again — driven by a sequence of disruptions that reads like a stress test: COVID closures, the Russian invasion of Ukraine, Panama Canal drought restrictions, Houthi attacks on Red Sea shipping, the Francis Scott Key Bridge collapse, a brief ILA strike, and then broad-based tariff announcements that froze orders almost overnight. Each of these events is visible as a distinct spike in the rate and volume data. Taken together, they illustrate something important: there is always something going on in supply chains that disrupts the flow of goods. The question is no longer whether disruption will happen, but how quickly your network can absorb it.

Import volatility at the top nine U.S. ports neared COVID-era highs in mid-2025 as tariff deadlines triggered a wave of front-loading, followed by a sharp pullback as orders were canceled. Vessel tracking data captured the dynamic vividly: immediately after broad-based tariffs were announced, ships clustered off the Chinese coast as importers froze purchases. Within about a month of the policy being walked back, traffic patterns had largely normalized. The whipsaw is real, it's measurable, and it's exactly the kind of signal that AI-enabled forecasting and planning systems are designed to interpret faster than human planners can.

Port Volumes Tell a Resilience Story

What's worth noting, amid all this volatility, is that aggregate port volumes have held up surprisingly well. Of the nine major U.S. ports tracked in our Savills research, most grew their year-to-date TEU volumes in 2025 compared to 2024. Los Angeles handled 9.5 million TEUs, up slightly. Long Beach processed 9.0 million, up 2.9 percent. Savannah reached 5.3 million, Houston 4.0 million. Only Seattle/Tacoma and Virginia saw meaningful year-over-year declines. The global economy, measured by the actual flow of goods into U.S. markets, has proven more durable than the disruption narrative would suggest.

The practical implication for real estate strategy is that the push toward nearshoring and domestic manufacturing — while genuine — has not yet produced a significant reduction in import-dependent supply chain activity. Clients tell me they want to reduce their overseas exposure. Many are taking real steps to do so. But the containers are still moving. The nearshoring thesis is playing out as a supplement to existing global flows, not a replacement for them, at least for now. That means the industrial markets that serve as import gateways — Southern California, Savannah, Houston, the Northeastern corridor — retain their strategic relevance even as Texas border markets and Mexico-adjacent logistics hubs grow in importance.

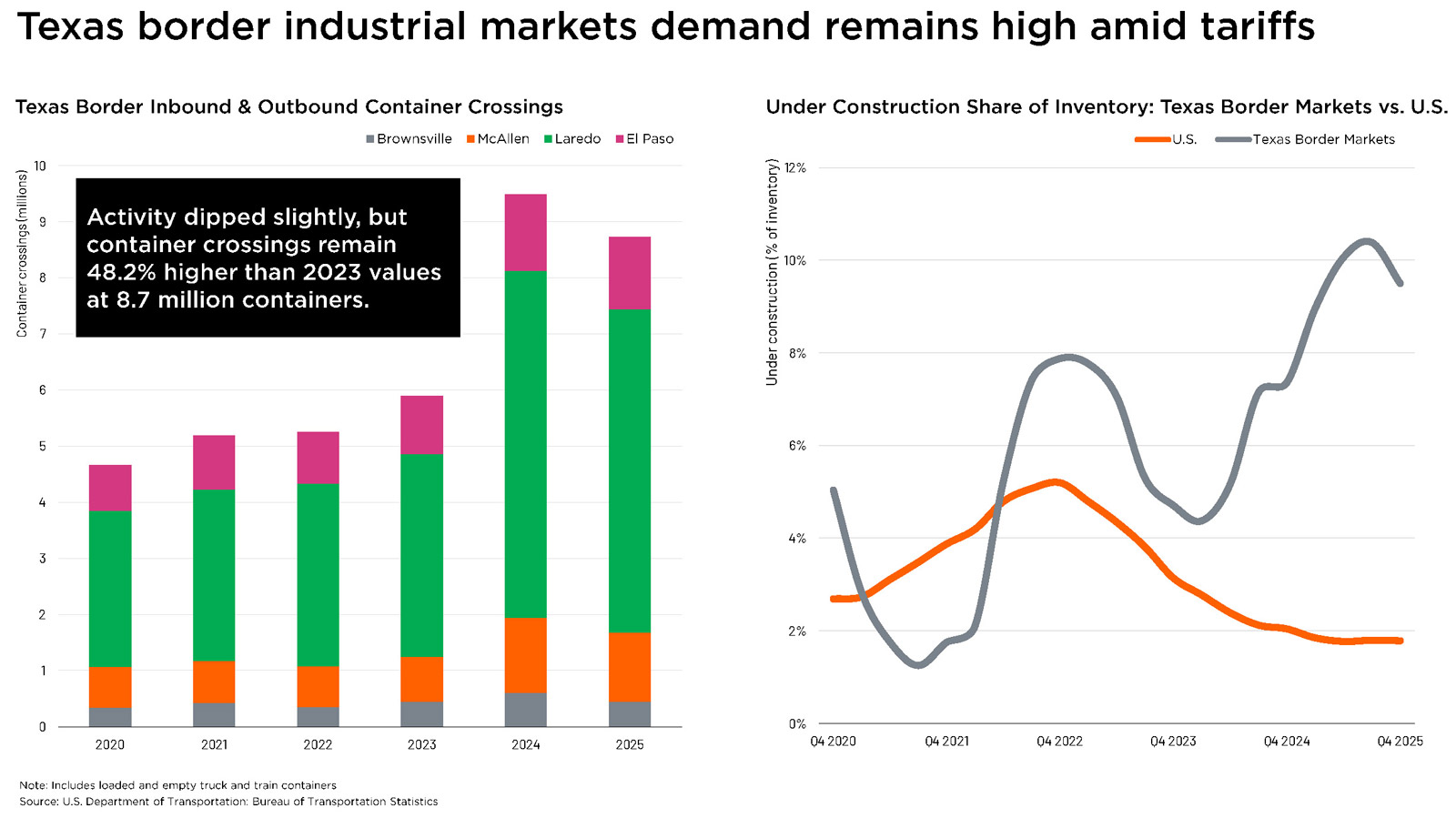

The Texas border data is particularly instructive. Container crossings at Brownsville, McAllen, Laredo, and El Paso remain 48.2 percent above 2023 levels at 8.7 million containers annually, even with a slight dip in 2025. Industrial construction in Texas border markets is running at multiples of the national rate as a share of inventory, reflecting genuine occupier demand rather than speculative development. That's the nearshoring thesis in action — not as a replacement for trans-Pacific trade, but as a parallel system being built to hedge against it.

Rhetoric Versus Reality on Reshoring

The manufacturing announcement picture is more complicated. Savills Research tracks U.S. manufacturing projects of 500 or more jobs, and the data over the past decade tells a nuanced story. New announcements have risen significantly over the past year — 53,416 jobs announced in the trailing 12 months, representing $42.2 billion in capital investment. But stalled projects are also at historically high levels, running well into negative territory on our tracking chart. Activity has risen even as previously announced projects are being canceled or put on hold at rates we haven't seen before.

48.2%

When you look at where the genuine activity is concentrated, three sectors account for 75 percent of new manufacturing project announcements in 2025: aerospace and defense at 49 percent, grid and energy at 16 percent, and digital infrastructure at 9 percent. These are not consumer goods factories or general industrial facilities. They are highly specialized, capital-intensive projects with long lead times and specific infrastructure requirements — power access chief among them. A project like JetZero's all-wing aircraft facility in Greensboro, North Carolina, with 14,500 jobs and $5 billion in capital investment targeting a 2028 opening, is real and consequential. But it's a different animal than the broad-based manufacturing renaissance that some of the headline numbers imply.

The power constraint is real and deserves more attention than it typically gets in real estate discussions. Grid capacity is increasingly a binding constraint on where advanced manufacturing and data center projects can actually land. The total capacity in the interconnection queue at the end of 2023 was nearly 2.6 terawatts — more than twice the current U.S. generating capacity. Half the country faces high risk of power shortfall within the next decade. For site selectors, this means power availability is no longer a checkbox item — it's a primary location filter for an expanding category of industrial demand.

What This Means for Your Next Decision

The industrial market fundamentals, taken in aggregate, remain solid. U.S. inventory stands at 17.2 billion square feet, vacancy has held at 8.2 percent, quarterly net absorption came in at 48.9 million square feet in Q4 2025, and asking rents have stabilized around $9.61 per square foot. Third-party logistics providers now account for 41 percent of leasing activity — up from 23.3 percent five years ago — reflecting the broader shift toward outsourced logistics as companies seek flexibility in an uncertain environment.

Against that backdrop, a few principles seem durable regardless of how the specific disruptions of 2026 play out. AI adoption in supply chain planning is accelerating faster than most real estate professionals have internalized, and the operational changes it enables — leaner inventory, faster replenishment cycles, more dynamic network configurations — have direct implications for facility sizing and lease structure. Proximity to customers remains the anchor of network strategy, because service level expectations that Amazon established are not going away. And flexibility has genuine option value in an environment where policy can shift a supply chain overnight.

The companies best positioned for the next five years are not the ones that guessed right about any single disruption. They're the ones that built networks — and real estate footprints — capable of absorbing surprises. AI is increasingly the tool that makes that kind of adaptability achievable. The question for everyone in this room is how quickly that reality gets priced into location decisions.